With Manchester United looking to raise approximately $300mm in an IPO, we should take a minute to put a few things into perspective around the values of sports teams, and brands that endorse them.

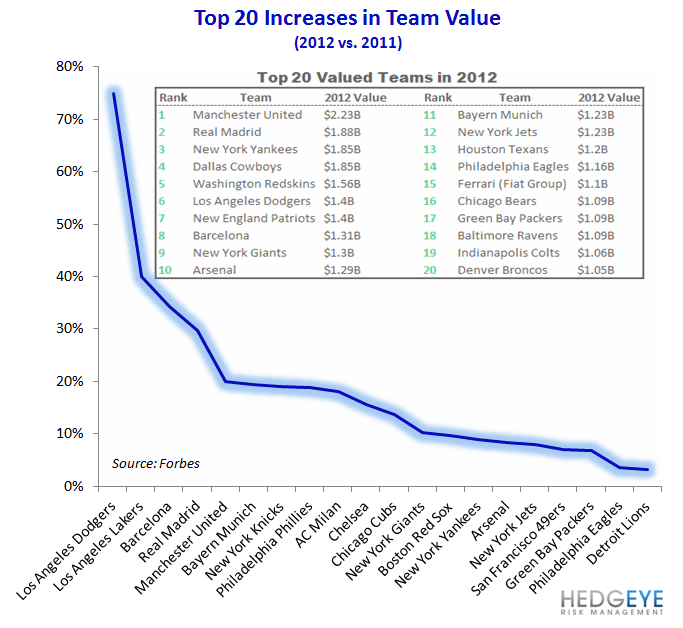

A) As it relates to the full value of Manchester United, it has nearly 400mm fans worldwide. Note to you/us Yankee fans who think it is the top team in the world – there are only 310mm people in the US, and outside our borders no one cares about the Yankees. Forbes ranks Manchester United as the number 1 team globally with a value of about $2.23bn. Next is Spain’s Real Madrid at $1.88bn. The Yankees manage to come in next in line at $1.85bn, but the interesting callout is that it is tied for third with the Dallas Cowboys. Then there’s a big step down to the Washington Redskins at $1.56bn, and no other teams passing the $1.5bn mark. As it relates to changes in value over the past year on the margin, here are some callouts amongst the top 50 franchises in looking at last year’s Forbes values vs what it is reporting today.

- The most notable point, by far, is that the two teams with the greatest increase in value are both in Los Angeles. The next two teams on the list are in Spain (FC Barcelona and Real Madrid). We get the California angle, but is Forbes watching what’s going on in Spain? Not so sure about that.

- As bullish as a $1.4bn valuation might sound for the Dodgers, the team was purchased by Guggenheim Baseball in April for $2bn which was based on an impending local TV deal that is expected to be worth nearly $3.5bn in cash and equity. Steve Forbes is probably getting several angry phone calls this week questioning valuation math.

- Despite the Juventus Football Club moving into a new stadium this year with a 49% increase in capacity, it fell off the top 50 list and was replaced by the Texas Rangers. Now valued at $674mm, the Rangers won the AL West only to lose in the World Series for the second straight year in game 7. Regardless, attendance reached Franchise history highs and the team struck a 20yr cable deal with Fox Sports Southwest beginning in 2014 valued at $3bn.

- Only 5 of the top 20 clubs are Football/Soccer.

- 12 of 20 are US rules (NFL) Football. There’s a little snippet for NFL fans that hate soccer.

B) It just so happens that Nike does, in fact, endorse Manchester United and pays in the vicinity of $40mm per year for the rights to manufacture ManU replica kits. It is anticipated that come 2015 when Manchester United’s current deal with Nike expires, they will be looking to ink a deal worth up to £600m over 10 years. This is pre-contract negotiating in the press, but it’s interesting to note that if they get £60 per year (nearly $95mm annually), Manchester United would have the highest valued contract amongst Nike's high profile endorsements topping The French National Football Team, FC Barcelona,~7 Lebron James’ and 314 Tim Tebows….