Conclusion: There are too many factors helping out the top line and margins to get bearish…at least not yet. But watch the CEO’s stock sales…he’s good.

Keith pinged us yesterday on GIL, as it started to look like a short based on his models. True to our process, we re-evaluated the fundamental case to see where it stands vis/vis price (they’re often two very different things). This is one of those times where we told him to focus short efforts elsewhere, as it is likely another two quarters before the fundamentals will likely line up with a bearish stock call.

Here’s a quick review of the primary financial drivers – Revenue, Margins, and Cash Flow.

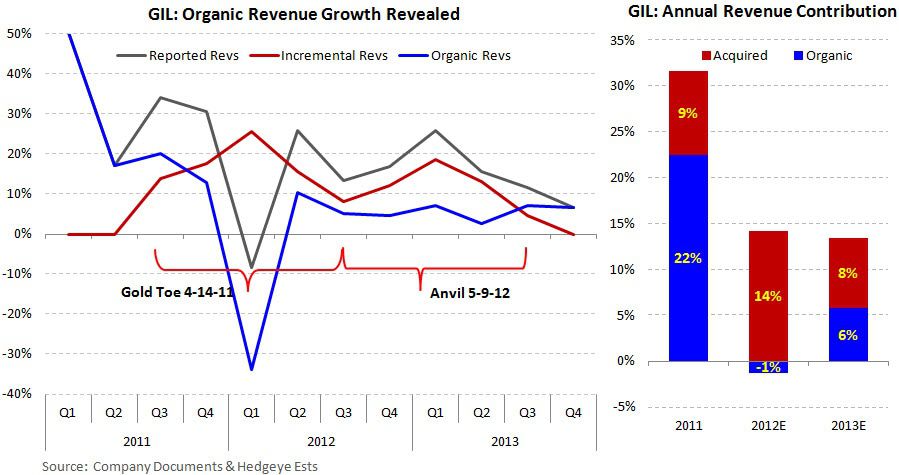

Revenue: The setup is getting easier near term. Just as GoldToe anniversaries, Anvil revs layer on and will manufacture double-digit revenue growth alone. After the upcoming quarter, the setup is very favorable with GIL up against devaluation discounts of last year. Post FQ1, organic revenue growth will be more challenging to manufacture with the company now representing over 71% of the U.S. Distributor market forcing them to rely more heavily on building Branded Apparel, which is uncharted territory and away from management’s core expertise. Barring another acquisition (which we wouldn’t put past them) following FQ2, revenue growth should slow meaningfully as the benefit of recent deals will have passed, and the share gain from Hanesbrands jettisoning its screenprinting business will have ebbed.

Margins: This setup is also very favorable near-term as GIL starts to lap cotton prices as well as manufacturing downtime and inventory devaluation that will add 300-400bps of margin alone. GIL also posted a positive Sales/inventory spread in 3Q for first time in six quarters, which is gross margin bullish near term.

Cash Flow: Favorable. CapEx coming down after two years of higher spending to grow retail, open a new DC, another manufacturing facility, and revamp several existing manufacturing facilities to lower operating costs. Increased spending over the last two years at 9%-10% of sales should ease CapEx requirements for the next 2-3 years

Sentiment: Definitely mixed signals here, with short interest down to 3% of float (it’s been as low as 2%) and the sell-side generally positive as well. But on the flip side, CEO Glen Charmandy recently filed a 10b5-1 plan to sell up to 2.75mm of his 9.8mm shares of GIL stock. While these 10b5-1 plans are ‘at arm’s length’ and are executed by a third party, it’s usually a wise move to pay attention when the CEO of a company registers an intent to sell 28% of his stock – especially when it’s a CEO that has had such a great track record in capital preservation on stock sales.