We advised not staying short, but staying away, from this stock on the print. That ended up being the wrong call; the sell-off we were looking for happened more abruptly than we were expecting. We still see risk in the stock from here. Below we offer some takeaways and a recap of the quarter.

Takeaways

Buffalo Wild Wing’s quarter (recap below) was disappointing. Same-store sales missing expectations and, more predictably, elevated food costs led to a 7% miss on the bottom line. Here are the key takeaways:

1. Management layered on roughly one point of price in July bringing the total run rate to 3% for the third quarter. On September 3rd, with the rollout of revised menus, the company will take an additional 1%, bringing the run rate to 4% for the fourth quarter.

HEDGEYE: We believe that Buffalo Wild Wings’ competitive set may be broader than some think. Running price at 4% versus Food Away from Home CPI at ~3% could negatively impact traffic. CMG struck a cautious tone when discussing price, and consumer demand in general, on its earnings call last Thursday. Even with much less price on the menu than a year ago, CMG is not seeing an uptick in traffic that some were expecting. CFO John Hartung said, on price, “when a lot of restaurants get resistance, when they increase prices, they either see resistance and people spending less on each visit or they visit less. We don't usually see that. So last year when we raised prices, we didn't see any kind of decline in transactions. We didn't see any kind of decline in average check.” If Chipotle is observing some incremental softness in consumer demand, we believe it is reasonable to assume that all restaurant companies are experiencing it to some degree.

2. Management lowered FY12 guidance from 20% net income growth, provided on April 24th, to 15-20% net income growth.

HEDGEYE: We believe that there is further downside to that guidance. Our range of expectations is for EPS growth of between 11-14% for FY12.

3. The commodity cost set up for this company is not favorable. Corn prices remaining elevated suggest that chicken wing prices may take longer to fall than many have been anticipating. Management said, “It’s hard to believe that wing prices could go much higher”. Chicken wing prices were up 86% versus 2Q11 levels and the remainder of the commodity basket was up roughly 3% year-over-year. For 3Q to-date, wing prices are tracking roughly 70% above 3Q11 levels.

HEDGEYE: An upgrade on the EPS miss last quarter was based on the chicken wing conversation turning from higher prices to lower prices. We believe that consensus is now much less certain about chicken wing prices declining in the near future, particularly given recent movements in the grain markets and the ongoing struggles of the food processors within the chicken industry.

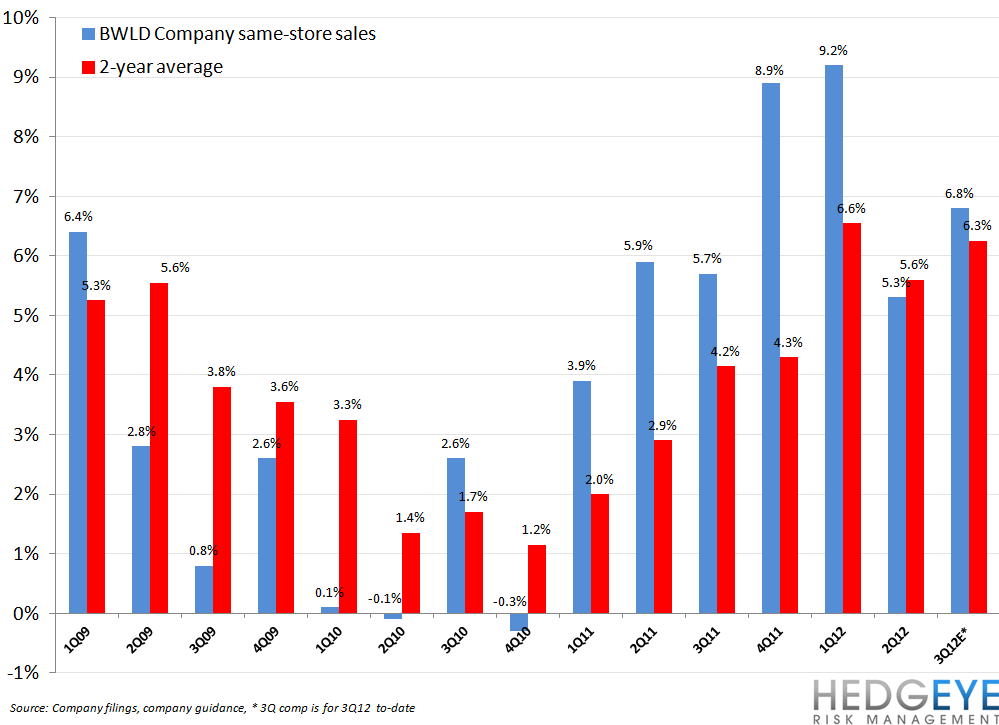

4. Same-restaurant sales growth for 3Q to-date at company-owned stores was +6.8%. This implies a sequential acceleration in two-year average trends from 2Q.

HEDGEYE: In his monthly write-up, Malcolm Knapp mentioned a shift from June to July related to the fourth of July this year that favorably impacted casual dining revenues this month. Additionally, management mentioned one additional UFC event versus the same period last year that will benefit traffic for the quarter. Other non-recurring factors in the third quarter include a positive impact from the NFL adding Thursday night games versus 3Q11. Despite these positives, there are many other variables, such as the elasticity of demand, that remain to be seen. Our sense from this conference call was that the Wall Street community is far less trusting of this management team today than it was in April when the company last reported. The line of questioning was far more skeptical and we believe appropriately so. That management can navigate the delicate path between protecting margins and not overly discouraging traffic in the current cost environment is less than certain.

2Q12 Earnings Recap

BWLD missed on the top-line largely due to comps coming in at 5.3% at company-operated restaurants versus 6.1% consensus. Earnings per share of $0.62 also missed the Street’s target of $0.67 as food costs “moderated” the company’s earnings growth, according to management. Earnings per share grew 7.7% year-over-year versus 15.8% consensus. The tables below offer further details.

Howard Penney

Managing Director

Rory Green

Analyst