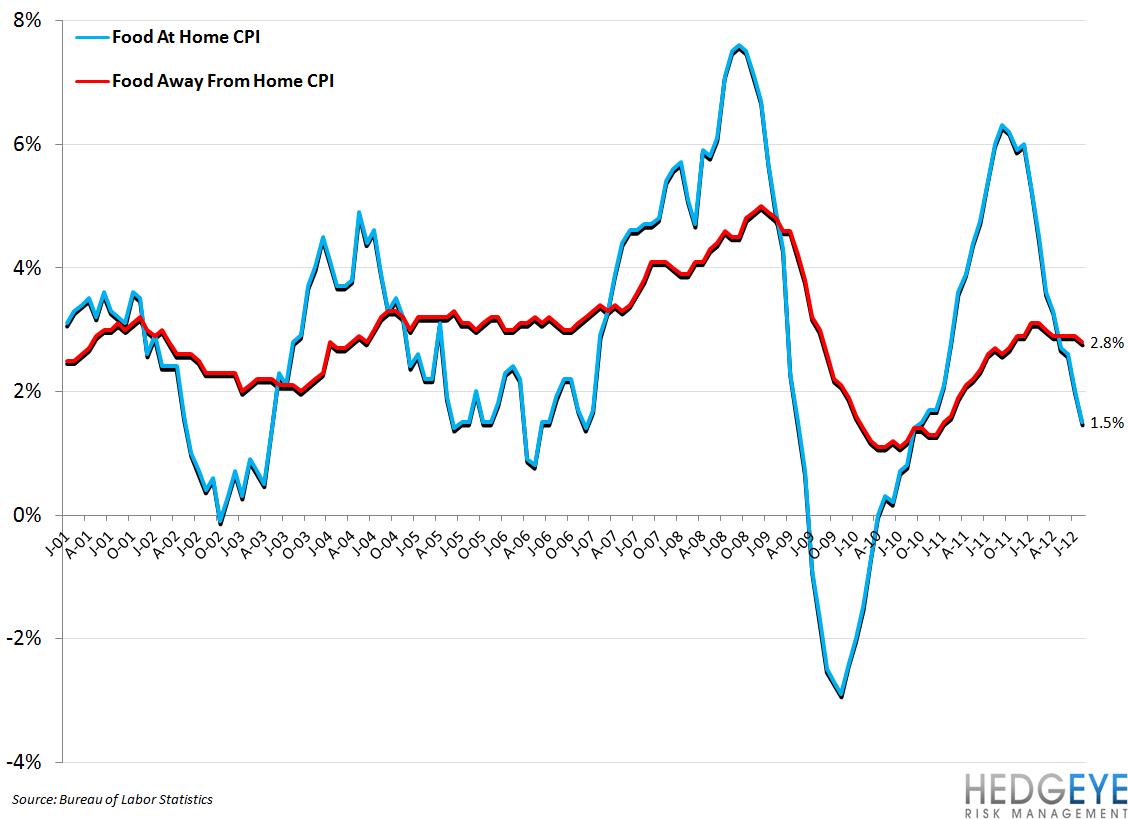

The Bureau of Labor Statistics released CPI data for the month of August this morning. The spread between CPI for Food at Home versus Food Away from Home continues to grow. Inflation in the restaurant check is far-outstripping inflation in the grocery aisle.

We have long been calling out this trend; the advantage that restaurants enjoyed over grocers in 2011, in terms of lower price increases year-over-year, continues to fade. Grocers were forced to raise prices in line with inflation to protect margins during 2011; we believe that restaurants benefitted from that. Last year, restaurants’ strong top-line trends helped the industry mitigate the impact of inflation on margins but, it seems, this year pricing power is much-diminished. Even McDonald’s is running price at roughly 3% in the United States.

Casual Dining

Using a “Restaurant Value Spread”, which is the basis point spread between CPI for Food at Home and CPI for Food Away From Home, we believe we have a good indicator of the traffic cycle for many casual dining brands. This is not a complicated theory; when inflation at the grocery store is far in excess of inflation at the restaurant, people are more likely to skip the grocery store and eat at a restaurant. We will be publishing on this in more detail over the weekend/early next week but our initial take is that the collapsing Restaurants Value Spread is bearish for casual dining traffic and comps (Knapp). The relationship is quite strong.

Darden

Looking at the first chart in this note, above, it seems that the value spread has more room to decline. Darden’s Red Lobster, in particular, could be facing a difficult environment if the current Restaurant Value Spread cycle has similar amplitude to the last. In addition, consensus estimates (quarterly so not shown here) from Consensus Metrix suggest that the Street is anticipating a quick rebound for Red Lobster comps. We do not think that is going to happen; the Restaurant Value Spread is likely to decelerate for another 6-9 months.

Please reach out if you want to discuss this in greater detail or in the context of other names within the restaurant space.

Howard Penney

Managing Director

Rory Green

Analyst