TODAY’S S&P 500 SET-UP – August 21, 2012

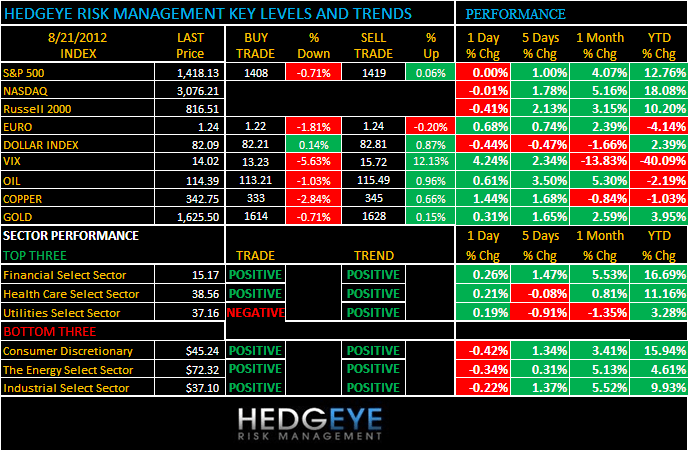

As we look at today’s set up for the S&P 500, the range is 11 points or -0.71% downside to 1408 and 0.06% upside to 1419.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/20 NYSE -343

- Decrease versus the prior day’s trading of 706

- VOLUME: on 08/20 NYSE 550.72

- Decrease versus prior day’s trading of -18.49%

- VIX: as of 08/20 was at 14.02

- Increase versus most recent day’s trading of 4.24%

- Year-to-date decrease of -40.09%

- SPX PUT/CALL RATIO: as of 08/20 closed at 2.44

- Up from the day prior at 1.77

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 34

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.82%

- Increase from prior day’s trading of 1.81%

- YIELD CURVE: as of this morning 1.54

- Up from prior day’s trading of 1.52

MACRO DATA POINTS (Bloomberg Estimates)

- 6am: EFSF to sell up to EU1.5b 182-day bills

- 7:55am/8:45am: ICSC/Redbook retail sales

- 8:45am: Fed’s Lockhart speaks in Atlanta

- 11am: Fed to sell $7b-8b notes 9/15/2014-4/30/2015

- 11:30am: U.S. Treasury to sell $40b 4-wk., $25b 52-wk. bills

GOVERNMENT

- House, Senate not in session

- Manufacturers Alliance for Productivity and Innovation hosts discussion on NERA report on impact of regulations on U.S. manufacturers, 10am

- API holds conference call briefing to discuss SEC regulations on companies that make payments to foreign governments under Section 1504 of Dodd-Frank financial regulations bill, 10:30am

- Acting Commerce Secretary Rebecca Blank meets local business leaders in Philadelphia, Allentown Pa. on job creation

- NRC holds conference call to discuss apparent violations of regulations regarding radiation safety, security of portable nuclear gauges at facility in Juneau, Alaska, 3pm

- AICPA 2012 National Governmental Accounting & Auditing Update Conference

- ITC meets on seamless carbon, alloy steel standard, line and pressure pipe imports from Germany, 9:30am

- ITC hears patent-infringement case X2Y Attenuators filed against Intel over processor chips in Apple, HP computers, 9am

WHAT TO WATCH:

- Citigroup became first Western bank to issue credit cards in China without co-branding from local financial institution

- Lawyers for Apple, Samsung to make final arguments to jury today following three-week trial over patents

- Spanish borrowing costs fall at 12-month bill auction

- Conoco, Origin Energy said to be working with JPMorgan to help sell stake in their $20b natgas project in Australia

- J&J said to agree to pay ~$600k to resolve 3 cases in first settlements of litigation over hip implants

- Apple set U.S. record for mkt value yesterday

- Facebook director Peter Thiel sold most of his stake yday

- Edison to cut staff at shuttered San Onofre nuclear plant

- Samsung to invest ~$4b in Texas factory to boost output of processors used in smartphones, tablet computers

- President Obama raised almost $9m more in July than Mitt Romney; combined balances as of July 31 for Republican election bid $169m vs $107m for Democrats

- Elpida Memory to get $3.5b in support from Micron

- Consolidated Media Holdings expects to receive details from News Corp. on its takeover proposal within six weeks

- Samick studying possible tender offer for Steinway

- U.S. Trustee overseeing Kodak’s bankruptcy asked to probe patent auction by New York hedge fund

- Apple sued by ex-worker who says Steve Jobs guaranteed his job

- Wall Street struggling to find champion to replace Dimon

- U.S. consumers rated automakers this year at same level as record-high satisfaction score in 2009: American Customer Satisfaction Index

EARNINGS:

- Tech Data (TECD) 6am, $1.19

- Williams-Sonoma (WSM) 6am, $0.41

- DSW (DSW) 7am, $0.62

- Globe Specialty Metals (GSM) 7am, $0.15

- Medtronic (MDT) 7:15am, $0.85; Preview

- Best Buy (BBY) 8am, $0.31; Preview

- Barnes & Noble (BKS) 8:30am

- Raven Industries (RAVN) 9:10am, $0.38

- Intuit (INTU) 4pm, $0.06

- Analog Devices (ADI) 4:01pm, $0.56

- Aspen Technology (AZPN) 4:01pm, $(0.04)

- Dell (DELL) 4:01pm, $0.45

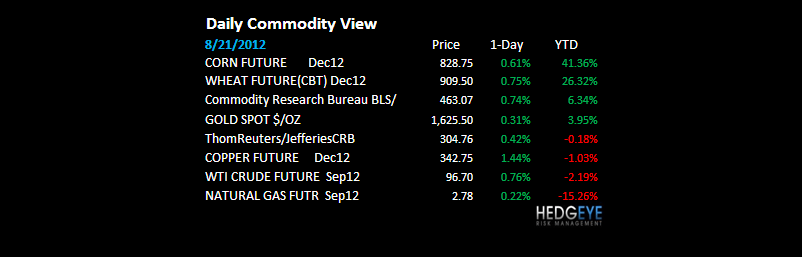

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Bear Market in Tin Shuts 70% of Indonesian Capacity: Commodities

- Oil Supply Rises First Time in Month in Survey: Energy Markets

- Soybeans Top $17 for First Time as Demand Jumps for U.S. Exports

- Commodities Headed for Bull Market as U.S. Drought Withers Crops

- Oil Advances to Three-Month High Before European Debt Meetings

- Copper Gains as European Meetings May Aid Debt-Crisis Progress

- Gold Advances to Three-Week High as Weaker Dollar Spurs Demand

- Glencore CEO to Abandon Xstrata Bid Should Qatar Stymie Deal

- China Buys Most Corn in Six Months as Imports Set for Record

- Cocoa Seen Gaining as Dry Weather Curbs Output; Sugar Declines

- Asia-Pacific Oil Drillers in U.S. Gulf Seen With BP Sale: Energy

- Natural Gas Advances in New York as Tropical Storm May Develop

- South Dakota Corn, Soybean Yields 47 Percent Lower Than 2011

- Copper May Extend Decline While Below $7,622: Technical Analysis

- Soybeans Advance to Record as Demand Rises

- Ohio Corn Yield Falls 29%, Soy Counts Decline, Tour Shows

- Norden Profits as Smallest Ships Beat Bigger Carriers: Freight

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team