“There’s a lot of things Congress can do, in the near term, not just in the long run, to make growth stronger.”

-Tim Geithner

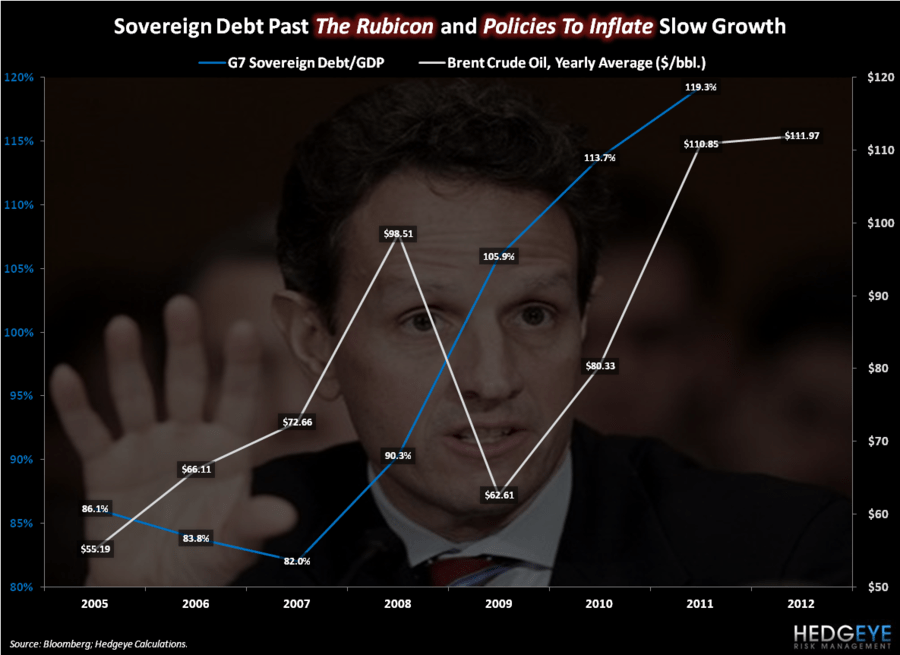

Having spent 54% of his born life in government, growing both deficits and debts as far as the eye can see, US Treasury Secretary Timmy Geithner’s Growth has been, if anything, consistent.

As President Obama goes into full campaign mode, his Top 2 central planners take center stage this week. Our almighty overlord of short-term asset price inflation will speak to commoners and journalists alike after his 215PM FOMC decision. Meanwhile, Geithner has been making his American/European media rounds for the last 24 hours.

The Germans in particular don’t care for the bailout policies to inflate inasmuch as they don’t care for Geithner’s economic partisanship. Now that Timmy is interviewing with Global banking outfits, he needs to be careful to not tell the Europeans what to do. Been there, done that – and he’s been mocked. That can be a bummer when negotiating a post Washington, DC employment agreement.

Back to the Global Macro Grind…

To paraphrase Geithner’s latest ideas for both Americans and Europeans alike: ‘We need to do more – more of what has not worked. There’s more of that to do – I believe that “deeply.” Do more.’

By “more”, he means more #BailoutBull policies for delinquent and/or underwater borrowers (US home buyers and Spanish banking conquistadors alike). By more, he means more government spending. By more, he means Big Government Intervention.

To review what doing “more” of that has done to both our economies and said “free” markets”:

- Shortened Economic Cycles (#GrowthSlowing)

- Amplified Market Volatility

In the very short-term, while No Volume; No Trust stock markets may or may not get this (depending on the latest rumor induced Viagra Rally in the S&P futures), the bond market understands this across intermediate and long-term durations, big time.

Geithner’s Growth (debt and deficits) slows growth. That’s not a rumor. That’s a fact. That’s why:

- 10-year US Treasury Yields continue to make lower-lows since #GrowthSlowing picked up on the downside in March

- Russell2000 (broad measure of US liquidity risk and equity exposure) stopped going up on March 26th

- That’s why US Equity market volatility (VIX) bottomed YTD on the same day that the Russell2000 topped (March 26th)

Bernanke’s Growth (asset price inflations) slows growth too. For July, this is best illustrated by the SP500’s Sector returns:

- Energy (inflation expectations) = UP +4.94%

- Consumer Discretionary (growth expectations) = DOWN -0.55%

Again, to review – INFLATION IS NOT GROWTH.

US Consumption represents the 71% that I don’t hear the Democrats talking about inasmuch as I didn’t hear the Republicans talking about it under Bush. That’s the 71% of the US Economy (GDP). And it’s been getting jammed by the likes of Bernanke and Geithner since at least 2006. Policies to debauch the Dollar and inflate oil prices at the pump are a colossal failure of Keynesian sense.

And it’s not just US Consumption Growth that slows when food/energy prices grow. Global Growth does too. Today’s reminder from the Big 3 Macro countries that will report gravity (economic data) for July continue support that:

- China’s PMI (manufacturing) hits its lowest level in 8 months

- Germany’s PMI hits a fresh YTD low of 43 for July (versus 45 in June)

- USA’s PMI is due out later this morning and could easily come in the low 50s (versus 52.9 in June)

In other words, the other side of “growth” that the Keynesians of the 112th Congress are being chastised to “stimulate” (export manufacturing) isn’t growing either. On a net basis (Exports minus Imports), exports were a negative drag on Q2 2012 US GDP.

After all this cochamamy stimuli “growth” talk and defict/debt spending, both US Consumption and Manufacturing Growth are slowing, at the same time. That’s not progress. That’s regressive. That’s why I still think the only real (inflation adjusted) “growth” solution is not doing more – it’s changing the lineup, and getting these failed central planners out of our way.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1, $102.46-105.49, $82.21-82.92, $1.20-1.23, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer