TODAY’S S&P 500 SET-UP – July 24, 2012

As we look at today’s set up for the S&P 500, the range is 25 points or -1.45% downside to 1331 and 0.41% upside to 1356.

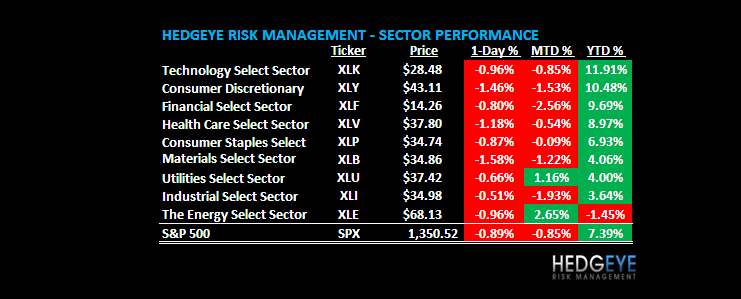

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/23 NYSE -1601

- Down versus the prior day’s trading of -1007

- VOLUME: on 07/23 NYSE 742.90

- Decrease versus prior day’s trading of -25.90%

- VIX: as of 07/23 was at 18.62

- Increase versus most recent day’s trading of 14.44%

- Year-to-date decrease of -20.43%

- SPX PUT/CALL RATIO: as of 07/23 closed at 1.23

- Down from the day prior at 1.99

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 36

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.43%

- Unchanged from prior day’s trading

- YIELD CURVE: as of this morning 1.22

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook retail sales

- 8:45am: Fed’s Bernanke speaks to the Children’s Defense Fund National Conference on early childhood education via prerecorded video

- 10am: Markit US PMI Preliminary, July, est. 52 (prior 52.9)

- 10am: Richmond Fed Manuf Index, July, est. -1 (prior -3)

- 10am: FHFA House Price Index M/m, May, est. 0.4% (prior 0.8%

- 11am: Fed to purchase $1.5b-$2b notes due 2/15/36-5/15/42

- 11:30am: U.S. to sell 4-wk, 52-wk bills

- 1pm: U.S. to sell $35b 2-yr notes

- 4:30pm: API inventories

GOVERNMENT:

- House, Senate in session

- Senate hearing on consumer impact of broadcast-cable disputes: CBS, TWC

- Senate Judiciary holds hearing on super PACs, 2:30pm

- Senate Energy holds hearing on natural gas and transportation, 10am

- House Energy hears from Chairman Allison Macfarlane, three NRC commissioners at oversight hearing, 10am

- House Financial Services’ Consumer Credit subcommittee hearing on legislation to create a federal charter for non- depository lenders, 10am

- House Financial Services Insurance Subcommittee hearing on Dodd-Frank Act’s impact on insurance industry, 2pm

- Senate Banking Subcommittee on Financial Institutions and Consumer Protection holds hearing “Private Student Loans: Providing Flexibility and Opportunity to Borrowers;” Sallie Mae President Jack Remondi to testify, 2:30pm

- NHTSA hearing on proposal to mandate anti-rollover technology in heavy-duty trucks, 10am

- U.S. Chemical Safety Board releases preliminary findings from the investigation into BP’s 2010 Macondo well explosion in the Gulf of Mexico, 9:05am

- International Swaps and Derivatives Association holds a Dodd-Frank Transaction Reporting Conference to review requirements’ impact on participants in the $648t global swaps market, 8:15am in New York

- CFA exam level I & II results are e-mailed after 9am

WHAT TO WATCH:

- Germany pushes back after Moody’s lowers rating outlooks

- Goldman Sachs, Bain Capital and Carlyle urged federal judge to dismiss lawsuit accusing largest investment banks, P/E firms of conspiring to rig bids on leveraged buyouts

- Treasury Secretary Timothy Geithner said President Obama “absolutely committed” to letting tax cuts for wealthiest Americans expire as scheduled, in interview on “Charlie Rose” show yesterday

- Apple lost Dusseldorf appeals court bid to ban sales of Samsung Electronics’s Galaxy 10.1N tablet computer

- Rosneft starts talks with BP on buying stake in Russia venture

- Compensation consultant to Best Buy’s board quit after company awarded more than 100 managers retention bonuses without tying them to performance

- China manufacturing gauge shows slowdown may be ebbing

- Spain’s borrowing costs rise at 3-mo. bill auction

- Home values posted first Y/y increase since 2007 in 2Q as U.S. property market began to lift off bottom, Zillow said

- Apple plans to send security manager to Black Hat USA 2012 to discuss iPhone, iPad, making first appearance at one of the hacking world’s largest conferences

- U.S. Chemical Safety Board releases preliminary results from BP/Macondo investigation

EARNINGS:

- Spirit Airlines (SAVE) 5:45am, $0.47

- RF Micro Devices (RFMD) 4pm, $0.01

- Whirlpool (WHR) 6am, $1.69

- Total System Services (TSS) 4pm, $0.32

- EI du Pont de Nemours (DD) 6am, $1.46

- FMC Technologies (FTI) 4pm, $0.48

- Polaris Industries (PII) 6am, $0.91

- Edwards Lifesciences (EW) 4pm, $0.65

- Synovus Financial (SNV) 6am, $0.02

- Buffalo Wild Wings (BWLD) 4pm , $0.68

- Centene Corp (CNC) 6am, $(0.10)

- Panera Bread (PNRA) 4pm, $1.43

- NorthWestern (NWE) 6am, $0.29

- Hatteras Financial (HTS) 4pm, $0.89

- Potlatch (PCH) 6:45am, $0.09

- Robert Half International (RHI) 4pm, $0.35

- Rogers Communications (RCI/B CN) 6:47am, C$0.86

- Norfolk Southern (NSC) 4:01pm, $1.53

- Altria Group (MO) 6:58am, $0.57

- Nabors Industries (NBR) 4:01pm, $0.37

- Reynolds American (RAI) 6:58am, $0.76

- Illumina (ILMN) 4:01pm, $0.37

- EMC (EMC) 7am, $0.39

- American Campus Com. (ACC) 4:01pm, $0.49

- Simon Property Group (SPG) 7am, $1.81

- Ezcorp (EZPW) 4:01pm, $0.62

- Biogen Idec (BIIB) 7am, $1.56

- Questcor Pharmaceuticals(QCOR) 4:02pm, $0.65

- Lexmark International (LXK) 7am, $0.88

- Thoratec (THOR) 4:02pm, $0.44

- Penn National Gaming (PENN) 7am, $0.64

- TripAdvisor (TRIP) 4:03pm, $0.41

- Western Union (WU) 7am, $0.43

- Broadcom (BRCM) 4:05pm, $0.67

- Ametek (AME) 7am, $0.46

- Netflix (NFLX) 4:05pm, $0.05

- Regions Financial (RF) 7am, $0.14

- Juniper Networks (JNPR) 4:05pm, $0.16

- Husky Energy (HSE CN) 7am, $0.36

- Tempur-Pedic International (TPX) 4:05pm, $0.38

- Under Armour (UA) 7am, $0.05

- Riverbed Technology (RVBD) 4:05pm, $0.21

- Pentair (PNR) 7am, $0.80

- Polycom (PLCM) 4:05pm, $0.20

- Waters (WAT) 7am, $1.16

- Aflac (AFL) 4:07pm, $1.61

- AT&T (T) 7:25am, $0.63

- Compuware (CPWR) 4:13pm, $0.07

- Rockwell Collins (COL) 7:30am, $1.15

- Aaron’s Inc (AAN) 4:15pm, $0.47

- Domino’s Pizza (DPZ) 7:30am, $0.46

- CH Robinson Worldwide (CHRW) 4:15pm, $0.71

- Anixter International Inc (AXE) 7:30am, $1.50

- International Game Tech. (IGT) 4:15pm, $0.29

- FirstMerit (FMER) 7:30pm, $0.28

- Altera Corp (ALTR) 4:15pm, $0.39

- PrivateBancorp (PVTB) 7:30am, $0.16

- Cymer (CYMI) 4:25pm, $0.04

- Lockheed Martin (LMT) 7:30am, $1.91

- WR Berkley (WRB) 4:29pm, $0.61

- United Parcel Service (UPS) 7:45am, $1.17

- Apple (AAPL) 4:30pm, $10.37

- Ryder System (R) 7:55am, $0.93

- Unisys (UIS) 4:30pm, $0.51

- Illinois Tool Works (ITW) 8am, $1.10

- Trustmark (TRMK) 4:30pm, $0.44

- Sigma-Aldrich (SIAL) 8am, $0.97

- Linear Technology (LLTC) 5pm, $0.45

- Paccar (PCAR) 8am, $0.81

- Ctrip.com (CTRP) 5pm, $0.20

- Peabody Energy (BTU) 8am, $0.53

- Range Resources (RRC) 5pm, $0.06

- Six Flags Entertainment (SIX) 8am, $0.73

- Bell Aliant (BA CN) 5pm, $0.43

- Gentex (GNTX) 8am, $0.29

- Acadia Realty Trust (AKR) 5pm, $0.24

- Lennox International (LII) 8am, $0.96

- Valmont Industries (VMI) 5:30pm , $2.16

- Liberty Property Trust (LRY) 8am, $0.63

- Cabot Oil & Gas (COG) 5:31pm, $0.06

- Wabtec (WAB) 8:05am, $1.23

- Suncor Energy (SU CN) After-mkt, $0.73

- Avery Dennison (AVY) 8:30am, $0.54

- Community Bank System (CBU) Aft-mkt, $0.50

- Neogen (NEOG) 8:45am, $0.26

- Newfield Exploration (NFX) Aft-mkt, $0.64

- Carlisle (CSL) Bef-mkt, $1.28

- UMB Financial (UMBF) Aft-mkt, $0.69

- Jarden Corp (JAH) Bef-mkt, $1.10

- Rock-Tenn (RKT) Aft-mkt, $1.02

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – bearish TREND; bullish TRADE; we’ll stay short it with a wall of TREND line resistance up at $108.37 Brent. The only thing that can get US and Chinese Growth back on track is a sustainable drop in Brent back below $90. With Qe drug addictions in this market’s whisper, good luck with that.

- Europe Heat Wave Wilting Corn Adds to U.S. Drought: Commodities

- China Ousts U.S. in Canada Oil Market With Bid for Nexen: Energy

- Investors Plow Cash Into Crops as Gold Jilted: Chart of the Day

- Crude Trades Near One-Week Low on Worsening European Crisis

- Copper Seen Rising as China Factory Contraction May Be Slowing

- Corn, Soybeans Tumble on European Risk, Forecast for Some Rains

- LNG Goes Extra 9,800 Miles as Europe Spurs Record Rates: Freight

- Cocoa Climbs on Speculation El Nino Will Cut Output; Sugar Falls

- U.S. Gas Futures Near Seven-Month High on Warm Weather Forecasts

- U.K. Natural Gas for Today Advances as Norwegian Imports Decline

- Illinois Corn, Soy Yields Drop From 2011, Doane Crop Tour Shows

- South Korea Buys 6,000 Tons of High-Grade Aluminum in Tenders

- Cocoa Usage Seen Falling as Processors Erode World Butter Glut

- Copper Gain Seen as New-Home Sales Spur Demand: Chart of the Day

- Gold Set to Decline in London as Europe Concern Bolsters Dollar

- Morgan Stanley Increases 2012 U.S. Gas Price Forecast by 14%

CURRENCIES

EUROPEAN MARKETS

GERMANY – for once we actually agree with a Moody’s move on the margin; Germany’s #GrowthSlowing slope has accelerated on the downside in the last 6 weeks, and that matters. This morning’s PMI print of 43.3 for July in Germany is an absolute bomb (45.0 in June) – German GDP growth could easily go negative y/y in Q3 (consensus has it up +0.5%).

ASIAN MARKETS

HANG SENG – nasty 2-day 4% drop in a major leading indicator in our model that certainly trumps whatever flash there was in the made-up HSBC PMI print of 49.5; Hang Seng, like KOSPI, is now back into a Bearish Formation (both of these indexes have led the SP500 and German DAX since March, so watch them both closely – Asian Growth is Too Big to Bail).

MIDDLE EAST

The Hedgeye Macro Team