This note was originally published at 8am on July 31, 2012 for Hedgeye subscribers.

“Freedom, however is not the last word. Freedom is only part of the story and half of the truth. Freedom is but the negative aspect of the whole phenomenon whose positive aspect is responsibleness. In fact, freedom is in danger of degenerating into mere arbitrariness unless it is lived in terms of responsibleness.”

-Viktor E. Frankl

“Man’s Search for Meaning” by Victor Frankl is one of my favorite books. It is the chronicle of Frankl’s experiences in Nazi Germany’s concentration camps and was written in 1946 shortly after the end of World War II. The book has sold over 10 million copies and is often noted on the lists of the most influential books in the United States.

Frankl was uniquely qualified to analyze the experiences in a concentration camp as he was a psychologist by training. Undoubtedly, his academic training allowed him to separate his actual experiences from the analytical lens under which he observed his, and other prisoners, broad experiences in the camp.

Ultimately, Frankl concluded, from analyzing the broad collection of experiences in the concentration camps of Nazi Germany (he himself lost the vast majority of his family), that life never ceases to have meaning. In fact, according to Frankl, there is meaning in every moment. Further, we all have the freedom of choice, even if our circumstances are incredibly dire. In fact, the only scenario that truly dooms a person is when they lose all hope.

Now, admittedly, this is deep stuff for a Tuesday morning. Further, it is obviously not even close to analogous to compare our lives as stock operators to Frankl’s analysis of life in a concentration camp, except for the fact that both are about a search. For Frankl, it was the search for the meaning of life. While for stock market operators, it is the search for value.

At the end of the day (to use an overused expression), investing is solely about value. For those that follow more quantitative strategies, value can simply come in the form of the price and volatility of the asset. For those steeped in more fundamental company analysis, value comes from deriving a value for company on both a standalone basis and versus comparable companies.

As many of you know, the vast majority of our firm is comprised of fundamental analysis. In fact, we currently have seven sector heads doing fundamental company and industry research. In aggregate, we cover energy, industrials, retail, gaming lodging & leisure, healthcare, financials, and restaurants & food processing. Similar to a multi-strategy fund, we also integrate both macro analysis and quantitative analysis into our research process.

In earnings season, we get bottom up data points that combine to inform our macro view. On face value, based on data from Zack’s, earnings season has been reasonably positive. In fact, as of yesterday 300 companies in the SP500 had reported earnings and aggregates earnings were up 5.5% versus the same period last year and almost 2/3rds of them beat earnings estimates by an average median surprise of 2.8%. As always though, the devil is in the details, especially in the search for value.

A key driver of this “not too bad” earnings season is the easy comparisons of the financial sector. In fact, if we back out the financial sector earnings reports, the positive 5.5% growth noted above actually becomes a year-over-year decline of -1.5%. Moreover, revenue performance has been particularly anemic with revenue coming in basically flat versus the same quarter last year (including financials) and only 1/3 of companies beating revenue expectations.

If you are a fundamental equity investor, you are likely either looking for stability of cash flow or cash flow growth to justify your valuation. Unfortunately, not many discounted cash flow models spit out compelling valuations if cash flow is declining on a year-over-year basis. Thus, from a top down perspective, the old adage that the market is cheap based on its multiple doesn’t hold much credence when earnings are declining, and not growing, versus the prior year.

Just as important as this quarter are future earnings and revenue expectations. Typically, fundamental investors focus on earnings seasons as a key catalyst to for the market to reward them for the hidden value in their investments. Currently though, future earnings growth expectations are very high with Q1 2013 consensus earnings growth at 12.9%, Q2 2013 at 13.0%, and Q3 2013 earnings growth at 16.4%. Given the GDP growth outlook, these numbers will be coming down meaningfully.

The search for global macro value will begin in earnest tonight and tomorrow. Tonight, we have Chinese Purchasing Manager’s Index at 9pm. While tomorrow we get the PMIs for both Europe and the United States. Based on the collective macro data points we’ve been analyzing, there is no reason to believe this slew of data points will do anything but reinforce our thesis that growth is slowing.

Ironically, the Chinese stock market seems to be the one market that is credibly signaling this continued slowing of global economic growth. Chinese stocks were down another -0.3% over night and are now down -14.5% since May. This despite rumors that Premier Wen will boost stimulus measures in China in the second half of 2012.

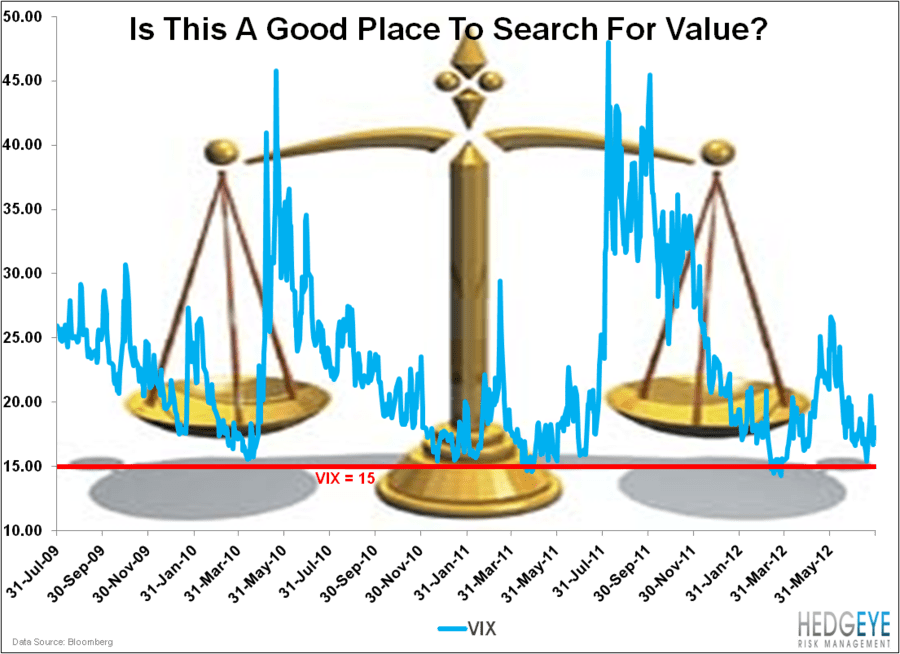

In the Chart of the Day, we once again highlight the VIX. Currently at 18, the VIX is not completely bombed out, but we would stress that it is at a level where you don’t want to begin your search for value in earnest. This is a point that has already been fundamentally validated by earnings season and will be reinforced as future earnings expectations are lowered.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Spain’s IBEX, and the SP500 are now $1606-1633, $102.52-108.36, $82.33-83.23, $1.20-1.23, 6656-6943, and 1363-1398, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research.