This note was originally published at 8am on September 14, 2012 for Hedgeye subscribers.

“Two things are infinite: the universe and human stupidity. And I’m not sure about the universe.”

-Albert Einstein

As much as we and other market prognosticators (and even trained economists) have criticized Chairman Bernanke’s monetary policies, he went ahead yesterday and put on the big boy gloves of monetary policy. In the Fed’s statement yesterday, quantitative easing was, as Buzz Light Year would say, extended to infinity and beyond.

In using the Einstein quote above I’m not suggesting anyone on the Federal Reserve board is stupid. In fact, they are obviously all very intelligent. While I would give myself the odds in a game of hockey, I’m pretty sure anyone on the Fed could beat me in a game of one-on-one Sudoku (if that even exists). Of course, what they may be missing is the impact of their policies on the real economy.

After Keith got off CNBC’s Fast Money last night, he and I had a long discussion about the quarter. Let’s be honest, we’ve been leaning too bearishly this quarter. Coming into the quarter, we actually believed that the Fed would be in a box because the data didn’t currently support incremental easing and that the Fed wouldn’t ease ahead of the election. Obviously, we were wrong on both those points.

Conversely, we’ve been spot on in terms of our view on general economic growth this quarter and this year. Ultimately, economic activity will drive both company fundamentals and the broader stock market. In the shorter term, of course, other factors can override these fundamentals.

So while we weren’t levered long in to this new market high (in fact, we are actually short the SP500), our risk management process has also enabled us to not have major blow ups. Step #1 for us is always to minimize our losses. Start by not losing money, and you will get your shot to generate returns.

A popular refrain yesterday in the media and around some areas of Wall Street was that Bernanke and the Fed are the only ones focused on doing anything about the abysmal jobs market. I have to admit, I find this view a little nonsensical. From a practical sense, printing money does very little to encourage companies to hire. Further, it has actually done very little to encourage banks to lend more broadly.

On the last point, and I will admit this is anecdotal, I ran into a friend who is one of the larger real estate developers and condo owners in a small New England city. I assumed that extending the duration that rates will be held at 0% and further monetizing of MBS would be beneficial for those in real estate. His response was that I was right, for those that can get a loan this is a very good thing. But, according to him, for the large percentage of the population who doesn’t have a 20% down payment or stellar credit rating, it is far less relevant. On some level, this likely explains why mortgage applications have not accelerated with rates at all-time lows.

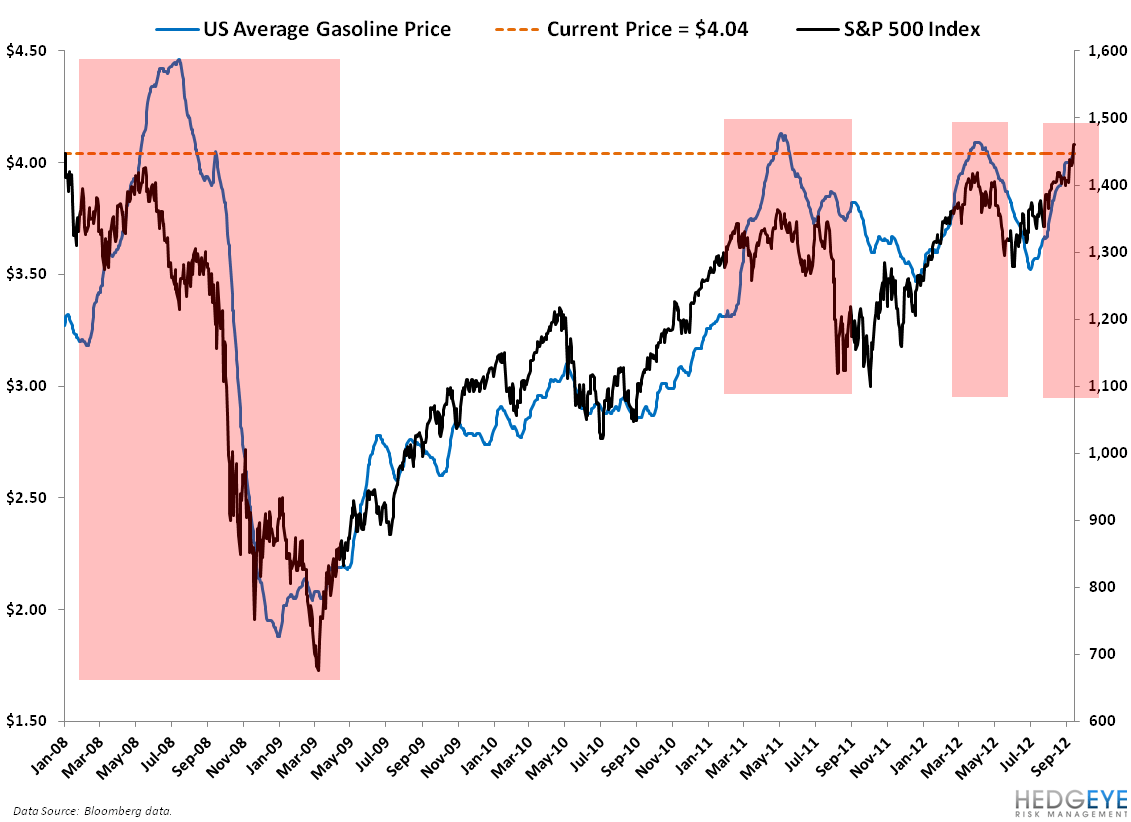

The most critical economic issue with printing dollars to infinity and beyond is the inflationary impact. Ironically, shortly before the Fed released its statement yesterday, PPI hit a three year high in terms of month-over-month growth. But forget that spurious government data, what about the real economy you say? Well, in the Chart of the Day today we actually looked more closely at the impact of commodity inflation on the real economy.

As the chart shows, going back to 2008 gasoline has exceeded $4 in mid-2008, in mid-2011, in early 2012, and now. The corresponding result, as the chart shows very vividly, is that economic growth slowed and we then saw a corresponding correction in equities, despite infinitely loose monetary policy.

Not to scare you this morning, but inflation from these levels shifts our growth slowing scenario squarely into potential recession territory. We don’t use the R word frivolously. In fact, the last time we emphasized recession as a probable scenario was back in March of this year.

Whether we get aggressive on the recession call will be data dependent, but we are comfortable continuing with the idea that global growth is slowing. In this vein, later this morning we will be doing a 15-minute call on Caterpillar Inc. (CAT) outlining our long-term bearish thesis. Our Industrials Sector Head Jay Van Sciver is relatively new to Hedgeye, but hasn’t been afraid to make a bold call. This one will be no different. The key tenets of his thesis on CAT are as follows:

- Resource company investment is near cyclical highs and set to decline. Other end markets do not appear poised to replace this tailwind;

- CAT has been adding capacity and building inventory into what we believe will be a peak in demand; and

- Our cyclically adjusted valuation for CAT implies a stock price range of $50 – 70.

This is going to be a quick call with a lot of data, so grab a coffee and join us at 11am. If you are an institutional subscriber and don’t have the dial in, please email sales@hedgeye.com and we will get it to you.

Before I let you head into this weekend, the other point related to extending QE to flag is that if equity markets continue to inflate, it will likely be positive for President Obama’s re-election chances. To wit, our Hedgeye Election Indicator has his chances of re-election at an all-time high at 61.9% and this corresponds closely with InTrade at 64.5% odds.

Incidentally, if you are confused by the global economy, you are in good company. In his most recent letter to investors, legendary investor Howard Mark writes that the “world seems more uncertain than any other time in my life.”

Indeed.

Our immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1721-1779, $114.49-118.01, $79.04-80.67, $1.27-1.30, 1.70-1.80%, and 1427-1463, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research