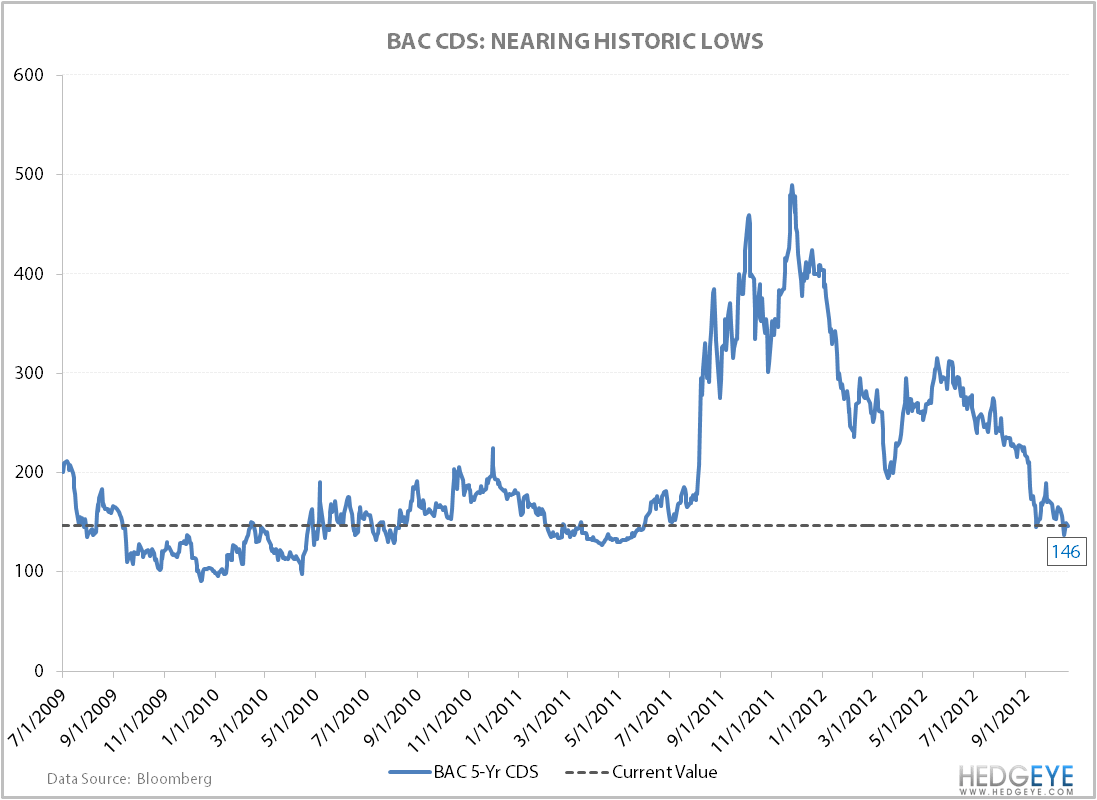

With many US large cap financials reporting earnings last week, reactions were essentially mixed for those participating in the stock market. However, the credit markets were delighted with earnings seeing them as a positive across the board. Credit default swaps tightened across the entire US financials complex, meaning that investors are less concerned with counterparty risk associated with the big banks like Citigroup (C), Goldman Sachs (GS) and Bank of America (BAC).

The positive notes in the credit market extended outside the US to Europe as well. The idea here is that financials have an embedded discount around counterparty risk and that investors in the stock market will soon play catch up to their peers in the credit market. In the intermediate-term side of things, be sure to keep an eye on the banks.