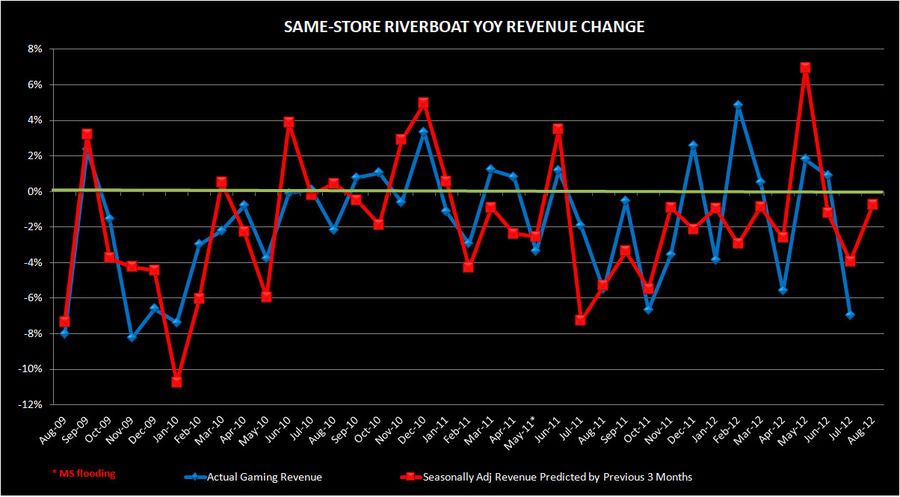

- Riverboat same-store revenues fell 7% YoY in July, the worst SSS performance since January 2010

- The seasonally adjusted trend was predicting -4%, and already accounted for the unfavorable calendar (one fewer Friday and Saturday relative to July 2011)

- Louisiana led the decline, tumbling 12% YoY—the worst monthly drop since January 2010