This note was originally published at 8am on August 23, 2012 for Hedgeye subscribers.

“In the end, you are exactly—what you are. Put on wig with a million curls,

Out the highest heeled boots on your feet, Yet in the end you remain just what you are.”

-Mephistopheles

Today is August 23rd. To many of you stock market operators, it is just another day of finding compelling investments and tweaking those market exposures. But for those of you who didn’t know, it is also National Compliance Officer Day. So take a few minutes and go see that guy or gal who runs your compliance department, who you typically like to avoid, and give them a big thank you.

One of the first hires at Hedgeye was our compliance officer, Rabbi Moshe Silver. Not only would I put his knowledge of the compliance up against anyone’s, but he is also kind of funny. By kind of I mean he tells jokes, even if they aren’t all funny. In all seriousness, Moshe, on behalf of all of us, thank you for your fine work as our compliance officer and teammate.

Now that I officially have my compliance officer off my back for a few months, let’s get back to the global macro grind. A topic I want to start with today is China. Maybe you’ve heard of it? It’s the country that has taken a massive amount of economic market share over the last two decades. I just wanted to flag a few interesting nuggets from China over the last couple of days. They are as follows:

- Chinese iron ore prices are at their lowest levels since 2009 and mills are beginning to default on supply contracts;

- Zhang Honxia, chairman of China’s largest cotton-textile maker, said: “The Chinese economy is only at the beginning of a harsh winter. We are in worse shape now then compared with 2008-2009.”;

- Iron ore output in China is down 8.1% in July;

- The Shanghai Composite hit a three-year low yesterday;

- Japanese exports to China in July were -11% year-over-year; and

- The IMF has estimated that China’s capacity utilization has fallen to just 60% versus 80% in the pre-crisis era.

To be clear, I didn’t hand pick those data points to paint some bearish mosaic. They are actually just what I wrote down in my notebook and, candidly, they are a little depressing as it relates to Chinese growth.

Last night’s PMI readings were of similar nature, if not worse, for China. In aggregate, the PMI for August fell to 43.0 from 45.1 in July. The specifics were even more dreary, new orders fell to 46.6 from 48.7, new export orders slumped to 44.7 (the lowest reading since the financial crisis), and inventories rose to 53.6. Inventory up and orders down are a toxic mix for any company, let alone the world’s second largest economy.

Despite this plethora of negative data points, the equity markets keeps grinding higher. Perversely, bad news is good news because bad news means more central bank easing. The only term I can really think of for this type of investing (and no offense to those of you that are profiting from it) is Faustian Investing.

As many of you know, Faust is a protagonist in a classic German legend. He is a very successful scholar, but like many successful people, he wants more. As a result, Faust makes a deal with the devil and exchanges his soul for unlimited knowledge and worldly pleasures. To me, buying equities at a VIX of 15.1 on hopes of further easing from central bankers feels like a deal with the devil. Incidentally, there is a gentleman named Jon W. Faust who is a special advisor to the FOMC Board of Governors. And I couldn’t make that up even if I wanted to …

Speaking of easing, many have asked our view of whether some incremental news on the monetary policy front could come out of Jackson Hole next week. I will touch on that in a second, but let me just start with this, it is likely priced in. The SP500 is up 11% in almost a straight line from the lows of the summer into Jackson Hole. And from interacting with our many subscribers and even more followers on social media, this is the “catalyst” people are talking about.

Now, as to whether the Fed will actually do anything next week is a different question. The key economic takeaway yesterday from the release of the FOMC’s minutes was that, “economic activity increased at a slower pace in the second quarter than earlier in the year and that labor market conditions had improved little in recent months.” So as a result:

“Many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery.”

There you have it: the Fed is poised to ease! I’m just not sure it will be at Jackson Hole next week. The last time Bernanke announced action at Jackson Hole was QE2 in 2010. At that point, equity markets had undergone a serious two month sell off, the government had just lowered its reading Q2 2010 GDP growth to 1.6%, and broad economic indicators were more anemic than they are now (we will have a detailed post on this later today).

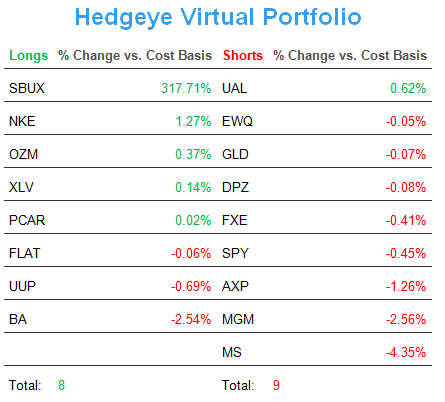

So in summary, we think any potential action at Jackson Hole is both unlikely and also priced into equities. To express this from a non-Faustian investing perspective, yesterday in the virtual portfolio we bought the U.S. dollar and shorted gold.

The greater question, though, is whether incremental easing will have any impact on economic activity. In the Chart of the Day below, we show both major recent Fed policy announcements in Q3 2007 and Q3 2010 and subsequent global economic activity. In both instances, growth slowed and inflation accelerated. Be careful what you wish for from those devilish central bankers.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500 are 1621-1679, 113.71-116.12, 81.41-82.11, 1.23-1.25 (TREND resistance = 1.26), 1.66-1.75% and 1410-1419, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research