This note was originally published at 8am on July 09, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Farmers are good fighters but poor politicians.”

-Victor Davis Hanson

I spent last week with my family up on the big lake they call Gitchee Gumee. It was a much needed vacation where I was finally able to dig into a book that has been recommended to me multiple times, The Soul of Battle, by Victor Davis Hanson.

The first part of the book focuses on a Theban general Cicero called “The First Man of Greece” (Epaminondas) and the epic story of how he led a bunch of Boeotian farmers to crush the Spartans. These were not King Leonidas’ warriors from the movie “300” who held Thermopylae in 480BC. These were the tired and passionless troops of 371BC Sparta who fought for politicians.

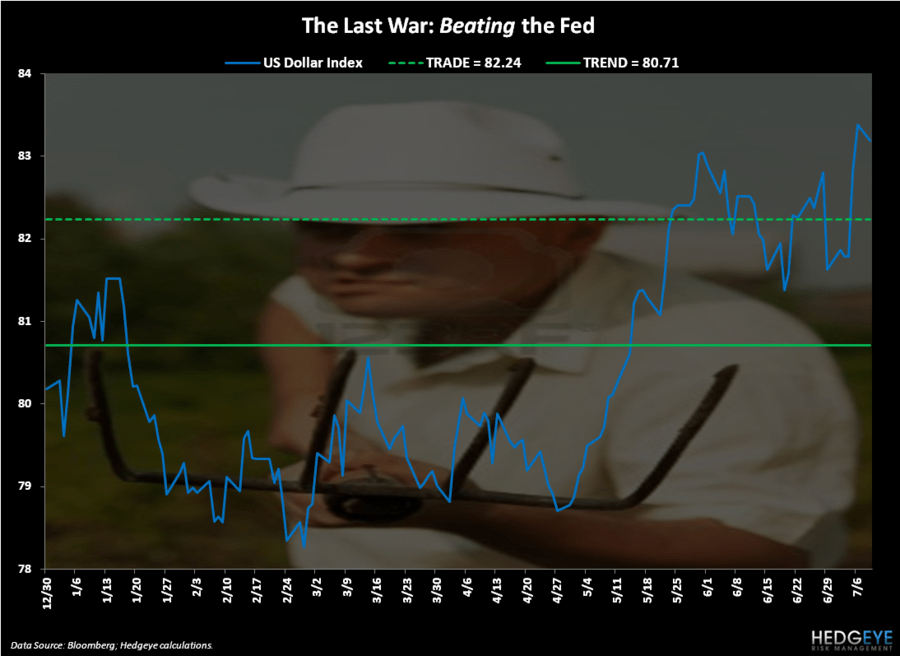

Since introducing our Q2 Global Macro Theme of The Last War: Fighting The Fed, we have been pounding our pitchforks into the keyboards reminding you that an end to a politicized US Dollar could bring about the return of the King. Since April, that King has been Cash. The People who use US Dollars as their currency will continue to fight alongside us.

Back to the Global Macro Grind…

Last week’s highlight in the Global Macro matrix was the US Dollar’s charge to fresh YTD highs. This is a currency war, so the other team (Europe’s currency) losing matters. With the Euro down -3.2% on the week, the USD Index closed up +2.1% to $83.38.

Strong Dollar Deflates The Inflation – some of us who like to buy things on red enjoy that. It allows us to invest some of our hard earned Dollars at better prices. With the US Dollar up last week, here’s how some of the week-over-week price deflation looked:

- WTIC Oil = -0.9%

- Gold = -1.3%

- Silver = -1.8%

- Copper = -2.2%

- Cotton = -1.9%

- SP500 = -0.5%

Behold, a 50 basis point deflation in the US stock market. Call in the cavalry, we need Qe5!

Let’s get real here folks. If the US stock market can’t sustain taking a few shots from the only thing that will save her in the end (a strong and credible currency backed by conservative fiscal and monetary policy), America will be looking just like Europe in no time.

That’s the long-run. In the shorter-run, given the US equity market’s manic depressive state, we can’t assume that Strong Dollar = Stronger US Consumption and Stronger/Sustainable Growth at the flip of a switch. Getting people off the Qe4 expectation drugs will take time; so will deflating food and energy prices.

In the meantime, the market has to deal with 3 very big things aligned with economic gravity this week:

- US Growth Slowing (both ISM reports and the unemployment update last week were terrible)

- China Growth Slowing (all of the June and Q2 data due this week)

- Q2 Earnings Season

Ah, the ole earnings season – what will the “fundamentals” bring?

It wasn’t long ago (March-April) that the bull case for US stocks was “growth is back, earnings are great, and stocks are cheap.” Therefore, assuming the bull case isn’t solely based on bailouts, it stands to reason that we should wait and watch for the reaction to #GrowthSlowing, earnings deteriorating, and stocks being valued on the right (instead of hopeful) numbers.

What’s already been discounted? I do not know.

Do you?

All I can tell you is what I have been telling you since we shorted Industrials on March 12th – you do not want to be buying pro-cyclical Sectors (Industrials, Energy, Basic Materials) at the top of another cycle.

Industrials (XLI) are already down -1.3% for July (versus the SP500 -0.55%), so I am not going to be willfully blind to the idea that some of the slowdown hasn’t already been priced in. But neither am I going to blindly accept forecasts from politician like CEOs that today’s outlook hasn’t changed dramatically from the conference calls they hosted in April.

Farmers Fight about the weather forecast too. But sometimes it’s pretty clear that everyone is getting wet while it’s raining.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1551-1587, $96.90-103.02, $82.42-83.49, $1.22-1.25, and 1346-1360, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer