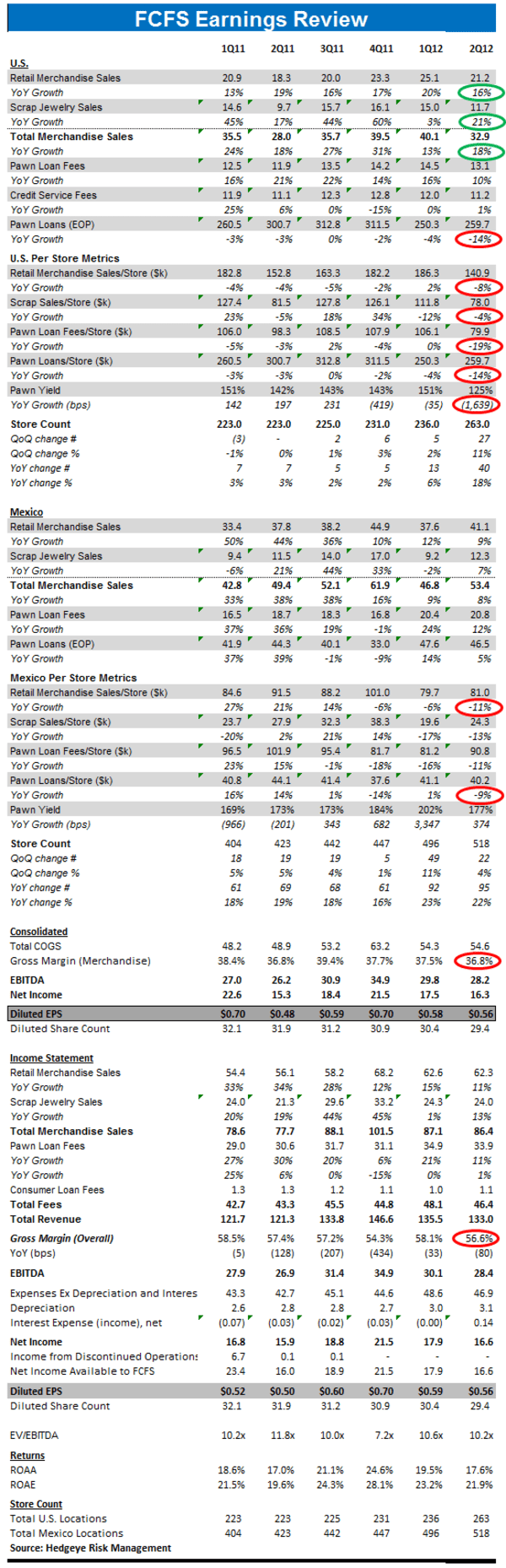

Our original call pre-earnings on First Cash Financial Services (FCFS) was that it would take a hit on earnings due to falling gold prices and the influx of “we’ll buy your gold now” stores popping up all over the place. That was our consensus on the pawn space as a whole. FCFS managed to beat expectations for Q2, but after speaking directly with management, we’re still cautious about this name.

Management pushed back on our argument. Since we had some valid discourse, we’ve decided to outline the points they made on the call below:

- Point 1: On the issue of gold, FCFS says it’s becoming a smaller portion of their business. US stores see gold for 60% of collateral, while Mexico only sees 20%. That’s significantly less than competitors in the pawn space like CSH and EZPW.

- Point 2: There are two types of customers: those trying to just sell their gold and those who are using valuable items (i.e. family heirlooms, wedding rings) for collateral that they ultimately want back.

- Point 3: FCFS is growing. From 2002 to 2Q12, they’ve gone from ~120 stores to 675 stores. The bottom line is that store growth has likely accounted for a larger portion of long-term revenue growth than we had assumed, which means that gold price tailwinds must have accounted for a smaller portion.

This quarter's results are consistent with our basic view on First Cash. The company is a solid operator with strong growth prospects baked into existing store count from acquisitions and new store openings. However, First Cash has significant gold exposure, though less than CSH and EZPW, and so long as gold prices are moving sideways to lower we think it will be hard for FCFS shares to hold their current level.