“The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.”

-Ernest Hemmingway

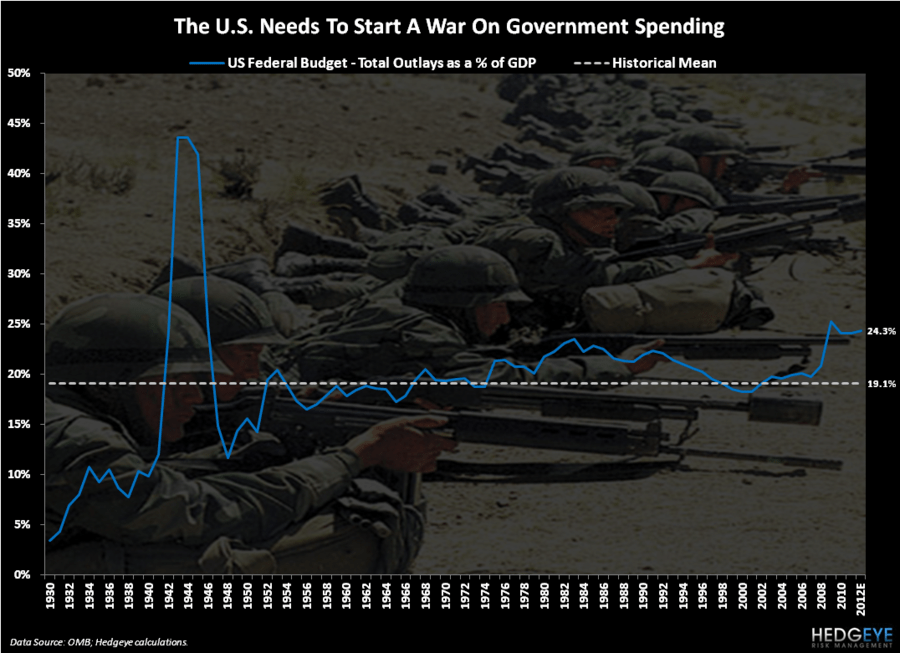

Anyone who has analyzed the United States federal budget understands that this fine country spends a lot on its military. In fact, based on estimates from the nonpartisan Congressional Budget Office defense spending, that is considered discretionary, will total $635 billion in fiscal 2013. This is more than 52% of the total discretionary budget of the U.S. government and just under 20% of total federal government spending.

In terms of all global defense spending, the U.S. is dominant. According to the Stockholm International Peace Research Institute’s (SIPRI) 2012 Yearbook, the U.S. spends more than 40% of the combined global military spending pie. The next four countries on the list are as follows: China at 8.2%, Russia at 4.1%, the UK at 3.6%, and France at 3.6%.

Since the U.S. spends the most on defense on a gross dollar basis and as a percentage of GDP at 4.7%, it is obvious that the U.S. has solidified its so-called “hyper power” status as the world’s primary military power. As a Canadian, I can assure you that I appreciate the powerful U.S. military and the people that currently serve and have served in the military. But as a global macro analyst, it is difficult not to question whether the U.S. is overspending, if not at least spending inefficiently.

The most recent military spending controversy occurred last month when a well-connected supplier received a contract to produce oil pans for $17,000 a pop. (If I could get a deal like that, I might even consider getting out of the research business!) Yesterday, in fact, the ever-controversial Grover Norquist made the following statement regarding wasteful defense spending:

“Conservatives need to remember that, just as spending money on something called education doesn't mean people are educated and spending money on welfare doesn't mean it adds to the general welfare calling something national defense doesn't mean it is. It may not be. It may undermine national defense if it's a waste of resources, if it's a misallocation of resources.”

Later today the CBO will release its updated budget and economic outlook, we will analyze this update in a note, but we certainly do not expect positive news from the CBO. It’s important because the direction of the U.S. budget is a key factor that will drive the value of the U.S. dollar over time.

The obvious conclusions from the CBO’s reports will likely be that the U.S. needs to drastically cut spending and that an effective growth policy needs to be implemented to juice revenue. On the military spending front, an improved spending outlook will come from more efficient spending and also more unique ways of waging war.

To the last point, next Wednesday at 11am we will be hosting a conference call with Jim Rickards, the author of Currency Wars: The Making of the Next Global Crisis. A key catalyst for writing this book was that Rickards has been a long time consultant to the Department of Defense and has participated in large-scale economic war games.

Rickards’ view is that the U.S. is already facing national security threats via economic warfare including: clandestine gold purchases from the Chinese, to hidden agendas of sovereign wealth funds, to explicit threats from the Russians about diversifying away from the dollar. In an even more controversial stance Rickards believes that the biggest economic threat we currently face may well be from an overly exuberant Federal Reserve Chairman in Ben Bernanke. While it sounds like Rickards is carrying Hedgeye water so to speak, we actually disagree on a number of key points and will be pushing him on some of his more extreme views.

On the call with Rickards we will also provide you with our updated investment views on the major currency pairs. Our institutional subscribers will automatically get access to the call, if you are not a current institutional subscriber but would like to participate, please email .

Now as for the war that is currently going on in your portfolio, I have a couple of points to highlight this morning. Near the close yesterday, we released a note that emphasized the quantitative set up, which is what we call an “outside day”. This occurs when the SP500 trades higher than the previous close intraday but then closes below it. From a fundamental perspective, this suggests that there is likely a good overhead supply of stock for sale at that level.

The inability of the SP500 to break through that key level is even more negative when combined with where we see investor sentiment, which is in a word: complacent. For starters, as we’ve stated repeatedly, the VIX at/or near the 15.0 level has consistently signaled a time to sell equities over the past three years. After yesterday’s action, the VIX also became bullish from a TRADE duration in our models. This implies the VIX has even more upside in the short term. Further, the bull/bear spread from the U.S. Investors Intelligence Poll is now 2,260 basis points wide to the bull side. So, yes investors are leaning long.

And on the old global growth watch, Japan posted a -8.1% decline in exports on a year-over-year basis. Not surprisingly, exports to the European Union were down -25% and to China were down -11.9%. But don’t worry, Japan is only the fourth largest economy in the world . . .

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500 are now $1, $113.52-115.18, $81.91-82.46, $1.22-1.24, 1.75-1.82%, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research