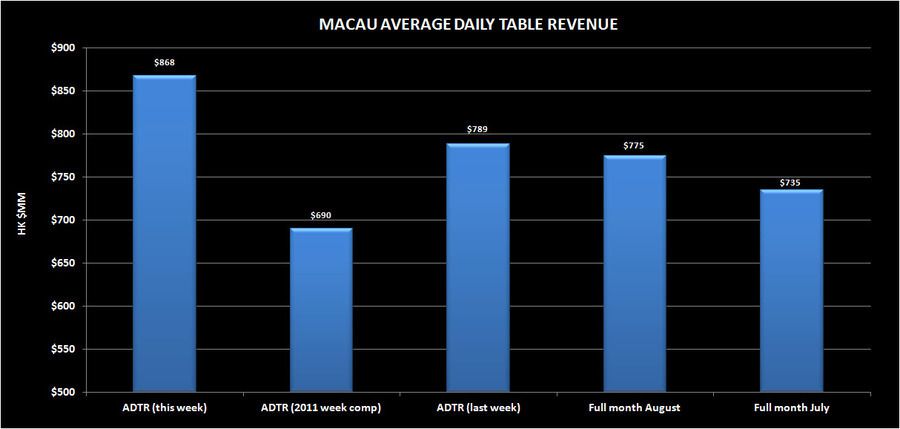

While Vegas struggles to recover, Macau is picking up the pace with strong numbers being put up over the previous week. Average daily table revenues are up 26% year-over-year, 10% over the prior week, and was 12% higher than August. Big money is coming into play, drawing in HK$868 million per day on average. With these numbers, you can see why we remain bullish on Macau-focused gaming stocks.

Also worth noting are hold trends for the casinos in Macau. For those of you who are unfamiliar with the term, hold is the measure of the amount of money a casino table game keeps from the total amount of money that is dropped into the cash box. LVS’ share is climbing back towards normal and MGM is having above trend for the month.