Conclusion: We’re keeping a TRADE a TRADE. The company is doing everything right, but it’s not immune. Earnings power is underappreciated, but we think we have time. For now it’s rangebound.

Keith covered our RL short this morning on the print. We shorted it into the print as a TRADE – simply because top line expectations were high, SG&A is headed up, they just lost their CFO, the global macro climate presented a perfect opportunity for RL to guide down, and this is a consensus long.

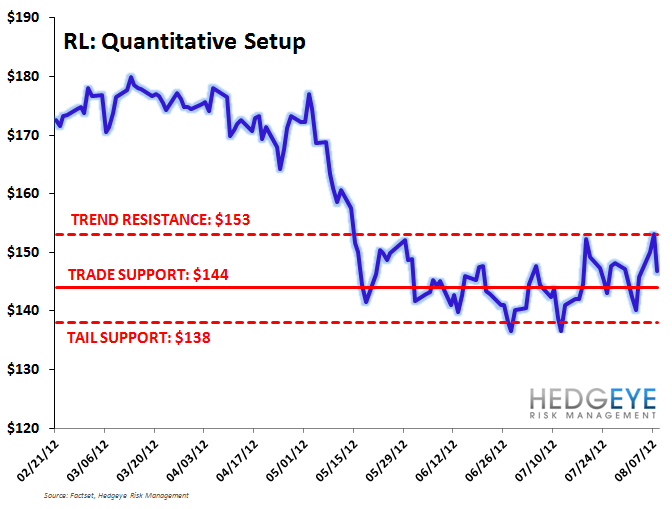

After a sharp initial sell-off, the stock is hanging in there reasonably well – most notably it is holding Keith’s $144 level. Breaking (and holding) that level would put $138 in play.

There’s not much that really changed our thought process here. We like the name more and more the further we go out in duration, and we have the earnings in our model to prove it. But the realization of $12 in EPS will not happen in a vacuum.

The reality is that this is the first time in three years that RL missed to this magnitude in its own retail stores. Comps of +1% do not exactly instill the confidence we need to bank on a 2H top line acceleration. They can make it up in the (higher margin) wholesale business, but let’s face some facts… if any power brand like RL wants to find some dollars, they turn to wholesale, not retail. Retail is the best barometer of a brand’s trajectory.

One of the positives is that they are beginning to see the benefit from input cost relief, and that should only improve from here. Unlike brands like Carter's, Hanesbrands, and Gap we think that Ralph has the brand power to keep most of the margin upside. But we’re mindful about ‘granting’ both margin upside AND top line acceleration starting 90 days out. That’s a long time to wait with a lot of unknowns.

Ultimately, where the Street shakes out over the next day or two with earnings estimates will be critical.

In the interim, Keith will do what he does…manage risk around a high conviction longer-term research call by trading a range which today stands at $144-$153.

Based on the research we have in front of us today, we’d need to see that $138 to step up and buy right now.

There are two things that could change that:

1) Time. We think that as each day draws closer to getting past 2Q, the stock has a better shot of working as margin pressure eases relative to last year's compares.

2) The Research. The reality is that the volatility in the business environment has never been greater than it is today. If there’s anyone who will be left standing, it will be RL. But there’s simply limited visibility past the upcoming quarter (where RL likely sandbagged). Could comps at retail be up 10%? Yes. Down 10%? Yes. We’ve got low single digit comps in our model for the remainder of the year. If we gain confidence in them later in the quarter, then all else equal, the stock might make sense here for the intermediate-term. But we don’t see the need to rush.

We have included below our RL Idea Alert from Monday, August 6

We shorted RL into the print for a TRADE. To be clear on this one, there’s a sharp delineation between where we like RL over each duration. In the event of a sell-off, we'd be looking for a point of entry once the dust settles to get involved with what could be $12 in earnings power.

TAIL (3-Years or Less): This is one of our favorite TAIL ideas, as we think that the consensus is underestimating RL’s 3-year earnings power by nearly a dollar. When we add up the opportunities by country, product category, and most notably – by channel (ie dot.com), we think that people are underestimating the leverage inherent to this model. Specifically, we’re looking at nearly $10 in EPS next year, and over $11.50 the year after. A 10% premium to the market suggests a stock near $175. A 1x PEG is $200+ over 2 years.

TREND (3-Months or More): RL still has a full 75% of its (March) FY left to go, so the company will be guarded into the print. RL laps European category expansion (intro of Polo FW), Denim & Supply, FX, and double digit retail comps – which are tougher to bank on this year.

TRADE (3-Weeks or Less): The company has every reason in the world to offer up a cautious outlook – given all that’s going on in the world – especially Western Europe (it has minimal exposure to China) and the clear trend of other companies putting up weak numbers. Add in the Olympic spending, tough wholesale and store productivity comps, and our analysis that stretches to find more than 10% of CFO changes that end up being a near-term positive earnings event, and we’re more inclined to be on the negative side of this print. This is a perfect ‘buy on pullback’ stock.