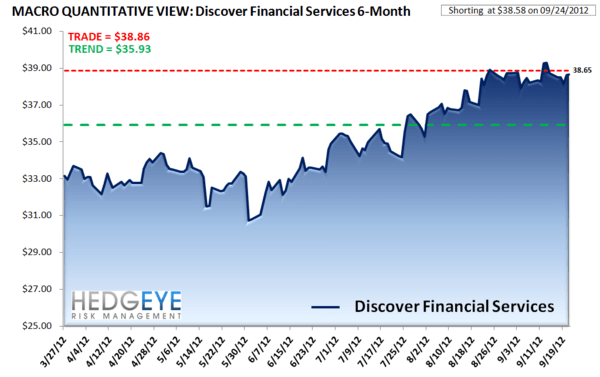

In the past, we’ve been too bearish on Discover Financial Services (DFS). The stock has had a fantastic run and we simply timed the cycle prematurely, thinking that delinquency rates were stacked against the long side. Cycles come and go and when you look at the loss of value for some companies in the past, it’s easy to be bearish. In the last cycle Discover lost 83% of its value, Capital One lost 90% and American Express lost 84%.

With DFS reporting on Thursday, we’ve shorted DFS in our Real Time Positions as the numbers finally add up on a quantitative basis. We expect a year-over-year negative trend in EPS and think the company is running on fumes at this point.