Claims Come Full Circle

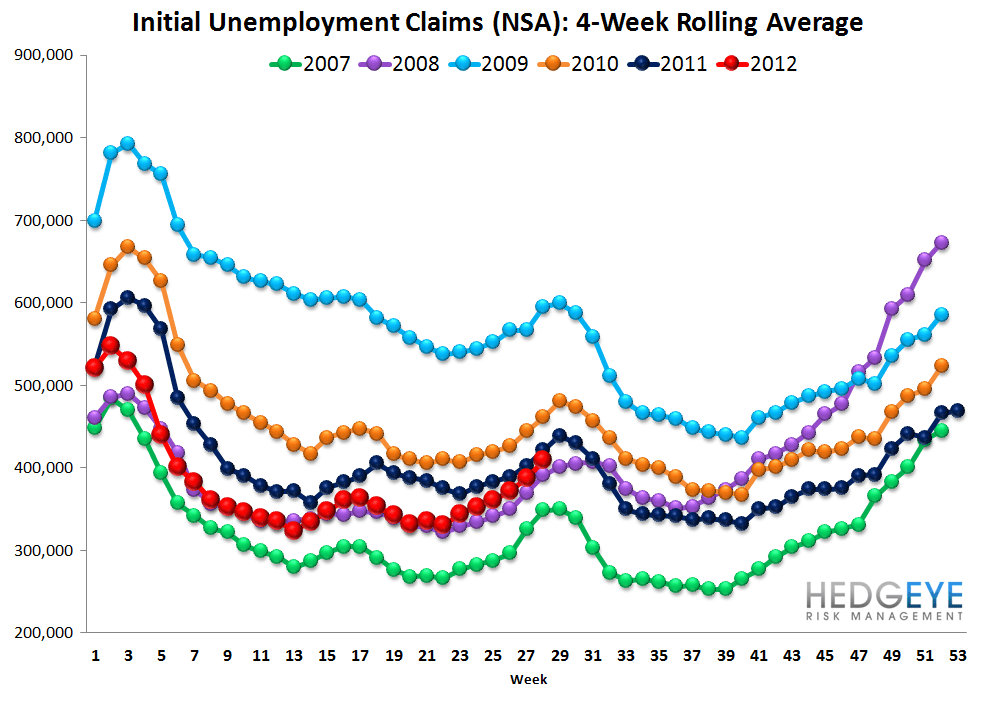

Initial jobless claims were 386k this past week, 36k higher than the prior week's number. There was a 2k upward revision to the prior week's data. The 4-week moving average, meanwhile, fell 1.5k to 376k. On a non-seasonally adjusted basis, claims rose by 11k. The YoY change in the non-seasonally adjusted series moderated to ~7% improvement from a ~8% run rate in the prior week. This last point is the most important. We use the YoY rate of change in non-seasonally claims to gauge the real underlying trend, considering the seasonal adjustment distortions that are taking place. That YoY rate of change has been slowly getting worse over the last few months, decelerating from a 10% YoY improvement to a 7% improvement currently. This suggests a real underlying slowdown, as opposed to the one created by seasonal adjustment distortions.

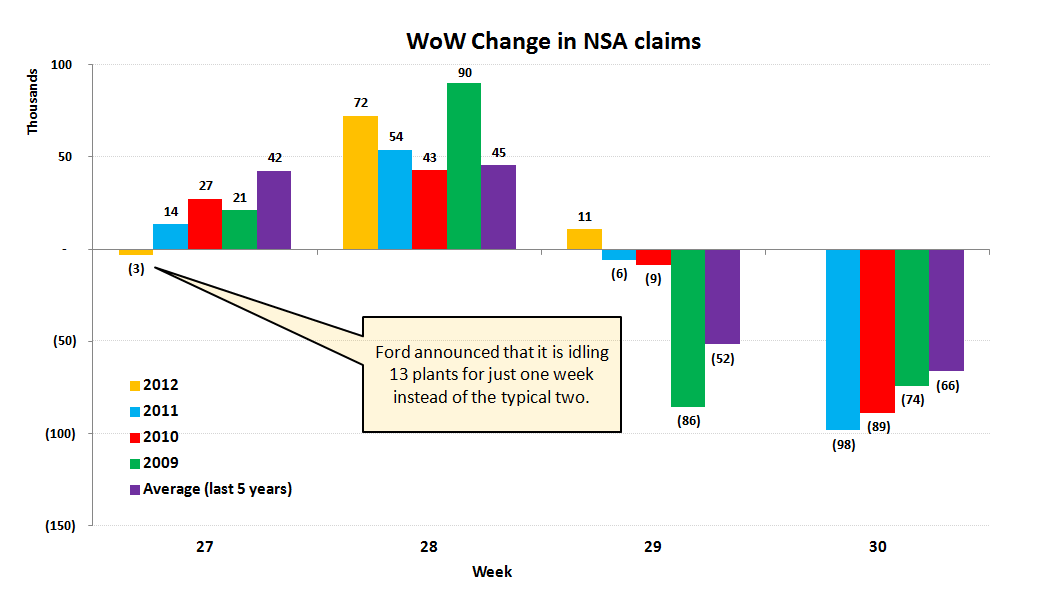

The Auto Distortions Correct

As a reminder, the distortions over the past three weeks all reflect differences in the timing of auto manufacturing layoffs from recurrent mid-summer plant idling. Last week claims rose 36k, while the two weeks prior to that saw claims fall a combined 36k, so we're back to square one.

Going forward, we still expect distortions in the seasonal adjustment factors to push claims higher from here. By the end of August, these distortions should begin to reverse and the data should start to look better again moving into the Fall months.

The 2-10 Spread

The 2-10 spread widened 2 bps WoW to 127 bps, as the ten-year treasury yield fell 2.5 bps to 150 bps. That's little comfort though as the curve overall is still exceptionally tight. We've seen plenty of evidence of the effect of this in bank earnings over the past 4 days. Our macro team expects the yield spread to continue to compress.

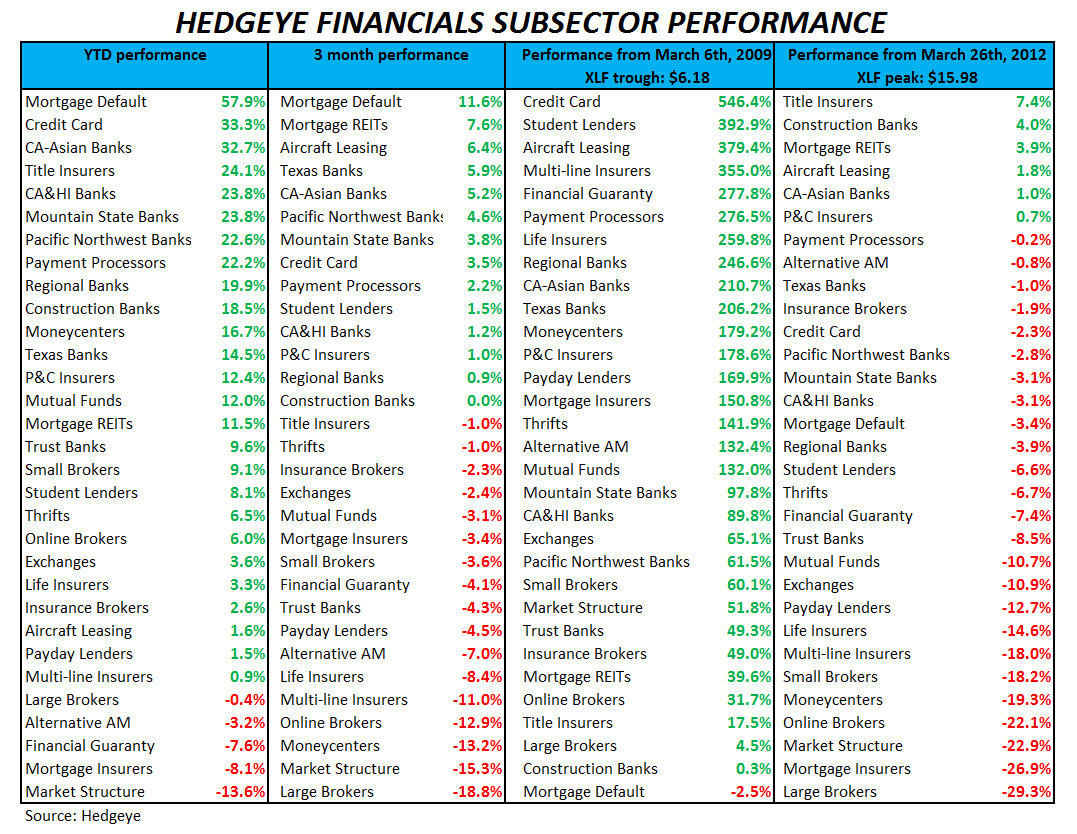

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.