“A tie is like kissing your sister.”

-J.C. Humes

How about if America woke up on November 7th and “269 – 269” was the headline on the front of major newspapers? The implication would be that the Electoral College was effectively tied. This is actually a somewhat plausible scenario in 2012. It could occur with Obama winning all of Kerry’s states from 2004 and adding New Mexico and Ohio. Currently, both New Mexico and Ohio, albeit marginally, are in the Obama camp.

In the event of an Electoral College tie, the decision gets handed to the House of Representatives. Given that the Republicans hold a majority in the House, Romney would then become the next President. Just as many moderates think that the Tea Party has hijacked the Republican Party, they would now be arguably the key reason that the Republicans gained the Presidency. After all, if it weren’t for the Tea Party insurgency (for lack of a better word) in the midterms, the Republicans would likely not currently control the House.

Regardless of whether you believe my 269 scenario, it is beyond argument that this race is getting too close to call. The averages of the major national polls are basically within 0.5 points, favorability ratings of the candidates are basically tied, and neither candidate has a definite edge in the Electoral College.

There are some credible outliers related to predicting the outcome of the election. One of these is Professor Ken Bickers from the University of Colorado. He has done an analysis that looks at state level economics as a predictor for the Electoral College. Currently, his analysis suggests that Romney and Ryan may win up to 330 seats.

We will be joined by Professor Bickers today at 1pm today for a conference call to discuss his analysis. For institutional macro subscribers, the materials and dial-in will be circulated this morning. If you are not an institutional macro subscriber, ping to inquire about access.

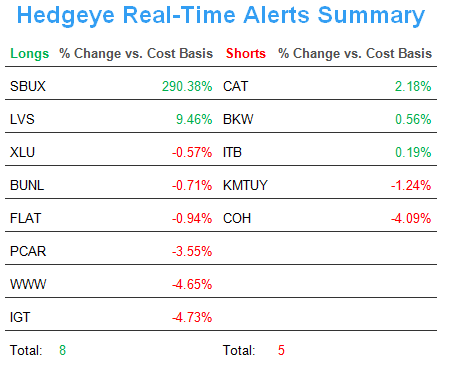

Politics matters as it relates to future economic policy, so we have been and will continue to focus closely on this election. In fact, we would postulate that some of the stock market weakness over the last few days, though largely driven by #EarningsSlowing, is being amplified by increasing uncertainty in political outcomes in the United States.

Globally, the bigger concern continues to be tepid economic growth. This morning HSBC’s flash PMI for China came in at 49.1 versus expectations of 47.9. Even if marginally better than expected, the number remains below 50. In Europe the numbers were bleaker as the Eurozone Flash PMI came in at 45.3 versus an estimate of 46.5. The German IFO business climate indicator also disappointed marginally coming in at 100.0 versus expectations of 101.6. Not surprisingly, the Euro is weak and Spanish yields are backing up this morning, as result.

It is a major policy day today in the United States with an announcement coming from the Federal Reserve. The FOMC rate decision will be held at 12:30pm today with a Bernanke press conference at 2:15pm. Even though the stock market basically peaked on the day of the last Fed announcement, it is unlikely that even Chairman Bernanke adds more fuel to the fire at this point. Although if the Fed were to signal they are going to take the money printing press up a gear, that would be the ultimate October surprise. It may even be bigger news than the October surprise that Donald Trump is purportedly going to reveal on Twitter today.

Our friends at Bespoke Investment Group actually did an interesting analysis looking at the return of the stock market on the days of Fed announcements in this period of zero interest rate policy. According to their analysis, the SP500 showed a positive return on 21 out of 31 of those days with an average gain of +0.71.

Even as history is a guidepost, we would suggest that investors are getting much better at front running the Fed. This is actually born out in the numbers as in the last year the return on a Fed day is closer to +0.30. Yes, this is still a positive return, but only marginally so. Today the setup seems more poised to disappoint as Chairman Bernanke will likely not have much new positive news on the economy, and is also unlikely to further ease. But, we’ve been surprised by the Fed before . . .

The broader issue with the Fed’s long-term zero interest rate policy is that extreme levels at which certain asset classes are getting priced. One example is the high yield market. As one high yield investor emailed me yesterday:

“Our basic premise is that there is massive technical support in the search for yield for the broader HY and leverage loan market driving yields to historically tight levels. There is such appetite in the loan market that terms are reverting back to 2007 peak levels…new issue spreads are being compressed and covenants are being pulled (45% of new issue is now ‘cov-lite’ vs. 10% last year). To a large extent this has been driven by the return of the clo…back from the dead…or at least from 2007. CLO issuance will be $40bn this year, which is more than the last 4yrs combined.”

Now we aren’t ready to make a big call on high yield market just yet, but the red flags raised above are well worth pointing out. After all, it’s not a tie if you are long high yield at the top.

Our immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $107.48-110.71, $79.58-80.16, $1.29-1.31, 1.71-1.82%, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research