TODAY’S S&P 500 SET-UP – August 28, 2012

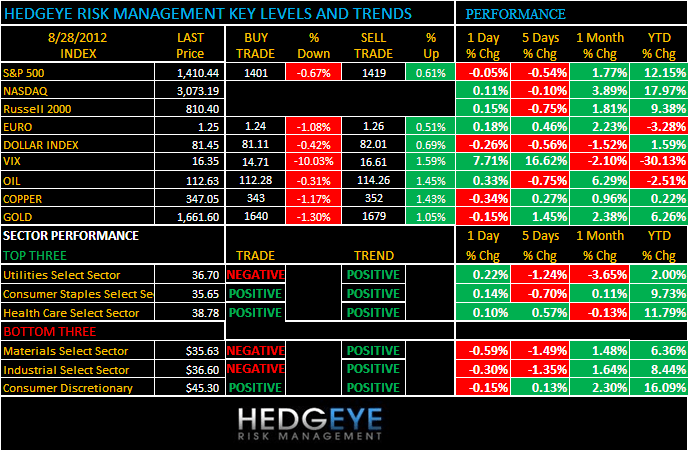

As we look at today’s set up for the S&P 500, the range is 18 points or -0.67% downside to 1401 and 0.61% upside to 1419.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/27 NYSE -149

- Decrease versus the prior day’s trading of 855

- VOLUME: on 08/27 NYSE 504.30

- Decrease versus prior day’s trading of -2.13%

- VIX: as of 08/27 was at 16.35

- Increase versus most recent day’s trading of 7.71%

- Year-to-date decrease of -30.13%

- SPX PUT/CALL RATIO: as of 08/27 closed at 1.80

- Down from the day prior at 2.23

CREDIT/ECONOMIC MARKET LOOK:

BONDS – sell stocks and buy bonds? at 1.89% in the 10yr, we did – now we’re staring down the pipe of a 1.64% 10yr yield this morning and a Yield Spread that’s pancaked in the last week back down to 137bps wide. Commodity inflation is not growth. It slows real growth.

- TED SPREAD: as of this morning 33.35

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.64%

- Decrease from prior day’s trading of 1.65%

- YIELD CURVE: as of this morning 1.37

- Down from prior day’s trading 1.39

MACRO DATA POINTS (Bloomberg Estimates)

- 7:30am/8:45am: ICSC/Redbook weekly sales

- 9am: S&P/CS 20 City Home Price Index M/m, June, est. 0.4% (prior 0.91%)

- 9am: S&P/CS U.S. Home Price Index Y/y, 2Q (prior -1.92%)

- 9am: S&P/CS Home Price Index, June (prior 138.96)

- 10am: Conference Board Consumer Confidence, Aug., est. 66.0 (prior 65.9)

- 10am: Richmond Fed Manuf. Index, Aug., est. -10 (prior -17)

- 11am: Fed to purchase $4.5b-$5.5b notes 11/15/2020-8/15/2022

- 11:30am: U.S. to sell $40b 4-wk. bills

- 1pm: U.S. to sell $35b 2-yr. notes

- 4:30pm: API inventories

GOVERNMENT:

- Republican National Convention in Tampa, Day 2: Prime-time speakers include Ann Romney; Rick Santorum; Va. Gov. Bob McDonnell; N.J. Gov. Chris Christie

- House, Senate not in session

- Arizona primaries: Rep. Ron Barber vs State Rep. Matt Heinz in Democratic primary; in Senate race, Rep. Jeff Flake vs Wil Cardon in Republican primary, polls close 9pm

- Biotechnology Industry Organization hosts conference call on “Renewable Fuel Standard and the Drought,” focusing on governors of several states petitioning EPA to waive requirements of federal renewable fuel standard, 2pm

- Acting FDIC Chairman Martin Gruenberg discusses Quarterly Banking Profile, 10am

- Center for Strategic and International Studies holds logistics conference on “Creating a 21st Century Supply Chain,” with HPQ’s Tony Prophet, World Bank’s Bernard Hoekman, 2pm

WHAT TO WATCH:

- Tropical storm Isaac on verge of becoming hurricane today

- Isaac seen making U.S. release from SPR more likely

- GM said to plan halt of Chevrolet Volt production for 4 wks

- Apple seeks ban on sales of 8 Samsung phones in U.S.

- Forest Laboratories adopts shareholder-rights plan

- U.S. farm income seen up as drought prices overtake lower yields

- ECB to urge weaker Basel liquidity rule on crisis concern

- Spain sells $4.5b of bills exceeding target

- Standard Chartered faces U.S. fine over Iran: N.Y. Post

- Japan cuts economic assessment as BNP says contraction looms

- Canada’s Bank of Montreal, Bank of Novia Scotia report earns

- Toyota offers $2b to buy 70% of CFAO to expand in Africa

- Knight Capital to name 3 new directors today: WSJ

EARNINGS:

- Sanderson Farms (SAFM) 6:30am, $1.07

- Brown Shoe (BWS) 7am, $0.03

- Cyberonics (CYBX) 7am, $0.36

- Bank of Montreal (BMO CN) 7:26am, C$1.34

- Bank of Nova Scotia (BNS CN) 7:30am, C$1.19

- Movado (MOV) 7:30am, $0.26

- Ship Finance (SFL) Pre-mkt, $0.42

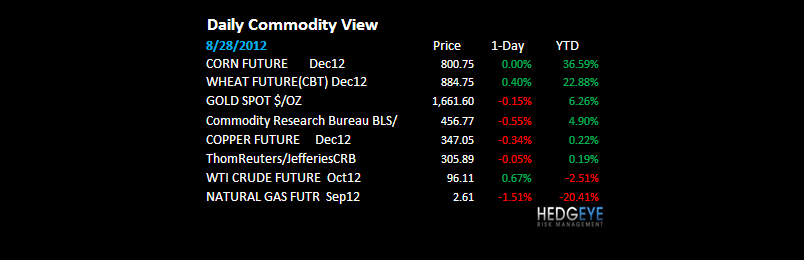

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – bailout bulls did not like the headline this morning that Draghi isn’t going to Jackson Hole. The Dallas Fed (Fisher) put the heat on Bernanke yesterday again too (don’t underestimate the GOP convention launching w/ a ticking debt clock in the background today either); Romney picking up some momentum this week could be Dollar bullish; gold bearish, on the margin, from lower-highs.

- Robusta Coffee Beats Arabica as Folgers Cut Prices: Commodities

- Barclays Gutted in Energy Trade as Bonus Limits Spark Exodus

- Isaac Seen Making U.S. Release From Oil Stockpiles More Likely

- China May Sell Cotton From Stockpile, Release Import Quota

- Oil Advances on U.S. Supply Forecast, Venezuela Refinery Blaze

- Corn Declines as Rains May Ease Dry Conditions in Southern U.S.

- Copper Nears One-Week Low on Signs of Slowing Asian Economies

- Gold Set to Gain in London on Demand for Protection of Wealth

- ICCO Reduces Global Cocoa Shortage Forecast by 56% This Year

- Iron Ore Poised to Drop as Slowing Growth in China Cuts Demand

- Louisiana Preps for Oil Dredged From the Gulf by Isaac’s Power

- Tanker Trackers Turn Bearish as IEA Trims Oil Forecast: Freight

- Olam Fourth-Quarter Profit Falls 14% on Industrial Raw Materials

- Crude Supplies Fall to Five-Month Low in Survey: Energy Markets

- Storm Isaac May Reach Hurricane Strength

- Sugar Nears Two Year-Low as Brazil Crop Speeds Up; Coffee Rises

- U.S. Farm Income Seen Up as Drought’s Prices Trump Lower Yields

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

JAPAN – could Japanese GDP growth go negative sequentially? They do have to adjust real growth for imported energy inflation (unless they make up the number like Spain does); and the Nikkei continues to make lower-highs (down -12% from its March top)

MIDDLE EAST

The Hedgeye Macro Team