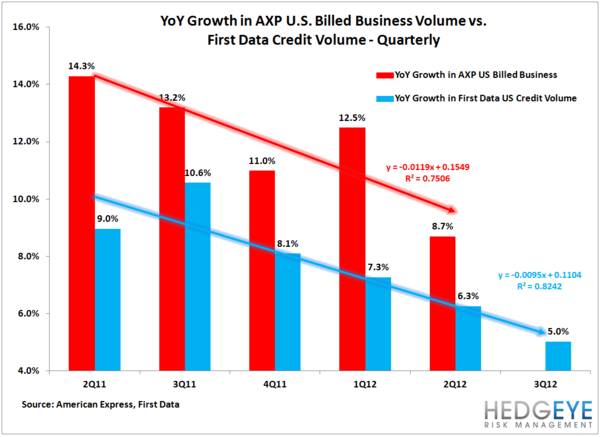

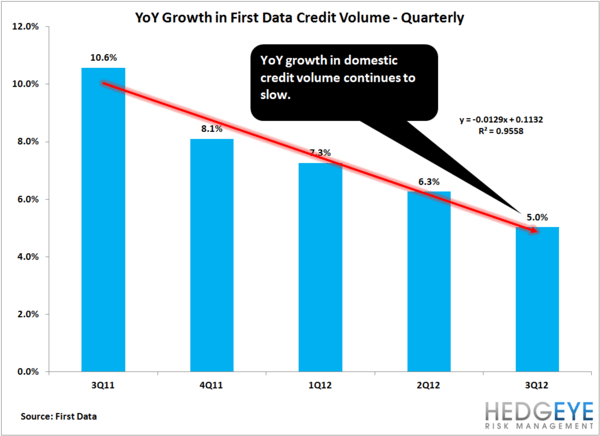

American Express (AXP) is experiencing the pandemic sweeping the financial world known as #GrowthSlowing. Using data from First Data, we’ve seen Amex credit volumes decline on a year-over-year basis. The company also faces headwinds in the form of a slowdown in consumer spending and tough comps for the month of September.

As for the Bluebird partnership with Walmart (WMT) that was announced yesterday, this is a positive for AXP. It’ll give the company access to the high-growth debit card market and revenue from fees associated with the card.