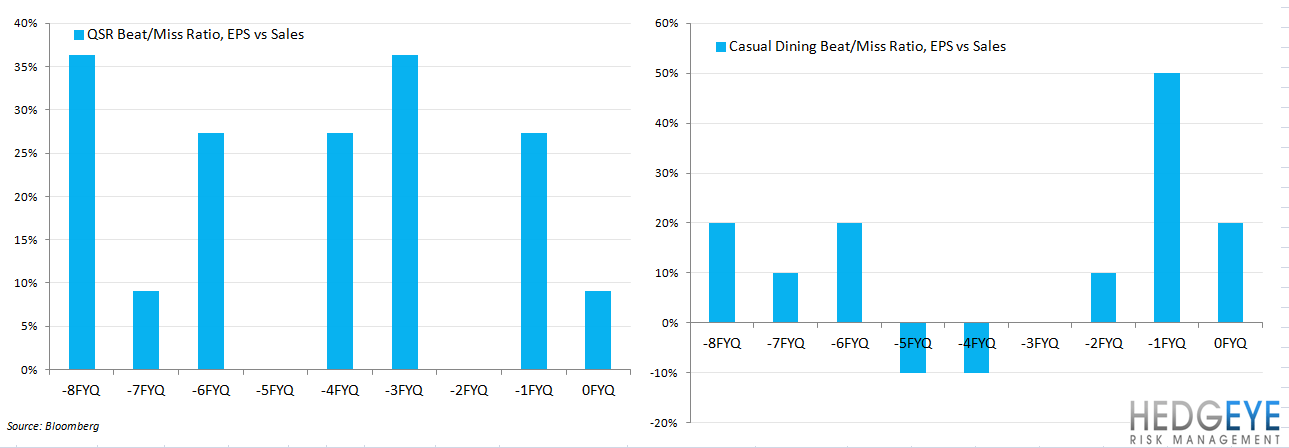

Now that earnings season is over, we decided to examine the trend in top- and bottom-line results versus expectations over the last couple of years. Conclusive takeaways are difficult to make in this case, but it certainly seems that restaurant companies have succeeded in managing EPS results over the the majority of the past eight quarters of reported earnings.

The restaurant stocks we have included in this note have produced earnings results that have, in general, exceeded consensus EPS expectations by a greater margin than sales expectations over the last eight quarters. From a price reaction perspective, it seems that sales beats/misses have possibly been more important to investors. We would add that we are not comfortable making that assertion definitively given the arbitrary duration – three days - of the price reactions we have aggregated and the broader market and industry moves that can obscure investors’ reaction to earnings results. That aside, we do think that the charts below make for interesting viewing.

The stocks included are as follows:

Casual Dining: RUTH, TXRH, DRI, BJRI, CAKE, DIN, BWLD, RT, EAT, CBRL

Quick Service: MCD, SBUX, WEN, GMCR, CMG, SONC, PEET, DPZ, PZZA, YUM, PNRA

EPS Surprises Far-Outstripping Sales Surprises in Recent Quarters

Companies within the restaurant industry seem to have succeeded in managing the bottom line over the last eight quarters. As the charts below illustrate, casual dining, in particular, has been able to pull levers either within operating costs or other expenses, in order to exceed EPS expectations more consistently than top-line expectations.

QSR Earnings Callouts

CMG: Chipotle Mexican Grill reported 2Q earnings that were in line from a sales perspective and 13% above EPS expectations. Nevertheless, due to comparable sales growth in 2Q lagging expectations, the stock traded off -21.5% over the three days following the announcement.

GMCR: Green Mountain Coffee Roasters reported EPS of $0.52 versus $0.49 consensus for 3QFY12 but missed the top-line number and struck a cautious tone on future sales trends. The stock sold off on the news but recovered and traded sharply higher, we believe on short covering, based on comments from management on a new demand forecasting model. We still believe that the bull case for Green Mountain’s stock is fanciful at best and will be publishing detailed work on the difficult pricing environment the company could face as its patents expire and competition intensifies in the single-serve category.

Casual Dining Earnings Callouts

BWLD: Buffalo Wild Wings missed the Street’s 2Q top- and bottom-line expectations and traded off almost 6% over the following three days. The bottom line miss was more meaningful, in terms of magnitude, than the top line as commodity costs continued (and continue) to pressure the P&L.

TXRH: Texas Roadhouse reported a strong EPS beat of 18% ($0.28 versus $0.24) but top-line results were only in line and beef inflation commentary also likely weighed on investor sentiment. We believe that this stock is one to stay away from on the long side given the commodity outlook and slowing industry sales. Additionally, the company’s Return on Incremental Invested Capital is decelerating.

QSR Beat/Miss Trends

Casual Dining Beat/Miss Trends

<chart6>

Howard Penney

Managing Director

Rory Green

Analyst