“This is a serious problem, although it is not as dramatic as sort of an epidemic.”

-James Bond

Author Ian Fleming created James Bond, code named 007, in 1953 and subsequently featured him in twelve novels and two short story collections. Bond was an intelligence officer in the Secret Intelligence Service and a Royal Naval Reserve Commander. Fleming based this fictional character on many of the intelligence officers and commandos he met during World War II. Interestingly, the name James Bond came from American ornithologist James Bond, a Caribbean bird expert and author of the definitive field guide Birds of the West Indies. (Don’t worry, I haven’t read it either.)

Over the course of the Fleming’s twelve novels and the twenty-two James Bond movies (the highest grossing series ever at $4.9 billion), Bond utilizes his astute intelligence gathering capabilities, combined with various gadgets, including an exploding attaché case, to save the world from a myriad of threats. If Bond were a research analyst studying today’s markets, the U.S. bond markets may be considered an emerging epidemic in his analytical purview.

Even if not an epidemic, bond issuance levels this year have been staggering. Firstly, in the municipal bond market in the United States, as of May, issuance is up 70% compared to the same period in 2011. Secondly, in the U.S. corporate bond market issuance is up 5% year-over-year, but has seen a serious acceleration in the last few months with investment grade issuance up 54% and high yield up 30% in July 2012. Finally, according to Lipper Research, bond ETFs have seen the eighteenth consecutive month of net inflows.

So, is there is a bond epidemic / bubble? Given the stance of the global central banks to keep interest rates at artificially low levels, it is likely not an epidemic that is going to end in the short term. In fact, we are actually aggressively allocated to U.S. government bonds as we think equities are at an extreme and growth is continuing to slow. Certainly though, James Bond, the research analyst, would be gathering his intelligence and watching and waiting for an opportunity to sell the high yield bond market.

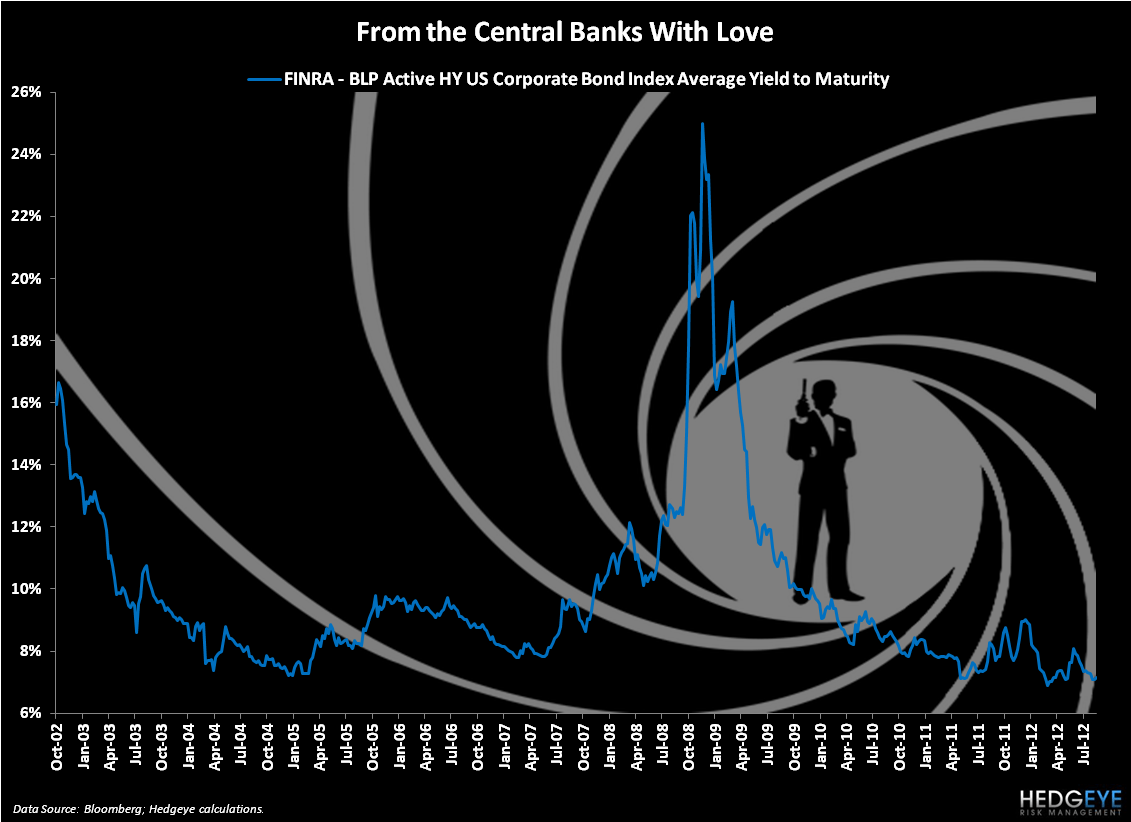

As we show in the Chart of the Day below, which we have aptly named, From the Central Banks with Love, the high yield market is at a generational low in yield. Obviously when studying a corporate bond, there are a number of factors to analyze in determining whether it is overvalued or undervalued. Certainly, the overall interest rate environment is critical, but ultimately the prospects of the company are the drivers of a junk bond’s value, especially given the bond’s inferior position in the capital structure. Therefore, given that yields in the junk bond market are literally at generational lows, it implies that default risk is also close to an all-time low. Personally, I’d need a few James Bond-esque martinis before I’d believe that last point to be an accurate assessment of default risk.

Speaking of bonds, Der Spiegel reported this weekend that the ECB may set a specific threshold to cap periphery bond yields at its meeting in September. The immediate reaction in the European sovereign debt markets is, not surprisingly, positive as credit default swaps are trading tighter across the board. As well, the Spanish 10-year is back down to 6.19%. Even if positive in the short term, broad intervention in a large market speaks to another epidemic, the epidemic of government intervention in the free markets. Random intervention by governments does not build confidence in the markets. And confidence is what is sorely missing in the European debt markets.

In the latest sign that global growth is slowing, the Shanghai Composite hit a fresh three and a half year low this morning. The Chinese equity markets may not always garner headlines in the U.S. financial media, but nonetheless China remains the engine for global growth and as China goes so goes marginal global growth. Thursday will give us some important insights on Chinese and global growth as flash PMIs are reported for China, Europe and the United States.

Keith is back in Thunder Bay this week taking some time off with his family ahead of what is going to be a busy next few months at Hedgeye, so we will be highlighting some of the key calls from our broader research team this week. This will be kicked off this morning with our Financials Sector Head Josh Steiner and our Retail Sector Brian McGough leading our morning client call at 830 a.m. Email if you like to ask them any questions, or get access to the call.

Although we are currently not short it in the Virtual Portfolio, one of McGough’s favorite short ideas has been J.C. Penney. We’ve been consistently short JCP for the past fifteen months and will likely look to re-short when we see our level. McGough had the following to say after JCP’s recent earnings announcement:

“We won't bother with the full financial review. Comps down -22%, dot.com down 33% and a ($0.67) loss pretty much sums that up.

But that's the past. We invest for the future. One thing that matters in investing for the future is believing in who is running the ship. We initially figured that Johnson's Apple halo would have lasted 18-24 months. But about 5-minutes into his commentary today, his credibility stood up, ran out the door, and got hit by a bus.

Last quarter, his level of arrogance around communicating the message was bothersome. He spoke to the Street like we were toddlers, or at least retail novices. He glossed over the bad, and played up whatever positive statistic he could find. A JV mistake for a new CEO.”

As it relates to CEO Ron Johnson at J.C. Penney, or really any CEO of a large public company, perhaps Ian Fleming said it best when he wrote:

“Once is happenstance. Twice is coincidence. Three times is enemy action.”

Indeed.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500 are now $1, $110.89-115.21, $82.20-82.89, $1.22-1.24, 1.72-1.87%, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research