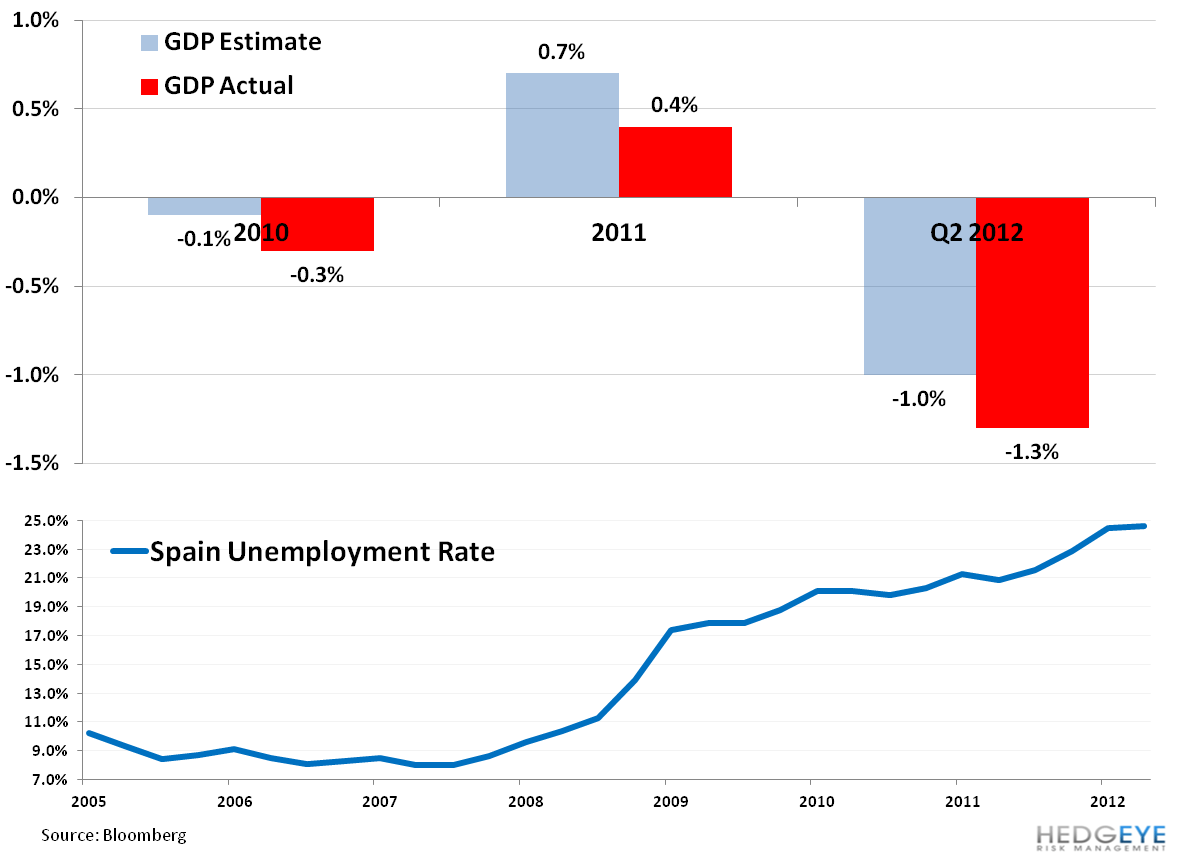

Spain is quickly becoming the new “China” in terms of the economic data its been putting out. China loves revising GDP and employment numbers all the time and now Spain is joining in on the fun. It revised its GDP numbers on Monday, indicating it had increased 0.4% in 2011 instead of 0.7%. It also noted that its economy shrank by 0.3% in 2010 instead of 0.1%. Whoops!

Spain’s unemployment rate has continued to climb since 2008 and picked up swiftly in 2011, in line with the revised GDP numbers. Nearly one-in-four people are unemployed in the country as the unemployment rate hovers around 22%. If this is a sign of the kind of games Eurozone members are going to play in order to save face, the outlook for the rest of 2012 is quite grim.

Hedgeye Senior Analyst Matthew Hedrick lists several reasons why Spain’s situation will continue to worsen:

• As many peripheral European counties continue austerity programs, growth will slow.

• This will show up in missed deficit targets, often because they’re unrealistic targets (Portugal and Spain in particular).

• And in missed growth targets, as austerity has a greater drag on growth and confidence than previously assessed.

• Spain is one example of a country trying to dig itself out of a huge hole, struggling with huge unemployment rate figures (over 50% for youths), further downside in the property market, and major bank recapitalization needs (current pending funds from the EFSF)

• We expect confidence and growth to be muted by the developments outlined above, and therefore growth targets to under deliver. This could be a theme throughout not just the periphery but much of Europe over the next quarters as the region’s sovereign debt and banking “crisis” has a nasty tail.