TODAY’S S&P 500 SET-UP – August 29, 2012

As we look at today’s set up for the S&P 500, the range is 17 points or -0.52% downside to 1402 and 0.69% upside to 1419.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/28 NYSE 386

- Increase versus the prior day’s trading of -149

- VOLUME: on 08/28 NYSE 516.47

- Increase versus prior day’s trading of 2.41%

- VIX: as of 08/28 was at 16.49

- Increase versus most recent day’s trading of 0.86%

- Year-to-date decrease of -29.53%

- SPX PUT/CALL RATIO: as of 08/28 closed at 1.49

- Down from the day prior at 1.80

CREDIT/ECONOMIC MARKET LOOK:

BONDS – hoowah! what a move in the US Treasury market – the 10yr yield looks like the Chinese synchro diving team here, dropping straight back down to 1.62%, snapping TRADE support of 1.65% like a knife through water – today’s US GDP report will remind the March 2012 “growth is back” bulls that stocks may have rallied for 6wks, but not for the growth reasons they called for back then.

- TED SPREAD: as of this morning 32.65

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.64%

- Increase from prior day’s trading of 1.63%

- YIELD CURVE: as of this morning 1.37

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates)

- 7am: MBA Mortgage Applications, Aug. 24 (prior -7.4%)

- 8:30am: GDP Q/q (Annualized), 2Q, est. 1.7% (prior 1.5%)

- 8:30am: Personal Consumption, 2Q, est. 1.5% (prior 1.5%)

- 8:30am: GDP Price Index, 2Q, est. 1.6% (prior 1.60%)

- 8:30am: Core PCE Q/q, 2Q, est. 1.8% (prior 1.8%)

- 10am: Pending Home Sales M/m, July, est. 1% (prior -1.4%)

- 10:30am: DoE Inventories

- 11am: Fed to purchase $4.25b-$5b notes 8/31/2018-8/15/2020

- 1pm: U.S. to sell $35b 5-yr notes

- 2pm: Fed’s Beige Book

GOVERNMENT:

- Republican National Convention, Day 3: Speakers include Paul Ryan; John McCain; Mitch McConnell; Jeb Bush; Tim Pawlenty; Condoleezza Rice

- House, Senate not in session

- SEC meets to consider eliminating prohibition against general solicitation, advertising in securities offerings, 10am

- CMS holds semi-annual meeting of advisory panel on outpatient payments for hospitals, 9am

- International Society of Air Safety Investigators holds annual seminar, with NTSB Vice Chairman Christopher Hart, 8am

WHAT TO WATCH:

- Daikin buys Goodman Global for $3.7b to expand in Nth. America

- Hurricane Isaac beginning to move into Louisiana, NHC says

- G-7 countries call for increased oil output to meet demand

- KKR said to be in talks to buy Renesas for $1.2b: Nikkei

- Italy borrowing costs fall at 6m bill auction

- Republican convention continues in Tampa; Paul Ryan speaks

- Morgan Stanley, Citigroup delay valuation of brokerage JV

- Wellpoint searches for new CEO as Angela Braly resigns

- Apple’s request for Samsung ban to be heard Dec. 6

- Swedish FSA says banks can lend more amid tougher rules

EARNINGS:

- Joy Global (JOY) 6am, $1.89 - Preview

- Fresh Market (TFM) 6am, $0.27

- Jos A Bank (JOSB) 6am, $0.73

- HJ Heinz (HNZ) 7am, $0.81

- JA Solar (JASO) 7am, ($0.96)

- Zale (ZLC) 7:30am, ($0.83)

- Genesco (GCO) 7:31am, $0.26

- Brown-Forman (BF/B) 8am, $0.63

- Tivo (TIVO) 4pm, ($0.24)

- Oxford Industries (OXM) 4pm, $0.63

- Pandora Media (P) 4:02pm, ($0.03)

- Vera Bradley (VRA) 4:02pm, $0.35

- Greif (GEF) 4:07pm, $0.71

- Canadian Western Bank (CWB CN) 6:48pm, $C$0.57

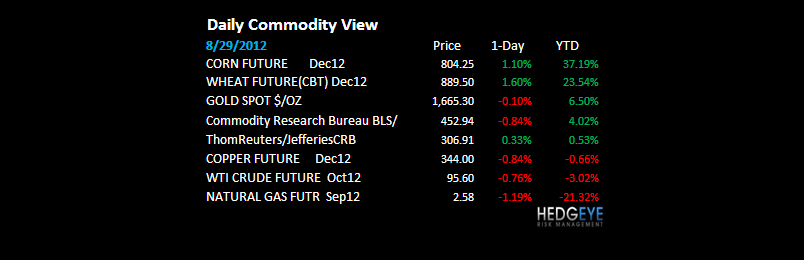

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- No Return to Dirty ’30s as Farmer Sees Drought Relieved by U.S.

- Oil Falls From One-Week High on Isaac, G-7 as Gasoline Declines

- Timah Restarts Tin Spot Sales After Advances, Sukrisno Says

- Big Coal Faces Steel Slowdown Amid Shale-Gas Pain: Commodities

- Southeast Asian Buyers Seek Cheaper Soybean Meal, Corn Supplies

- Soybeans Rise for Second Day on Signs of Increasing World Demand

- Monsoon Revival Brightens Prospects for India Rice, Cane Crops

- Gold Seen Falling in London Before Bernanke Speech This Week

- Aluminum Premiums in Japan Set for Record High as Supply Limited

- Cocoa Rises as West Africa May Have Little to Sell; Sugar Gains

- Gold ETP Assets Jump to Record to Overtake Italy’s Reserves

- Lingerie Delayed as $517 Billion India Jam Idles Trucks: Freight

- Platinum ‘Correction’ a Buying Opportunity: Technical Analysis

- Gold Calls at 2008 High on Jackson Hole Bet

- Tin Declines as Restart of Producer Sales Eases Supply Concern

- Palm Oil Drops on Speculation Stockpiles to Increase in Malaysia

- Gold Calls at 2008 High on Easing Bets for Jackson Hole: Options

CURRENCIES

EUROPEAN MARKETS

EUROPE – lower-highs on lower volumes across the board in all of the major Eurocrat markets; finally, the apex of the short squeeze looks to be over as my most immediate-term TRADE lines of price momentum are all snapping (for the IBEX that line = 7416).

ASIAN MARKETS

CHINA – it’s not just U.S. consumers who couldn’t care less about 6 wk U.S. stock market rallies to lower highs; Chinese and Indian consumers do not like food/energy prices up here and neither do their stock markets; Shanghai Comp -1%, back to YTD lows.

MIDDLE EAST

The Hedgeye Macro Team