Jobless Claims - Small Step Backward

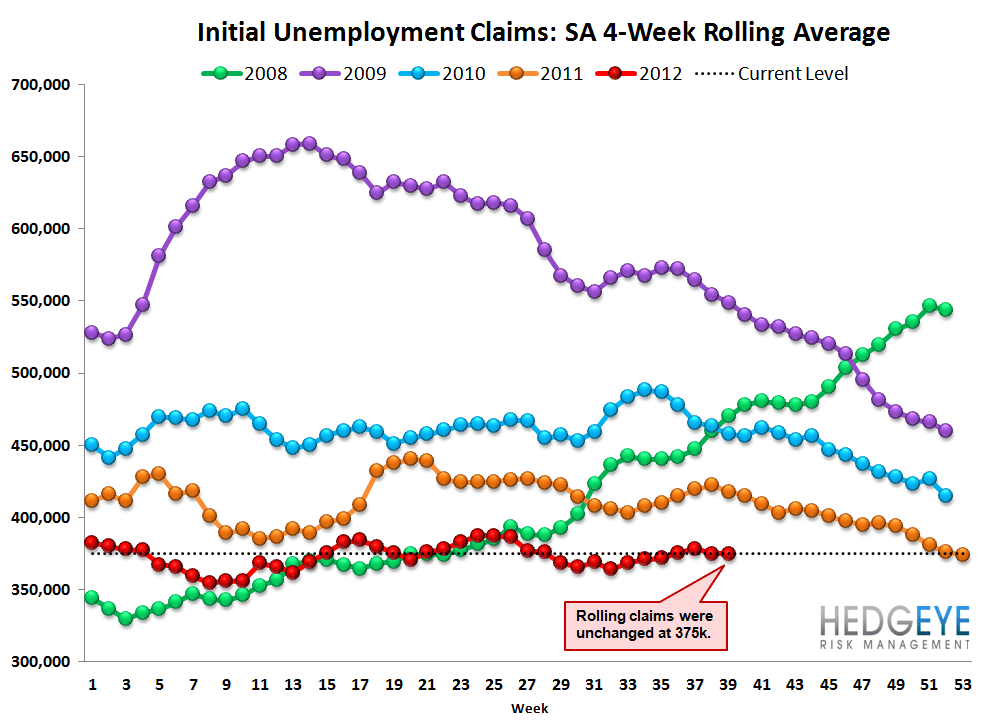

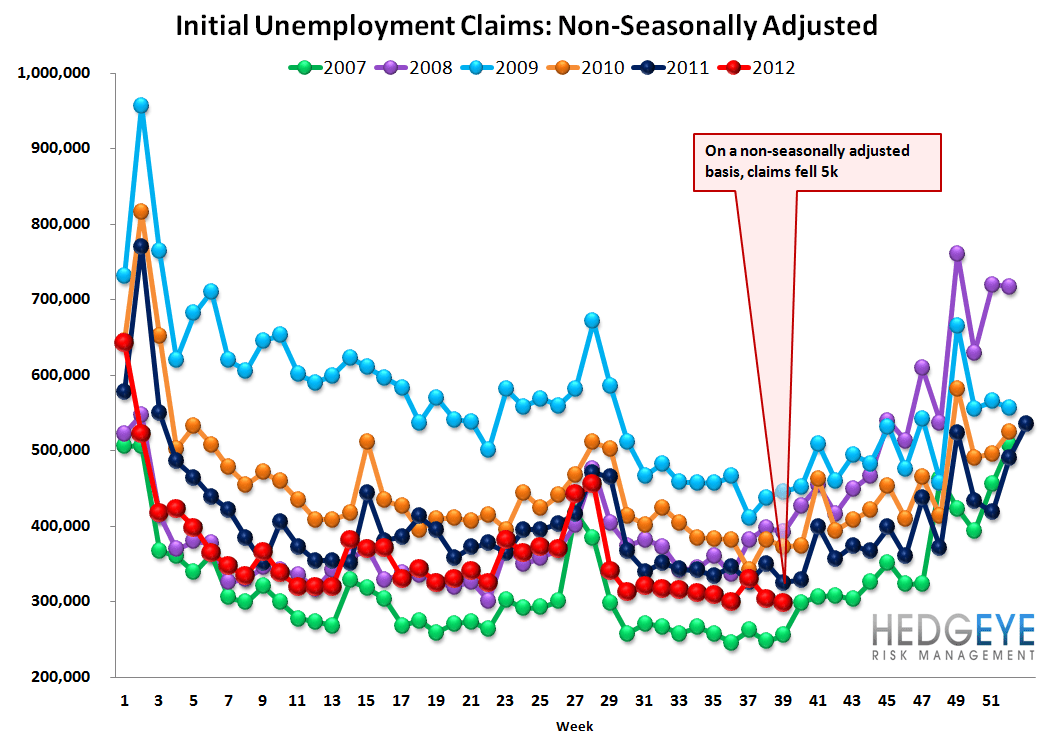

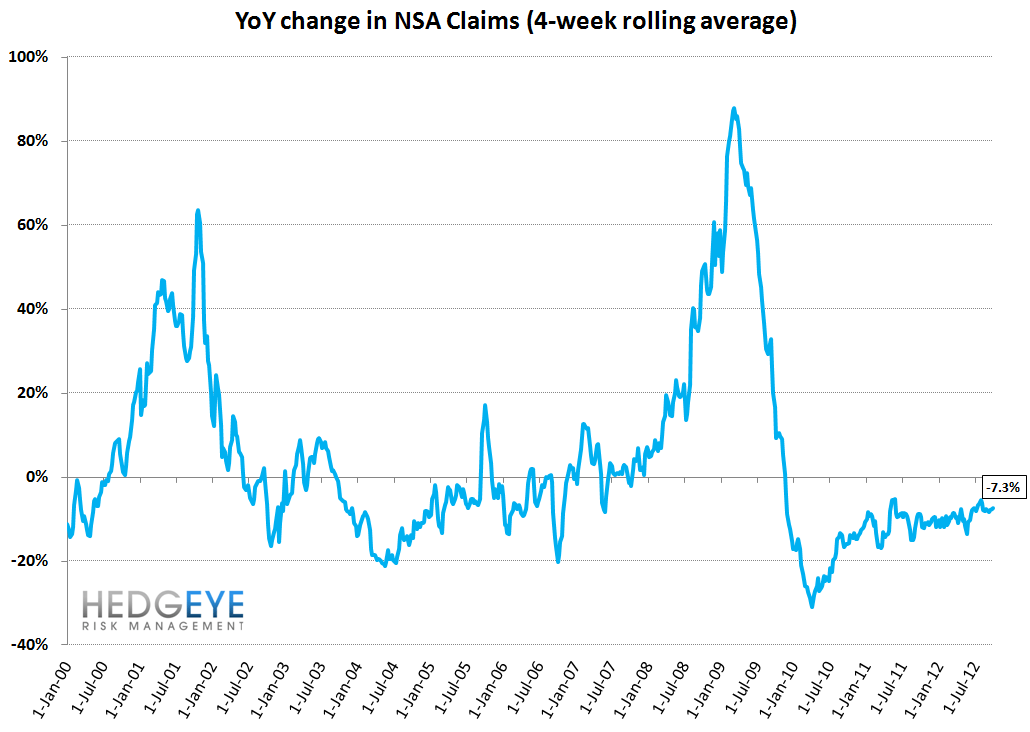

Initial claims rose 8k last week to 367k but after incorporating the upward revision to the prior week's data, rose only 4k. Rolling claims were unchanged at 375k. On a non-seasonally adjusted basis, claim were 5k lower than the prior week, ending at 299k. Last week, the rolling NSA YoY series weakened from -7.7% YoY to -7.3% YoY. The rate of improvement in claims has been slowing since early 2010. We like to look at the rolling NSA series on a YoY basis because it removes the effects of seasonality. For reference, this morning's print was slightly lower than consensus expectations for 370k.

Overall:

Over the coming months we expect jobless claims to benefit from distortive seasonality tailwinds. In the first chart below we show how the claims series trends lower from September to February and goes sideways or higher March through August. We expect that 2012 will play out similarly to the last three years. That said, it will be important to monitor the YoY change in the rolling NSA series going forward. If we continue to see the rate of improvement slow, this could offset some of the effects of the positive seasonal distortion.

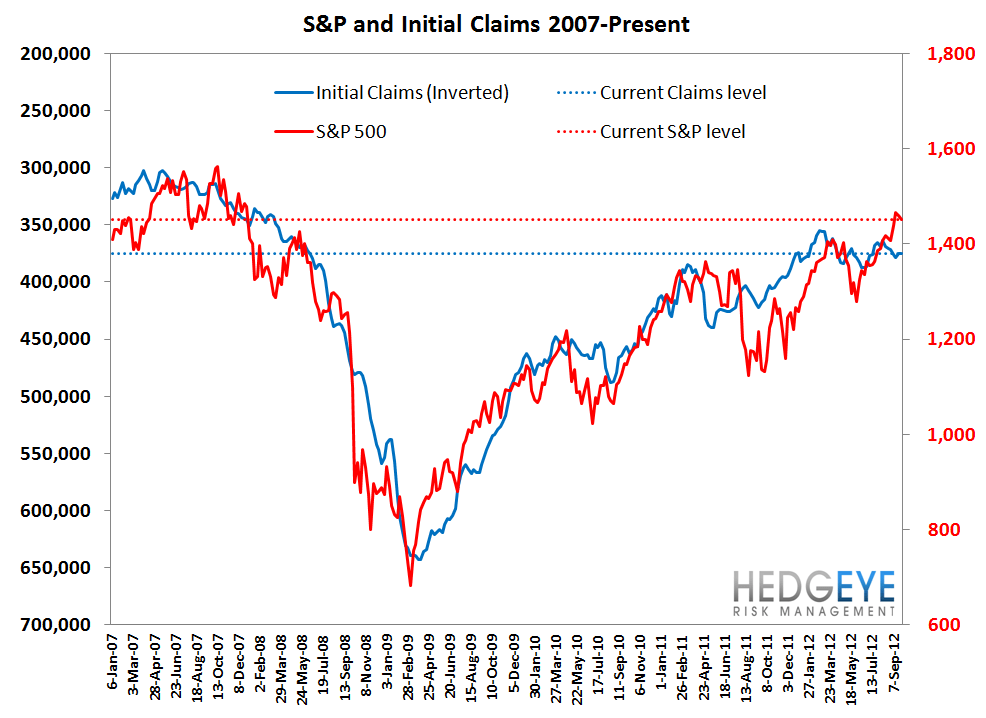

Another important relationship to monitor is that of the S&P and claims. These two series move together over the long-term but tend to see short-tern divergences. The current level of claims now implies an S&P level of 1348, which is 7.1% lower than the most recent S&P print .

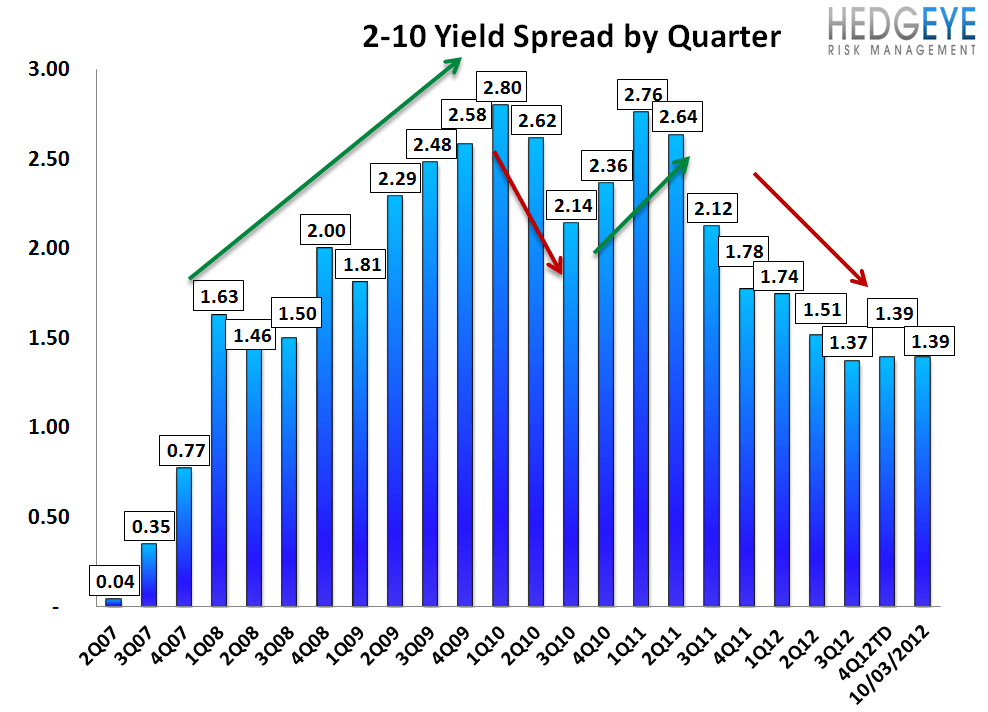

Yield Spreads

The 2-10 spread rose 3 bps WoW. 4QTD, the 2-10 spread is averaging 1.39%, which is up 2 bps basis vs 3Q12.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over multiple durations.

Joshua Steiner, CFA

Robert Belsky