TODAY’S S&P 500 SET-UP – October 8, 2012

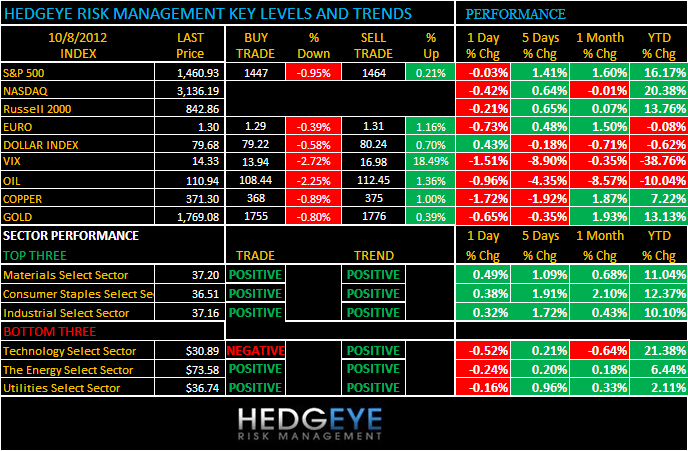

As we look at today’s set up for the S&P 500, the range is 17 points or -0.95% downside to 1447 and 0.21% upside to 1464.

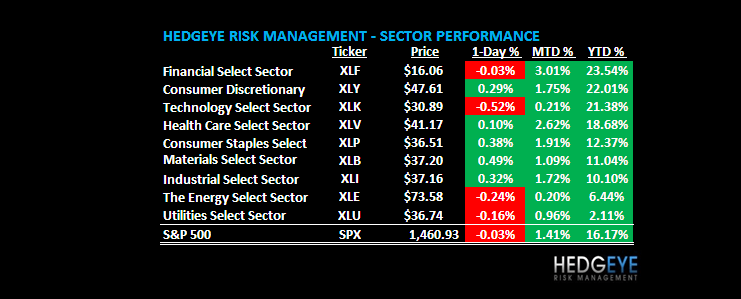

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 10/05 NYSE 408

- Decrease versus the prior day’s trading of 1384

- VOLUME: on 10/05 NYSE 606.70

- Decrease versus prior day’s trading of -10.08%

- VIX: as of 10/05 was at 14.33

- Decrease versus most recent day’s trading of -1.51%

- Year-to-date decrease of -38.76%

- SPX PUT/CALL RATIO: as of 10/05 closed at 1.93

- Up from the day prior at 1.58

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 25.49

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.74%

- Increase from prior day’s trading of 1.67%

- YIELD CURVE: as of this morning 1.49

- Up from prior day’s trading at 1.43

MACRO DATA POINTS (Bloomberg Estimates)

- No major U.S. economic data releases scheduled

- U.S. Economic Data Preview

- U.S. Rates Weekly Agenda

WHAT TO WATCH:

- Columbus Day holiday; equity markets open, bond markets closed

- Canadian markets closed for Thanksgiving holiday

- Allscripts said to get first-round bids from Blackstone, Carlyle

- Foxconn labor disputes disrupt iPhone production again

- Europe seeks to contain Spanish troubles as finance chiefs meet

- Amazon.com to buy Seattle headquarters complex for $1.16b

- Google to make first entry in credit-card business: FT

- Neeson gets revenge again as Fox’s ‘Taken 2’ leads wkend

- American Securities buys auto-parts co. HHI for $750m: WSJ

- Yahoo buyback urged by holders seeing doubling of shares

- Gannett, Dish talks extended by several hours

- Company at center of meningitis outbreak recalls products

- U.S. Weekly Agendas: Finance, Tech, Consumer, Real Estate, Transports, Media/Entertainment, Health, Industrials, Energy

- Canada Weekly Agendas: Energy, Mining

- G-7, IMF Meeting, Nobel Prizes, Sandusky: Week Ahead

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

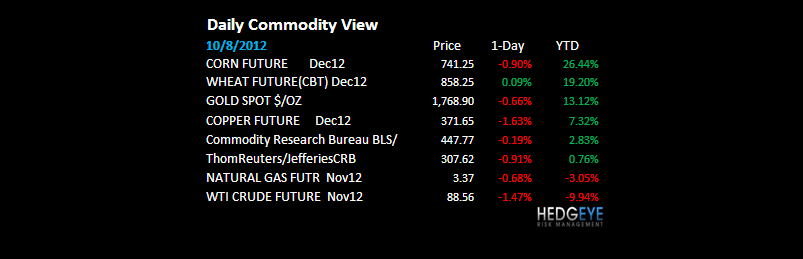

OIL – get the EUR/USD right, you’ll get a lot of things Oil right; Brent remains under big league pressure post the Bernanke Bubble top (Sep 14 for Commodities, which we’ll host a call on at 130PM today – Q4 Macro Themes) and after breaking its long-term TAIL line of $112.45/barrel support. Copper -1.4% this morn also failed at $3.95 TAIL risk resistance as well.

- Oil Declines a Second Day on Economic Outlook for Europe, Asia

- Hedge Funds End Rout as Prices Reach Two-Month Low: Commodities

- Traders Eye Grains Rebound as Supply Set to Tighten Post Harvest

- German 2013 Power Declines as European Coal, Carbon Permits Fall

- 5 Asia Fuel Oil Discount Shrinks; Vitol Buys Gasoil: Oil Products

- U.K. Within-Day Natural Gas Trades Near Highest in Two Weeks

- Brent-Nymex WTI Crude Oil Spread Widens to Near One-Year High

- Coffee Falls on Dollar as Brazil’s Trees Flower; Sugar Drops

- Iron-Ore Swaps Rise as Chinese Buyers Return After Holidays

- Palm Oil Drops for First Time in Four Days as Stockpiles Advance

- China Benchmark Coal Price Rises for First Time in Five Weeks

- Bullish Gas Wagers Climb First Time Since July: Energy Markets

- Ghana’s Gold Rush Sparks Conflict With Illegal Chinese Miners

- Hedge Funds End Rout as Prices Decline

- Palm Oil Exports From Indonesia Set to Sink Most in Four Months

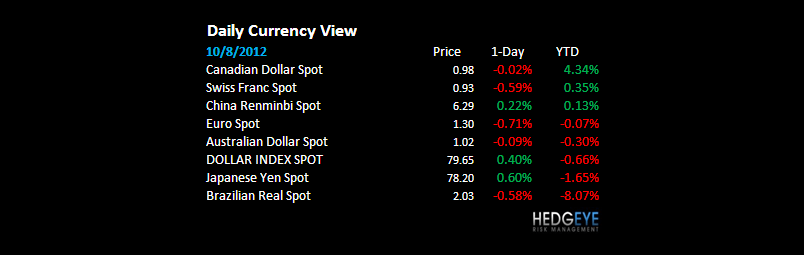

CURRENCIES

EUROPEAN MARKETS

ITALY – Greece is back, Spain to be saved, and Italy? Oh my goodness is the storytelling in Europe getting good – meanwhile Italy leads losers -1.7% this morning after snapping its immediate-term TRADE line of 15,866 3 wks ago – when will they ask?

ASIAN MARKETS

ASIA – after such a “great” US jobs report, you’d think the world would go straight up – nope; bad jobs report underneath the hood has USA close on the lows and Asia open/close weak across the board: Singapore -1.1%, India -1%, Indonesia -1%, etc.

MIDDLE EAST

The Hedgeye Macro Team