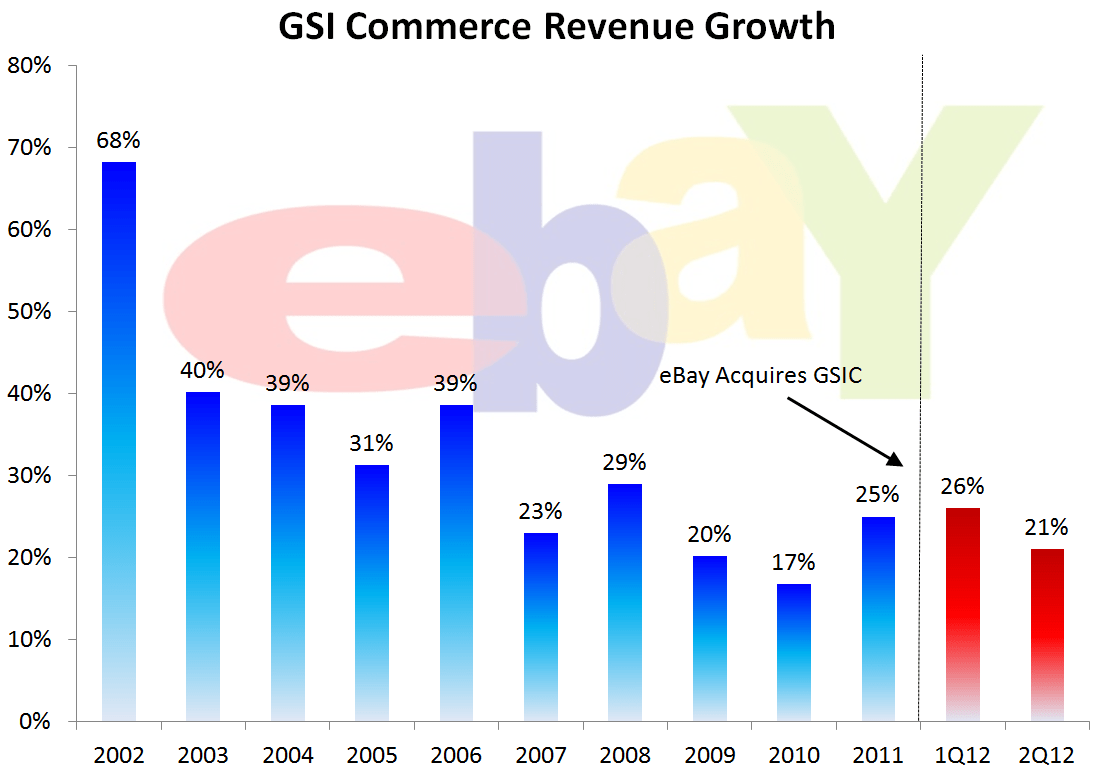

While not exactly the first metric people look at with eBay, the performance of GSI Commerce, which it acquired in June of 2011, is particularly important to us as a proxy for brick & mortar expansion into the digital marketplace. GSI (8% of eBay sales) specializes in creating, developing and running online shopping sites for brick and mortar brands and retailers (customers include but are not limited to Sport’s Authority, Dick’s Sporting Goods & Toys R Us). It might be too soon to judge, but since the acquisition, growth at GSI has gone in the wrong direction. It still rang in a healthy 21% comp in the latest quarter, though this was a 500bp deceleration from the 26% rate posted in both 4Q and 1Q. It’s not the end of the world, but the synergies have clearly yet to show themselves.