TODAY’S S&P 500 SET-UP – October 4, 2012

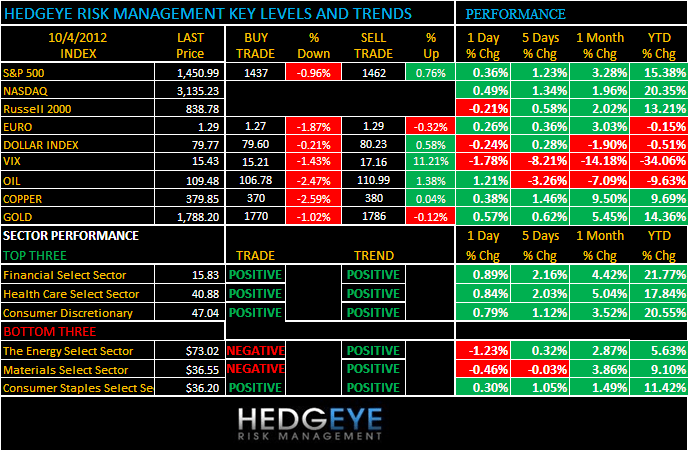

As we look at today’s set up for the S&P 500, the range is 18 points or -0.96% downside to 1437 and 0.76% upside to 1462.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 10/03 NYSE -2

- Decrease versus the prior day’s trading of 196

- VOLUME: on 10/03 NYSE 665.91

- Increase versus prior day’s trading of 11.68%

- VIX: as of 10/03 was at 15.43

- Decrease versus most recent day’s trading of -1.78%

- Year-to-date decrease of -34.06%

- SPX PUT/CALL RATIO: as of 10/03 closed at 2.55

- Down from the day prior at 2.56

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 26.63

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.63%

- Increase from prior day’s trading of 1.61%

- YIELD CURVE: as of this morning 1.40

- Up from prior day’s trading at 1.38

MACRO DATA POINTS (Bloomberg Estimates)

- 7am: Bank of England announces interest rates

- 7:30am: Challenger Job Cuts Y/y, Sept. (prior -36.9%)

- 7:45am: ECB announces interest rates

- 8:30am: ECB’s Draghi holds news conference

- 8am: RBC Consumer Outlook Index, Oct. (prior 50.4)

- 8:30am: Jobless Claims, Sept. 29 est. 370k (prior 359k)

- 9:45am: Bloomberg Consumer Comfort, Sept. 30 (-39.6)

- 10am: Factory Orders, Aug. est. -5.9% (prior 2.8%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas storage change

- 11am: U.S. to announce plans for sale 3-yr, 10-yr, 30-yr debt

- 11am: Fed to purchase $1.75b-$2.25b notes due 2/15/2036-8/15/2042

- 2pm: Fed issues minutes of FOMC Meeting

- 8pm: Fed’s Bullard speaks in Memphis, Tennessee, on economy

GOVERNMENT:

- SEC member Daniel Gallagher, three officials from agency’s trading and markets unit speak at Sifma market structure conference in New York. 8:45am

- Cheniere Energy, Royal Dutch Shell, GDF Suez join U.S. Energy Association at conference on global supply. 9am

WHAT TO WATCH:

- Euro-area, England central banks to keep interest rates at record lows, economists say

- U.S. same-store sales seen slowing in Sept. from August gains

- Romney debate tactics may put campaign against Obama ’back on track’

- U.S. shopping center demand slows as consumer spending stalls

- U.S. consumer credit delinquencies near 6-yr low, bankers say

- AT&T said to add first Nokia Windows 8 phone for US market

- Unilever said to put Skippy peanut butter brand up for sale

- Teva pulls depression drug generic after FDA says not same

- Spain meets maximum target at bond auction as 3-yr yield rises

- 3M scraps Avery label-unit deal as antitrust regulators balk

- Applied Materials to cut 9% of workforce amid slump

EARNINGS:

- International Speedway (ISCA) 7am, $0.08

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Rises From Biggest Drop in Three Months on Syria Conflict

- Overlander Leads Sucden to Metals-Trading Dominance

- Morgan Stanley Backs Gold, Silver, Copper on Demand Outlook

- Palm Oil Set to Drop After Rebound on Indonesia Tax, Mistry Says

- Copper Gains in New York as Higher Equities Boost Demand Outlook

- Soybeans Gain a Second Day as Price Drop May Boost Import Demand

- Sugar Climbs to Seven-Week High on India’s Imports; Coffee Gains

- Pan Pacific Said to Offer 15% Cut in Copper Premium for China

- World Food Prices Jump to Six-Month High as Dairy Costs Rise

- Iron-Ore Swaps Rise 1.4% in London Trading, Clarkson Data Show

- Aluminum May Climb to $2,200 on Fibonacci: Technical Analysis

- Bottom in Coking Coal Price Rests on Supply and Demand Response

- Danube Decay Hinders Rhine Link to Leave Shippers Blue: Freight

- Gold Jumps in New York on Signs of India’s Demand, Weaker Dollar

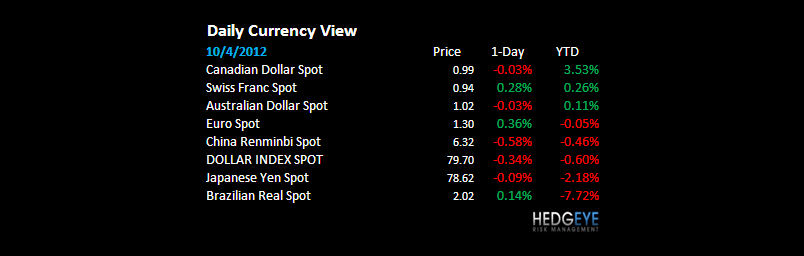

CURRENCIES

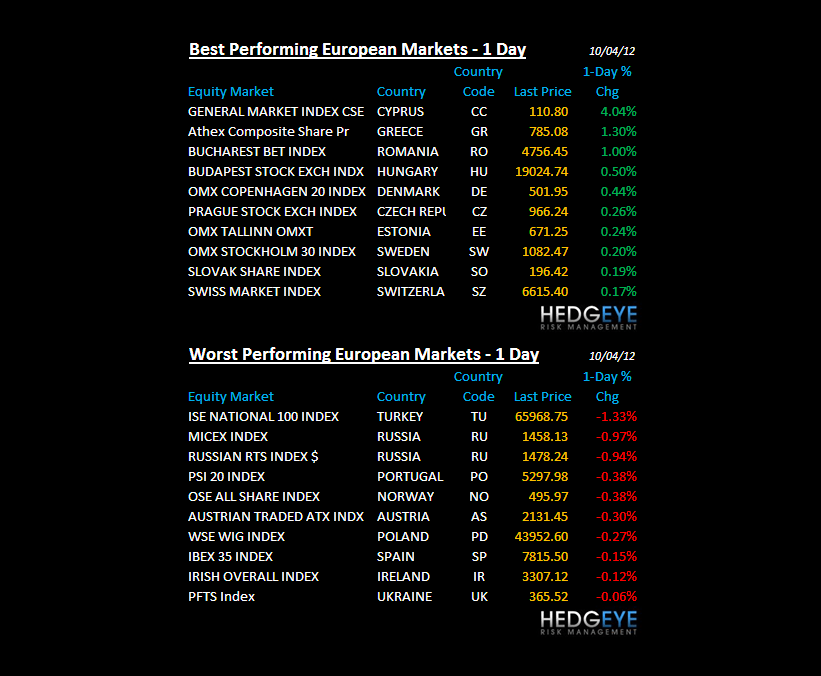

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team