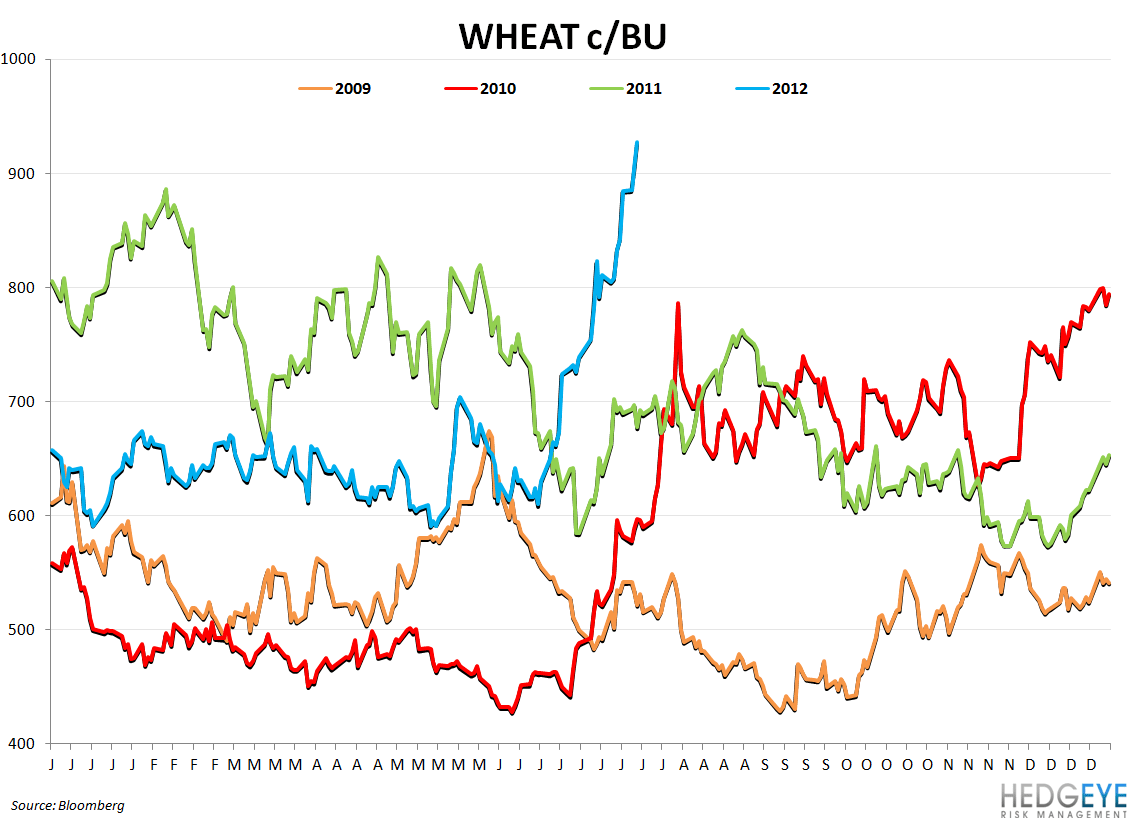

What news reports are calling “the most expansive U.S. drought in more than a half century” intensified this past week, sending already-high grain prices higher still. Almost all of the other food-related commodities we track followed suit as the dollar also declined.

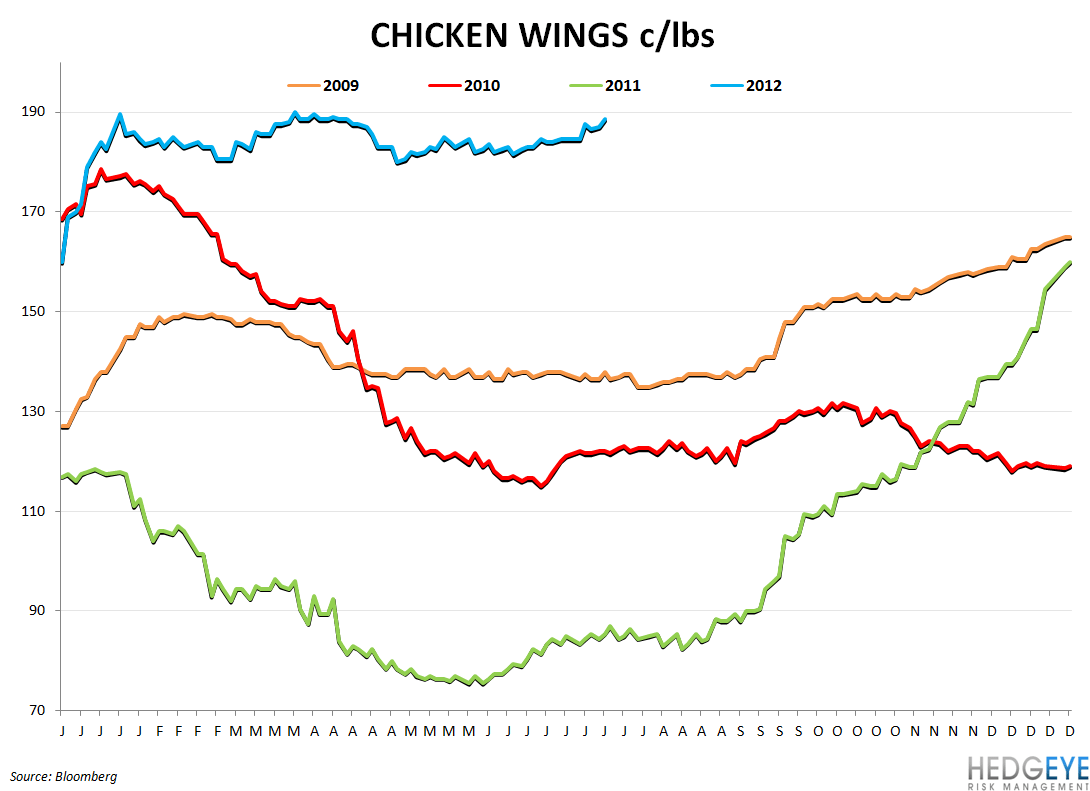

With regard to corn, in particular, the response in Food Processor stocks has been as one would expect. PPC and SAFM have underperformed the group, likely due to the chicken industry’s exposure to corn prices.

Before our post on July 10th, titled “BWLD: WINGSTOP COMPS POINT TO UPSIDE”, we would have argued that this was also a strong negative for Buffalo Wild Wings coming into the quarter, given the food cost headwinds it is facing. It remains a negative but an upside surprise to comps of the magnitude that our post outlines would likely trump any inflation concerns, at least in the immediate term.

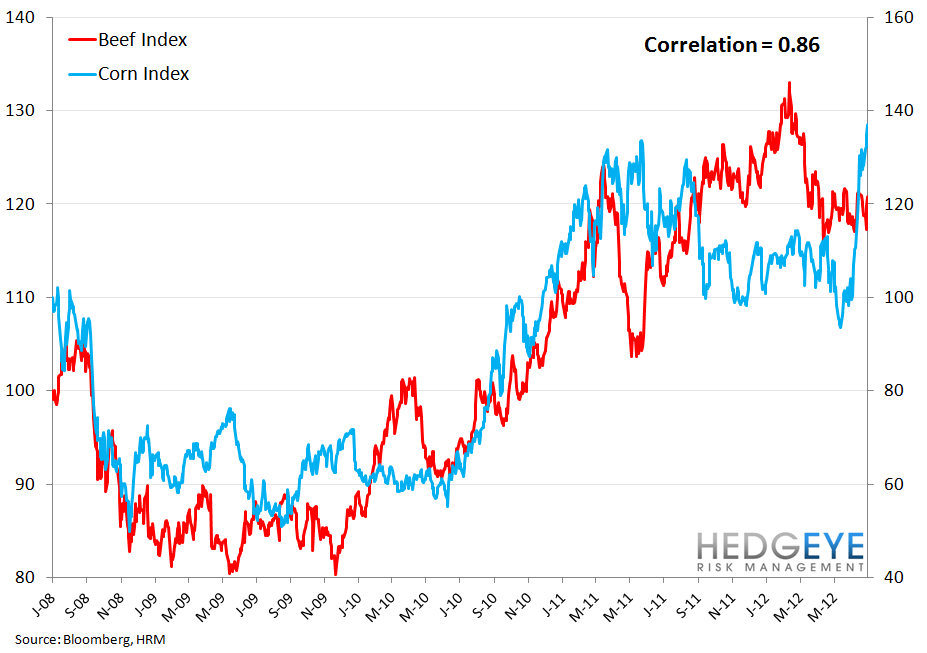

One commodity that has been somewhat surprising to us is beef. The weak economy is dragging U.S. beef exports lower but, when we consider the impact that last summer’s drought had on the size of the U.S. herd, the fact that rebuilding that herd is becoming more and more difficult, and the continuing loosening of restrictions in Japan on U.S. beef, there are reasons to believe that beef prices could climb higher over the next few months. The relationship between the two seems quite tight, as the chart below shows. If corn prices keep gaining or remain at these levels, we would expect beef to rise which would be a negative for TXRH, JACK, CMG, and WEN.

GAS PRICES

CORRELATION

CHARTS

Howard Penney

Managing Director

Rory Green

Analyst