Position: Short the euro via FXE.

As many of you know, our firm is set up like a buy side firm in order to match up better with many of our subscribers. In essence, our analysts cover a broader swath of names and try to go to where the opportunities are rather than just publishing maintenance research. As well, we encourage vigorous debate about ideas.

On the last point, this morning was no exception as we spent a good twenty minutes debating and discussing the euro. A key consideration is whether the outlook for the euro has dramatically changed with the recent policy pronouncements from the European Central Bank. To start, let’s consider the new policy.

At the press conference following the ECB monthly meeting President Mario Draghi told reporters:

“We want this to be perceived as a fully effective backstop.”

Ultimately, what that means practically is important, but from a perception perspective the markets are clearly looking at this as the ECB committing to unlimited bond purchases from the periphery. The string attached to this commitment by the ECB is that governments sign on to a euro-zone plan for budgetary discipline.

Budgetary discipline in the European Union is, of course, not a new concept. In fact, the very origin of the European Union via the Maastricht Treaty outlined some key elements of budgetary discipline. As it relates to government finance there were two key goals: 1) annual government deficit not to exceed 3% of GDP and 2) gross debt to GDP not to exceed 60% of GDP. We know how that ended.

Perhaps budgetary discipline will be different this time in Europe, although we won’t know for sure without understanding the enforcement mechanism. As a result, Europe may well be left with a situation where there is an unlimited commitment by the ECB to back stop the sovereign debt market, but the fiscal outlook never meaningfully improves. In terms of outlook for the euro currency, this scenario seems likely to lead to fundamental weakness. Ironically, in free markets the interest rate is the mechanism which penalizes countries with poor fiscal discipline.

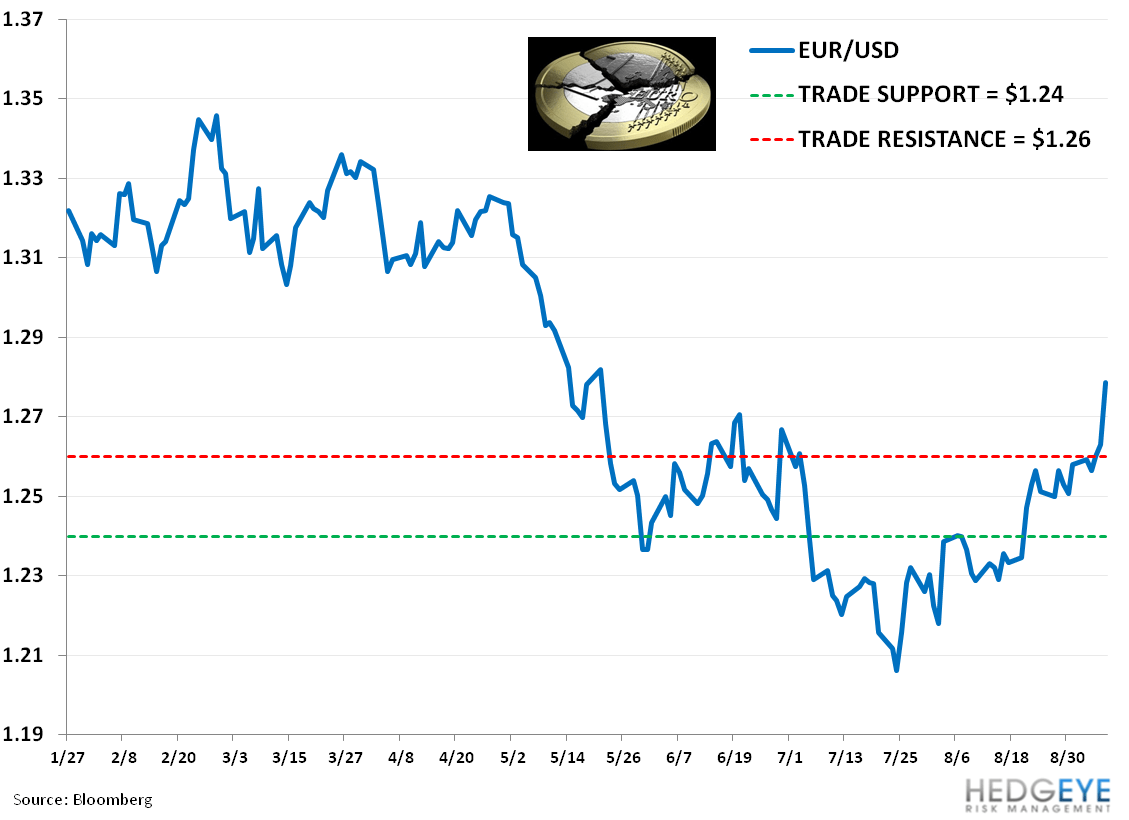

The obvious question, then, is how we explain the current move upwards in the currency. To put it simply, it looks like a short squeeze. In the chart below we highlight the net futures positions in the euro going back to 2008. The obvious takeaway is that the early summer of 2012 was the most heavily shorted position of the euro since the European sovereign debt debacle began.

Not surprisingly, as the chart below highlights, the euro bottomed roughly around the time that short interest reached its highest point, or shortly thereafter, and the euro has been climbing as the shorts have continued to cover. The climb itself has been gradual, though the last few days highlight a fairly typical short squeeze as the shorts have scrambled to cover due to the latest policy pronouncement.

It is certainly possible that the future for the euro is now bright. On some level that may be true, as the ECB actually seems committed to at least sustaining the currency. The fundamental drivers of the currency, though, continue to paint a bearish outlook for the euro based on our analysis. For starters, money printing is bearish for any currency and the ECB has now indicated the printing press is open 24/7 for business. We highlight the balance sheet of the ECB below, which is already in a precarious position and now only set to expand further.

The other consideration for the euro is the actual economic outlook for Europe. We haven’t minced words on our view of global growth slowing and Europe has been the poster child for this as the chart below highlights. The one benefit in coming quarters may be easy comparisons for economic activity in Europe, but the PMI readings from Europe remain consistently below 50 and actually imply continued contraction in Europe.

So on one hand, the ECB’s commitment to completely backstop bond purchases is certainly a positive for those peripheral nations that are inclined to continue to issue debt with wanton abandon. On the other hand, even if it does signal a willingness to keep the euro intact, we do not see printing money as a factor that leads to a strong currency. Underscoring all of this is a European economy that continues to deteriorate. A fact that implies a return to ZIRP is likely to happen sooner rather than later. Once again, negative for the currency.

The other side of the euro is our outlook for the U.S. dollar. For purposes of this note, we won’t get into the prolonged analysis of the U.S. dollar, but a few things are positive for the dollar versus the euro. First, the outlook for economic growth in the U.S. is more positive than in Europe, even though it is somewhat tepid here as well. Second, one way or the other, government spending is set to decline in the U.S., likely via sequestration. Finally, there is a close to 50% probability that Romney becomes President and he has espoused a much more pro U.S. dollar policy (including replacing Bernanke).

As for now, we will stick with the view that short covering is the key driver of euro strength. At least until the fundamental outlook changes, or until our quantitative model supports it.

Daryl G. Jones

Director of Research