Los Angeles and other California cities are running out of gasoline due to a shortage of supply in the area, driving prices 45 cents higher to $5/gallon at some stations. It doesn’t help that some major refineries at Chevron (CVX) and ExxonMobile (XOM) are under both planned and unplanned maintenance.

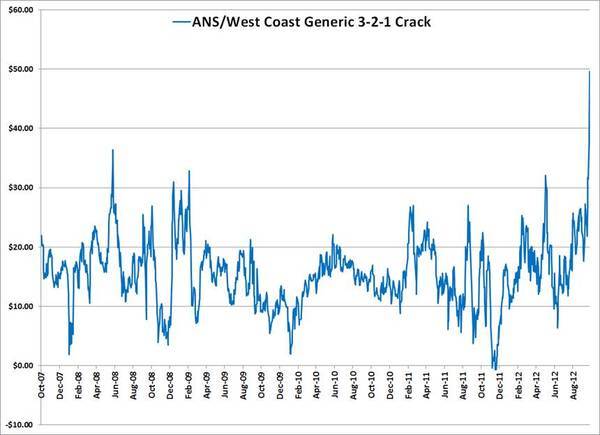

Tesoro (TSO) stands to benefit from the shortage in the near-term as the ANS/USWC 3-2-1 crack is at $50/bbl (see below). The massive spike that took it from under $30/bbl to $50/bbl is where the money is. Short-term bonuses aside, the pain at the pump could lead to negative backlash from the press for TSO at a time when the company is trying to acquire a California-based BP refinery. Should the FTC block the deal, TSO’s stock will likely take a meaningful hit.