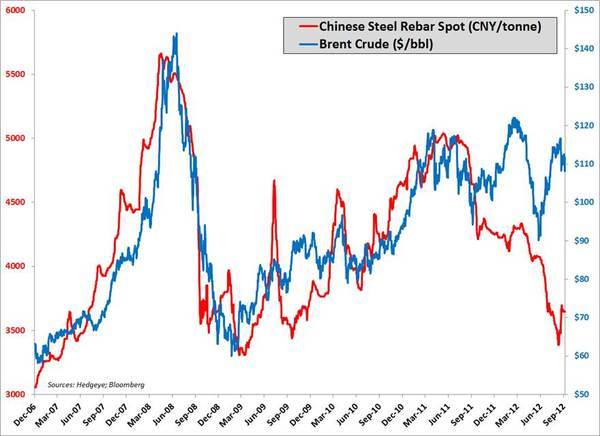

We like to compare the price of Brent Crude oil to Chinese steel rebar. Since the beginnning of 2012, there’s just been a massive drop in the price of both rebar and oil. And while oil got a legitimate bounce off the $90 level in June, rebar continued to head lower. Recently, there’s been a bounce in both rebar and Brent Crude, but we think it’s irrelevant as infrastructure spending is still on the decline. China isn't going to go on a building spree anytime soon.

Correlation does not equal causation, though this chart argues for Brent in the $70-80/bbl range. Something to think about. Rebar will have to climb higher and oil will have to head lower in order for these two to correlate closely again.