Did the Dept of Labor Double Count the "Missing State"?

This week's 49k WoW increase in initial claims is suspicious, just like last week's 28k decline. However, we suspect that the "missing state" from the previous week's data may have been double-counted this past week. Assuming that there was in fact a missing state, it's odd then that the previous week was not significantly upwardly revised. The number was upwardly revised by just 3k from 339k to 342k. It appears that instead, that missing state just lumped two weeks of data into this most recent week, which explains the moonshot increase of 49k this week. To be fair, we haven't seen anything to confirm our theory, but we see no other plausible explanation. As such, we would expect a roughly 25k decrease next week to around 363k, which is essentially in-line with the rolling average of late. For reference, it's also possible that Columbus Day (last Monday) caused some further dislocation in the series.

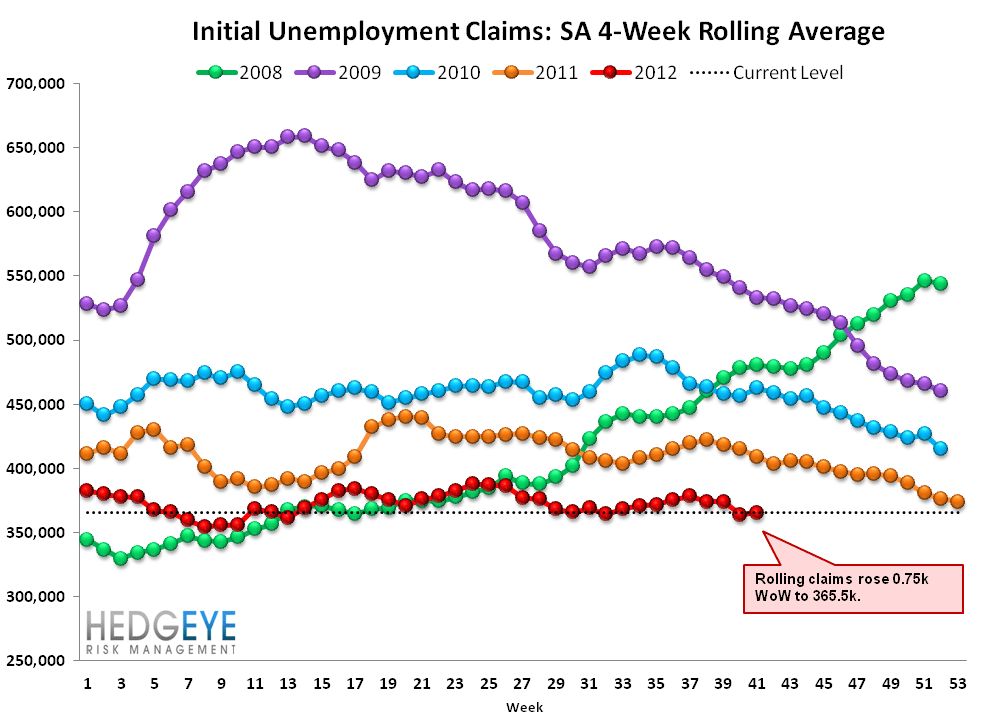

The bottom line is that the trend in jobless claims, i.e. the 4-week rolling average, is still trending lower, as we show in the first chart below. Notice that even after including this morning's huge increase in claims, the rolling average has only moved back to its trendline, which still has a negative slope. This is consistent with our thesis that there's a tailwind distortion in the data that will persist through February, 2013, making the labor market and economy appear stronger than they really are before reversing course in March 2013 and deteriorating through August 2013.

The Data

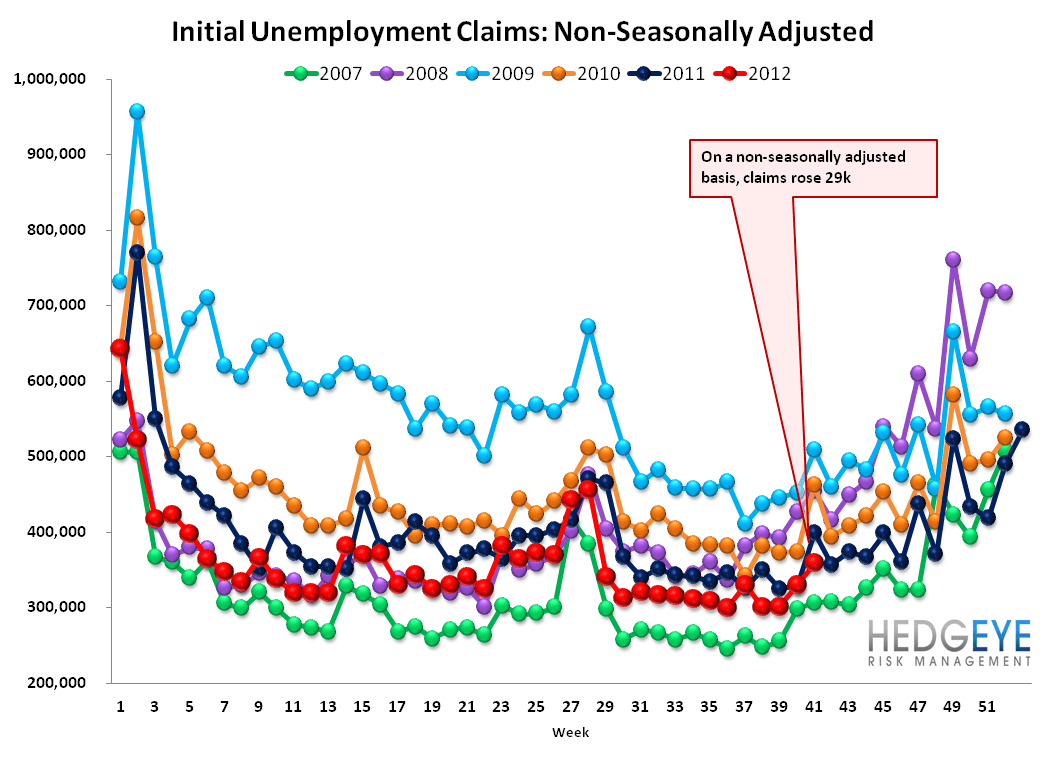

Initial claims rose 49k last week to 388k (but rose 46k after a 3k upward revision to the prior week's data). Rolling claims rose 0.75k WoW to 365.5k. On a non-seasonally adjusted basis, claims rose 29k to 359k.

Hedgeye Take

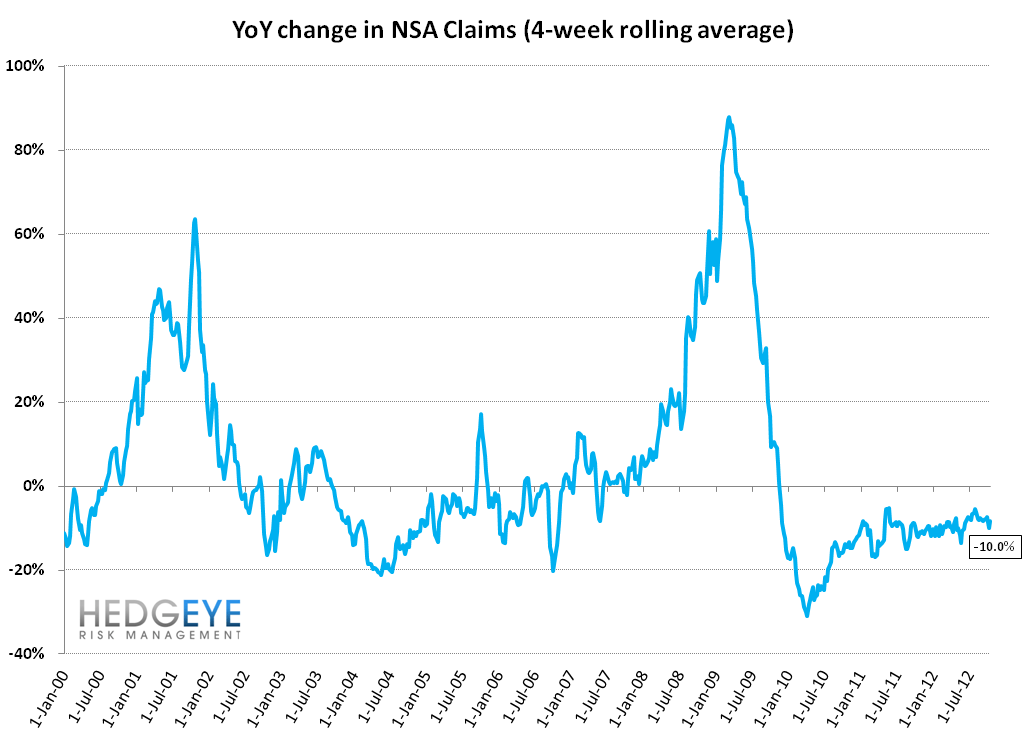

The YoY change in the rolling NSA series was roughly flat at -10.0%. This compares with -10.3% in the prior week and -7.4% in the week before that. This larger YoY improvement in the rolling non-seasonally adjusted data is meaningful as it indicates there is real improvement currently occurring in the employment environment.

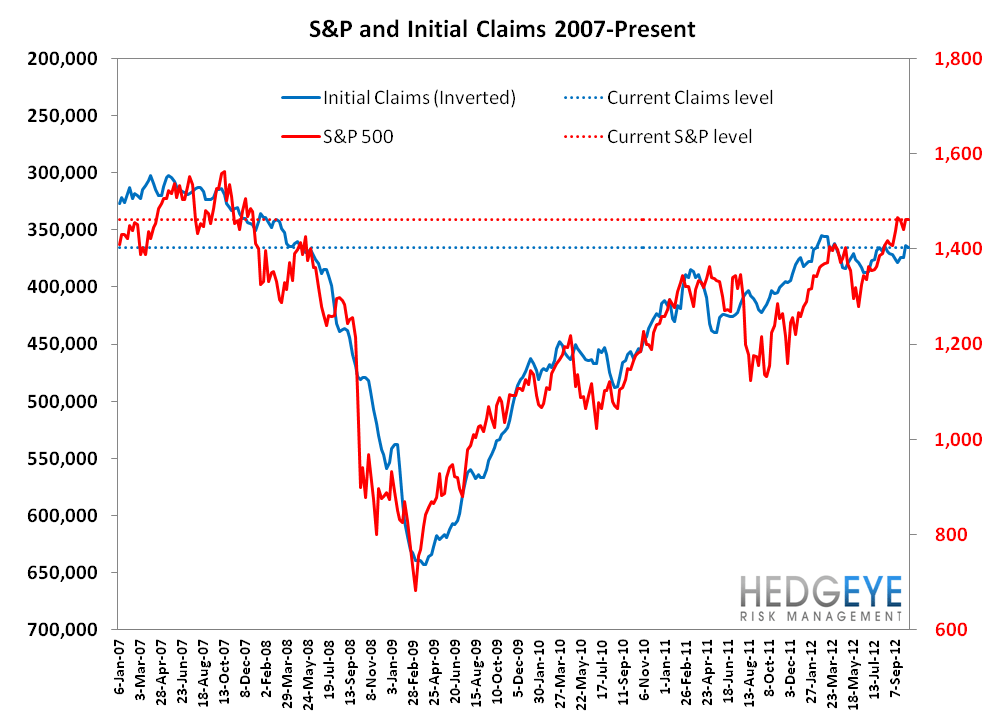

Lastly, the S&P and claims diverged again this week. For reference the current level of claims would imply an S&P level of 1372, which is 6% lower than current levels.

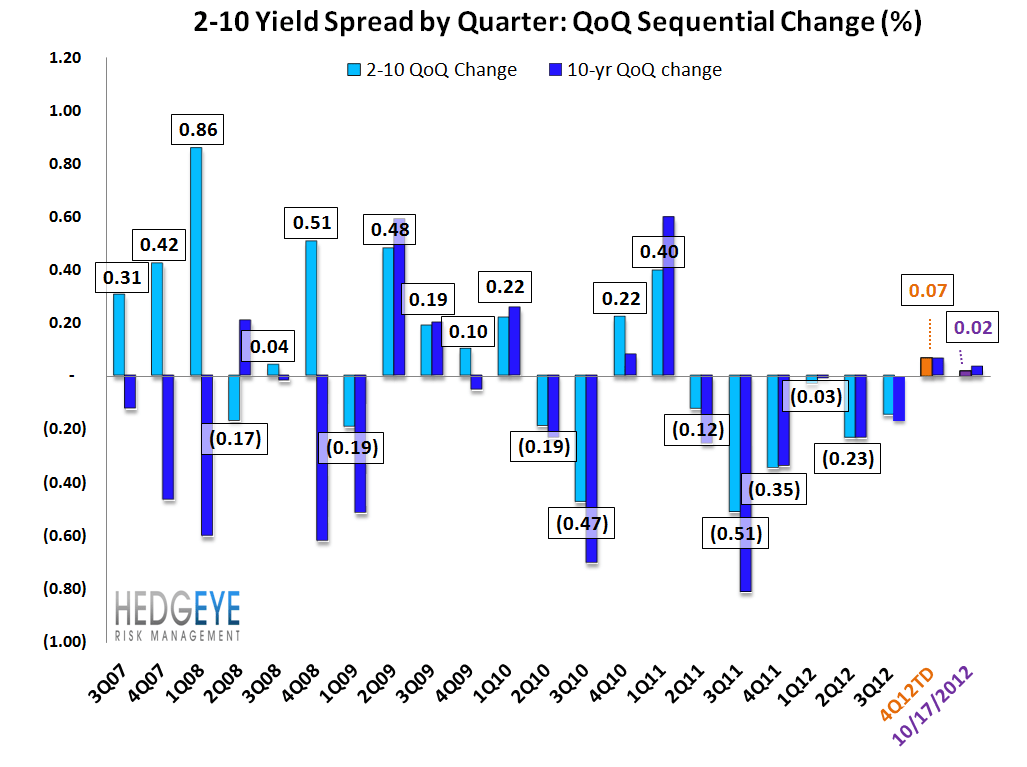

Yield Spreads

The 2-10 spread rose 12 bps WoW to 153 bps. So far 4QTD, the 2-10 spread is averaging 1.44%, which is up 7 bps relative to 3Q12.

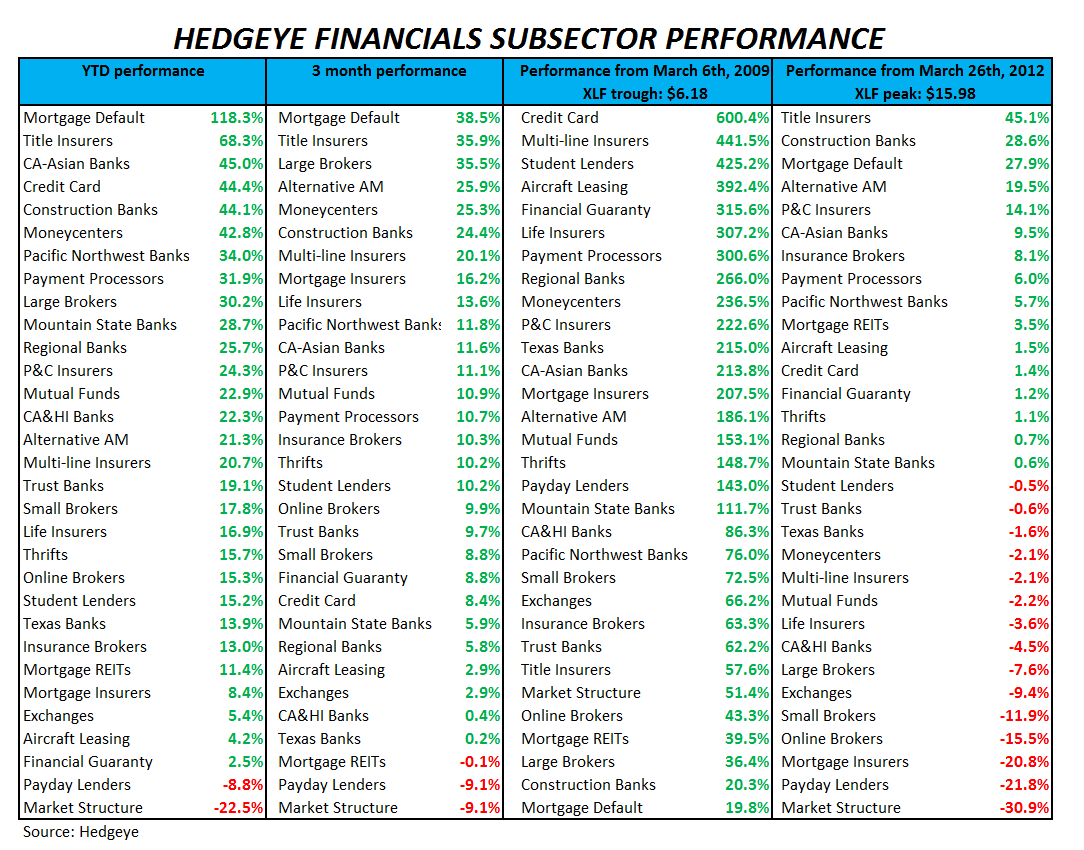

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over multiple durations.

Joshua Steiner, CFA

Robert Belsky