Strong recent stock performance and a still risky near-term environment, as evidenced by our recent pricing survey, leaves us on the sideline.

Despite a 6.5% increase in bunker fuel prices since their guidance on July 20, RCL should report in-line 3Q results Thursday due to better cost management. RCL has had six straight quarters of better than expected expenses ex fuel, and that streak should continue. 2012 guidance should be intact but F4Q may be lowered slightly due to continued pricing weakness in North America (i.e. Caribbean) and higher fuel prices. But investors may not care much about this fiscal year as all ears will be on Fiscal 2013 commentary. Bookings continue to be solid and will likely improve in 2013. F1Q 2013 is a difficult comp as yields were up 7% last year with much of the business booked before the Costa Concordia incident. We’re seeing slightly higher Caribbean pricing YoY for 1H 2013, though it is losing steam recently. 69% and 37% of capacity is in the Caribbean for 1Q 2013 and 2Q 2013, respectively. Meanwhile, the recovery in European pricing has been steady.

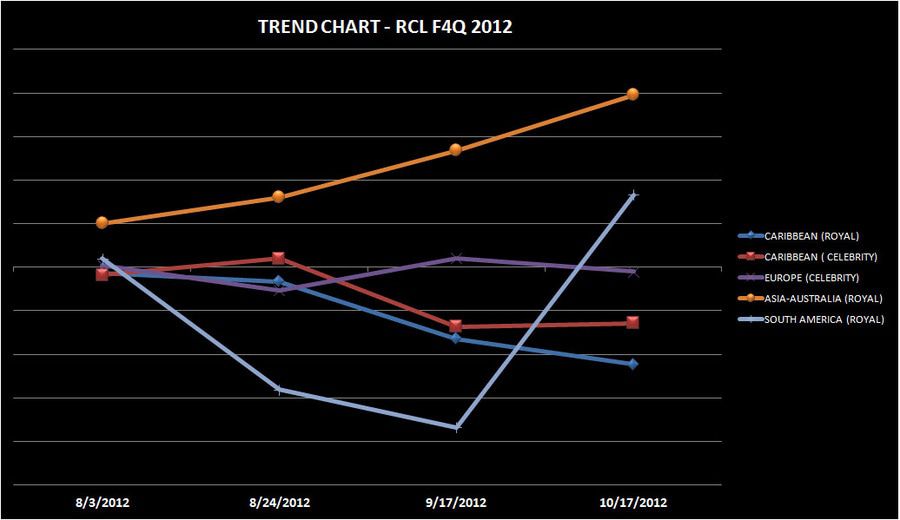

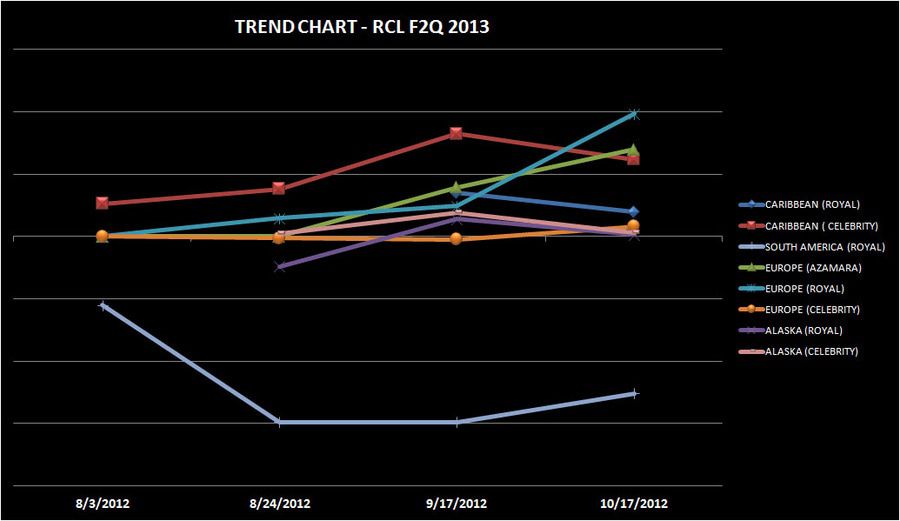

Here are some other conclusions from our cruise pricing survey completed last week. The charts below track pricing trends on a relative basis—i.e. prices relative to that seen on the last earnings call (RCL - July 20).

F4Q 2012

- Discounting on some last minute booking remains in the Caribbean. Celebrity pricing remains robust but the trend is slacking.

- Asia-Australia pricing continues to outperform as pricing trends have improved during the last two months

F1Q 2013

- Caribbean: pricing is flattish for RCL branded ships while modestly higher for Celebrity brands. Trend-wise, RCL brands slipped in prices from September to October while Celebrity brands improved slightly.

F2Q 2013

- European pricing continues to move higher across all brands

- Pricing in the Caribbean is flattish and the trend is worsening

- Alaska pricing hasn’t fluctuated much

Trading at more than 13x forward earnings, valuation is roughly in-line with its 20-year average. 2012 provided a difficult operating environment because of the European recession, increases in bunker prices, and costly incidents on the water. We believe 2013 could be another tricky year with difficult comps early in the year and the resiliency of the North America market will be tested again particularly with low GDP growth. The jury is still out on how RCL will handle the higher capacity in the Carribean in 2013. Europe may recover but the question is how much and how fast. While we are optimistic on RCL in the long-term on favorable demographics, low market capacity growth, and continued improvements on the cost side, we think it’s better to stay on the sidelines given the near-term risks and fair valuation.