POSITIONS: Short Industrials (XLI)

We too will do whatever it takes to manage the risk of what’s becoming a proactively predictable range. As long as these central planners continue to encourage reckless bailout expectations like they did in 2008, the probability of a big move lower rises.

Our fundamental research view of #GrowthSlowing reminds us why Industrials (GROWTH) continue to underperform Energy (INFLATION) here in Q3. Short term commodity price inflations are not growth. They slow growth even further. It’s not only a shame that Bernanke has not yet acknowledged that; it’s going to be his legacy (and our economic risk) if he continues to perpetuate it.

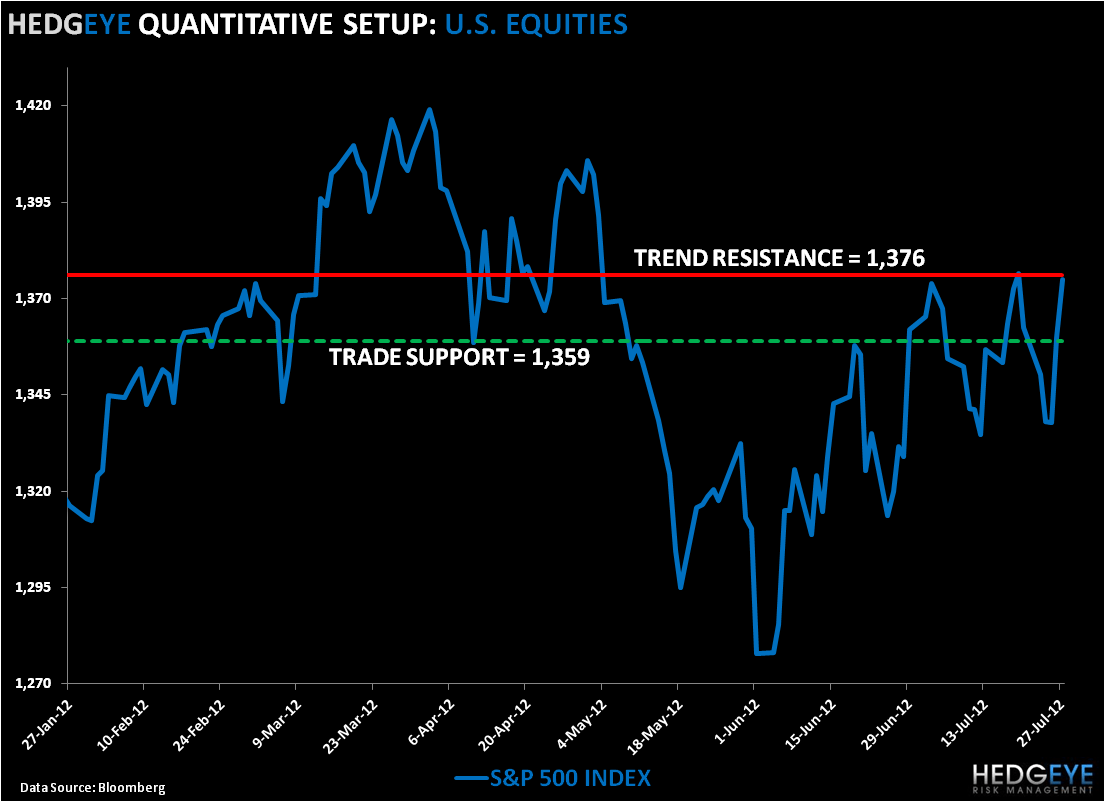

Across our risk management durations, here are the lines that matter to me most:

- Intermediate-term TREND resistance = 1376

- Immediate-term TRADE support = 1359

If 1359 snaps, this market will look as bad as it did pre the whatever thing from Draghi. If it doesn’t, we’ll just keep managing the risk of this 1 range. I’d like to see another no-volume intraday screamer > 1376 to short SPY itself.

Enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer