Beef was the outlier, versus other food commodities, over the last week as it gained 5.8%. Grains also dropped over the past week on Hurricane Isaac bringing rain to some, but far from all, states affected by drought in the U.S. However, it seems that downside may be limited as futures trading suggests that the market is betting on demand accelerating for grains on the back of the past two weeks’ price declines. Coffee prices continue to decline as supplies, on a global basis, seem abundant. Output in major coffee producing countries, such as Brazil, as well as inventory levels, are indicative of abundant supply which should help maintain a favorable cost environment for the coffee chains over the next year or so.

The Drought

Drought in the U.S. captured the attention of investors this summer as it drove grain prices dramatically higher. It seems that the knock-on effects of the drought are likely to be long lasting. The U.S. Drought Monitor’s latest weekly report was released this morning and indicated that Hurricane Isaac had brought some relief to some afflicted areas but others actually deteriorated over the last week. Oklahoma’s drought condition actually worsened. States towards the eastern part of the corn belt showed drastic improvement; nearly half of Arkansas was in the most extreme drought condition last week but, by this morning’s reading, that percentage is down to 12%. Illinois, Indiana, Kentucky, Missouri, and Ohio all saw improvements in drought conditions due to Isaac.

Where’s the Beef?

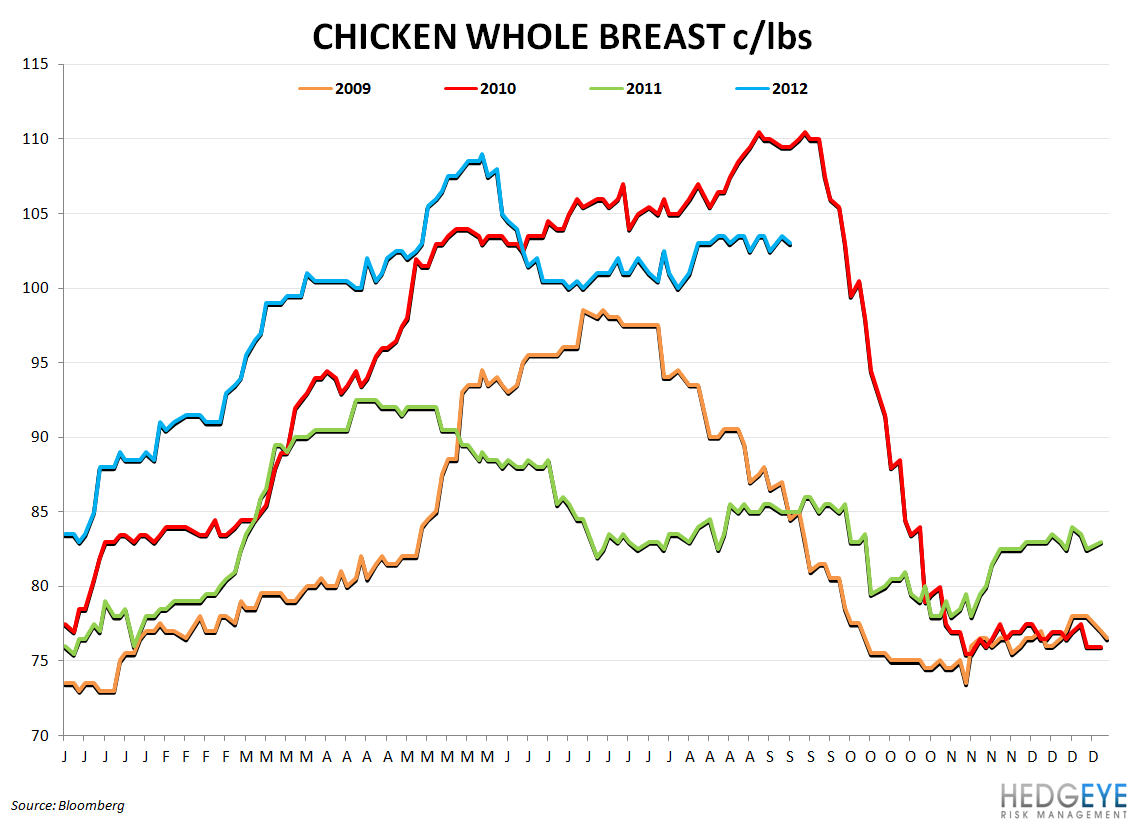

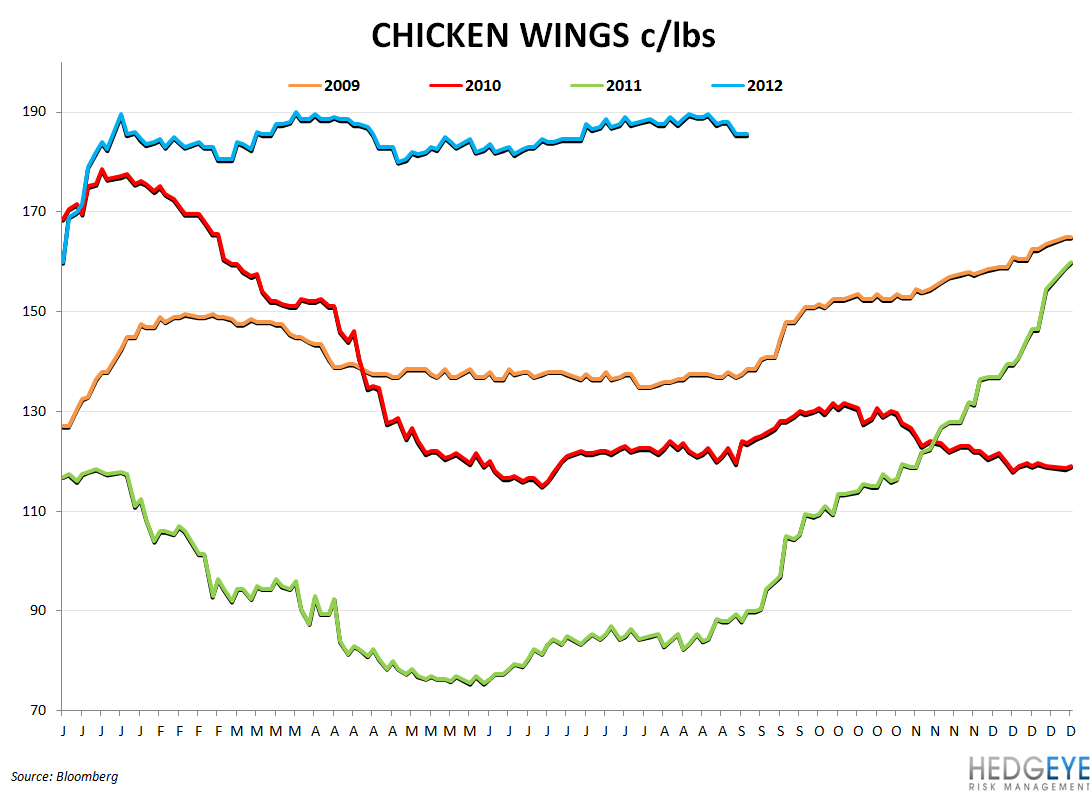

Last year’s drought had an impact on the supply of beef within the U.S. and, far from allow farmers to embark on the path to replenishing their herds, 2012 has proven to be even more challenging. Now, it seems more certain that livestock supply may be impaired for years as higher grain prices continue to take a toll on chicken, beef, and pork processors. Beef costs have not risen in step with grain prices as more cattle have been pushed to the feedlots, but increased herd culling is likely to maintain the negative trajectory in beef supply. Longer-term, this will likely pressure the operating margins of companies with exposure to beef costs.

Select Company Guidance

WEN:

- Total commodity basket +4-5% in 2013, beef a “big part” of that increase

- Mgmt’s conversations with experts takeaway: long-term supply-demand imbalance

- Beef is 20% of WEN spend

BLMN:

- Basket expected to gain 3-4% for FY12, including 10% gain in beef prices

- Beef prices expected to gain 10% in FY13 again

- Beef is 30% of BLMN spend

- Company believes it has room to take more price at Outback, currently at 1-2% range

JACK:

- Beef costs expected to be sequentially higher from where they were most recently (+5% yy)

- Lapping elevated beef costs in 1QFY13 (Dec) and 2QFY13

- Beef is 20% of JACK spend

Macro Callout

As we did last week, we are calling out gasoline prices again as the year-over-year increase seems likely to grow at least over the near-term. For Cracker Barrel and, to a lesser extent, other casual dining chains, this is a very important driver (or destroyer) of demand among consumers, on a year-over-year basis.

Correlation

Charts

<chart12>

<chart15>

Howard Penney

Managing Director

Rory Green

Analyst