This note was originally published at 8am on August 27, 2012 for Hedgeye subscribers.

“Bear banger is a slang or colloquial term sometimes used to describe exploding projectile wildlife deterrents.”

-Ursus International

Bear spray or bear banger? When you go for a run down by the McCullough Lake House in Northwestern Ontario, what do you use? Inquiring Risk Manager minds want to know.

After running up to a bear during our family vacation last week, my wife Laura asked the original Thunder Bay Bear (my Dad) for some reinforcements. Instead of the go-to bear mace that most locals use, he opted to buy her something that makes noise.

The twist on the noisemaking part is that Bear Bangers sound more like a shotgun than a firecracker. I wouldn’t put a loaded one in your running shorts.

Back to the Global Macro Grind…

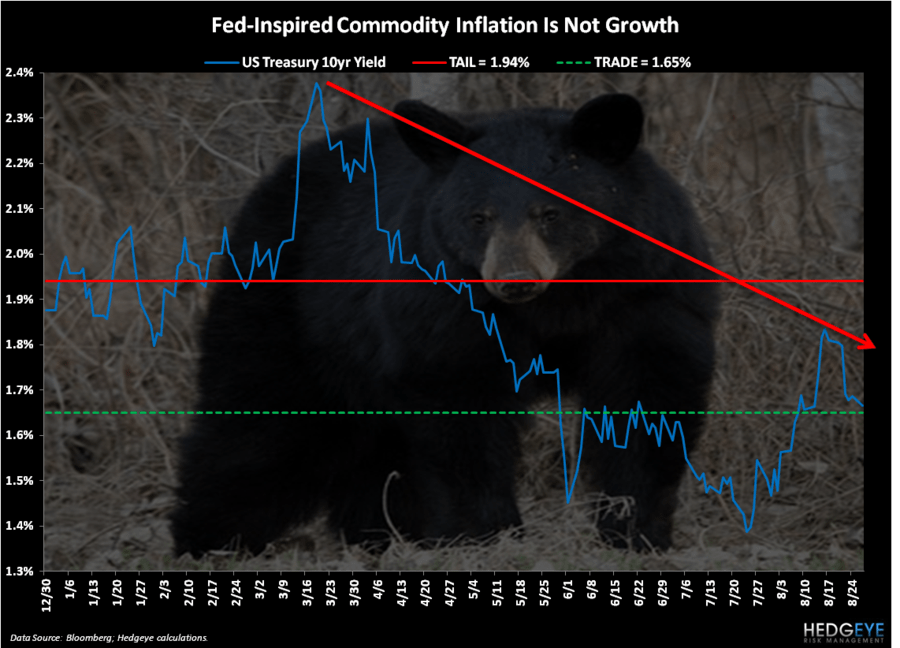

Running from your US or European Equity shorts at last week’s short covering highs was not a good risk management idea. Neither was selling your Fixed Income exposures at last week’s lows. Bear Banging works, but your timing matters.

Last week’s intra-week high for the SP500 was 1426. The intra-week low for 10-year US Treasury Bonds was close to 1.90%. However, those weren’t closing highs and lows. And it’s closing prices that matter most in our globally interconnected macro model.

From those no-volume intraday levels to the other side of the risk management trade:

- SP500 dropped a full -2% to 1398 intraday on Friday morning

- 10yr US Treasury Yields dropped just over -10% to close the week at 1.69%

So, I covered all but 4 shorts in the Hedgeye Portfolio at 1398 and sold almost 50% of our Fixed Income Exposure in the Hedgeye Asset Allocation Model week-over-week.

For those of you who are new to what we do, the Hedgeye Portfolio and the Hedgeye Asset Allocation Model are 2 mutually exclusive risk management products.

The Hedgeye Portfolio is simply a real-time idea list of risk managed long/short ideas that focuses on Rule #1 (don’t lose money), whereas the Asset Allocation Model attempts to be more dynamic than the Old Wall’s 60/40 stocks/bonds thing.

As time and prices change, we do.

When confronted with a live bull or bear, sometimes you have to move fast; sometimes you don’t have to move at all. If you’ve survived the last 5 years of this whipsaw, you get that the only perma you need to be is permanently flexible.

To be clear, I wouldn’t dare set foot in the Shuniah dump pit with a baby black bear (and no mama bear in sight) inasmuch as I’d short-and-hold stocks into a central planning event at Jackson Hole…

Being bearish on bonds at last week’s bottom was as bad a decision as buying last week’s 1426 top in US stocks. Being bearish on bonds means you believe growth isn’t slowing. Being bullish on stocks, at any price, just means you don’t sell on green.

Being bullish on commodities up here is something that I am not. While Bernanke claims “price stability and full employment”, what’s really happening here is that people are front-running him, getting all lathered up in what slows real (inflation adjusted) consumption growth (rising commodity prices).

Got causality? Last week’s CFTC (Commodities Futures Trading Commission) data revealed an all-time high in outstanding futures and options contracts:

- Week-over-week gain in total contracts of +10% to 1.32 million (eclipsing the Feb/Mar 2012 highs)

- Gold contracts were up a stunning +35% wk-over-wk to 110,623

- Oil contracts were up another +18% wk-over-wk to 179,526

Fed inspired (US Dollar Debauchery) commodity inflation is not growth. It slows growth. And when this entire centrally planned game of Bailout Begging ends, the 3rd of the Greenspan/Bernanke asset bubbles (commodities) will be in for one heck of a Bear Banger.

Our immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yields, and the SP500 are now $1634-1679, $112.31-115.87, $81.16-82.11, $1.23-1.25, 1.65-1.76%, and 1398-1419, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer