American Express (AXP) just can’t get its act together. After reporting its second quarter earnings, it’s clear that our macro Growth Slowing call is kicking into gear. The company reported large sequential deceleration in every growth category.

The company isn’t growing card volumes and instead is watching them evaporate, particularly in Europe. Taking into account that 100 basis points equates to one percentage point, look at the downward spiral that is AXP below:

US volumes slowed 380 bps to 8.7% YoY in 2Q vs. 12.5% in 1Q. International volumes slowed 920 bps to 3.0% YoY growth in 2Q from 12.2% YoY growth in 1Q. Right now the business is split 2/3 US and 1/3 International. As a result, overall growth slowed 570 bps to 6.7% YoY in 2Q from 12.4% last quarter.

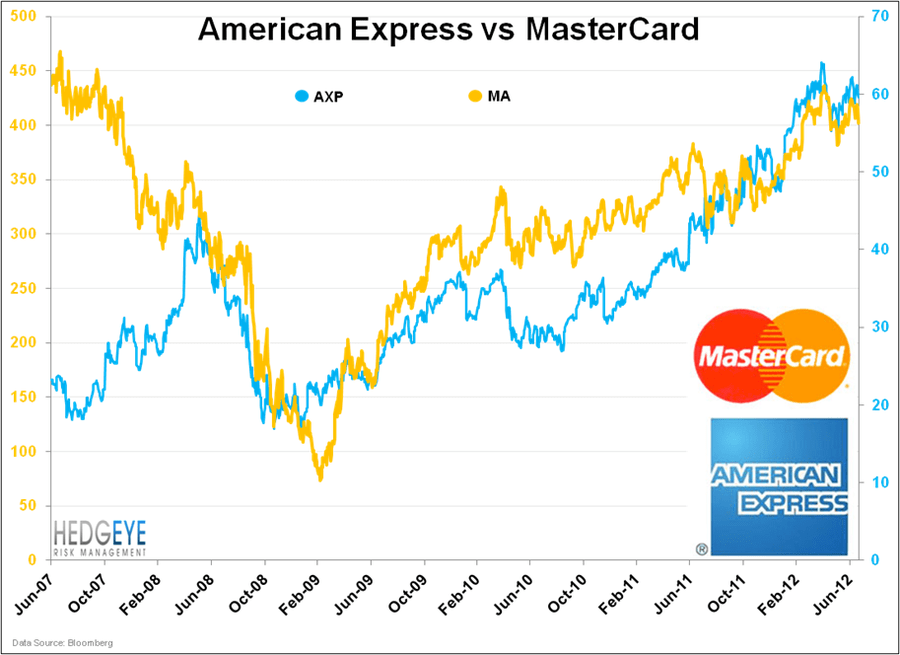

Conversely, MasterCard (MA) is doing quite well. Over the last five years, MasterCard is up 157% compared with American Express’ -12%. It’s easy to see why we’re bearish on AXP and bullish on MA. Visa (V) is also a winner, up over 95% during the same five year period. V and MA are doing well in the broader market. The Financials SPDR (XLF) lost 55% in that five year period, too.

The chart says it all. While MasterCard may be a little pricey, trading at 19x earnings, it’s golden compared to American Express’ performance and outlook.