Even the areas we thought IGT would deliver fell short.

We had concerns going into the quarter but we’re still baffled by IGT’s FQ3 performance. We thought international would be a bright spot and we were wrong. Possibly even more confusing was management’s almost complete denial that there are any issues. Maybe that denial explains why they would buy back a whopping 21 million shares ahead of a major punt. While some for-sale units may have slipped out of this quarter and into the next, management must have known that this was not going to be a “good” quarter. Maybe they felt they needed the 2c quarterly accretion to maintain their guidance and it was worth overpaying for the stock to get it.

Either way, the unchanged guidance – even with the additional 2c – means that the pressure is on for FQ4. At this point, the mid-point of their guidance looks like a big stretch. Our 31c implies the low end of the range and even on that we feel like there is limited visibility.

The Details:

There was so much that was wrong with the quarter, that we’ll start with the only 2 things that weren’t bad

The Good:

- North American Unit sales were 1,000 better than we expected

- 900 of the beat was due to shipments of Canadian replacement units that we didn’t expect until the September quarter

- There were also some used units in there so it’s unclear what “new” units shipped were. We suspect that the used unit sales may have been participation or lease units converting to sale rather than true “used” unit sales.

- Interactive revenues were $3MM ahead of our expectations

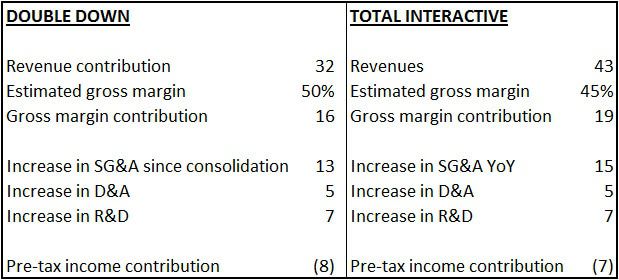

- We estimate that Double Down revenues were $32MM this quarter, just slightly better than the quarterized result of $24MM in F2Q for 72 days of consolidation

- Other interactive revenue of $11MM

The Bad (and The Ugly):

- Core gaming operations business (excluding interactive):

- Despite growing their install base by 3,600 units YoY, core gaming operations revenue declined 2% YoY and we estimate that gross margin declined 3% YoY

- Yields on participation declined 7% YoY and 4% QoQ (June is usually seasonally stronger for yields)

- Margins on the core business were down about 70bps YoY

- International game shipments grew 3% YoY and box sales declined by $15MM YoY

- So much for double digit growth in international and growing market share.

- We were wrong here as we thought this would be a quarter of progress.

- Mix/schmix… Product ASPs were terrible

- NA ASPs declined 8.5% YoY

- International ASPs were down 9% YoY

- Non-box sales in NA were down 20% YoY

- What happened to the Revel system deal?

- SG&A came in at the high end of guidance despite revenues coming in at the low end

- Double Down

- Memories of Server Based gaming?

- Despite IGT telling us about how accretive this acquisition has been and how well it’s performing, the math says otherwise.