TODAY’S S&P 500 SET-UP – July 18, 2012

As we look at today’s set up for the S&P 500, the range is 14 points or -0.93% downside to 1351 and 0.10% upside to 1365.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 07/17 NYSE 1036

- Up versus the prior day’s trading of -306

- VOLUME: on 07/17 NYSE 697.74

- Increase versus prior day’s trading of 15.89%

- VIX: as of 07/17 was at 16.48

- Decrease versus most recent day’s trading of -3.68%

- Year-to-date decrease of -29.57%

- SPX PUT/CALL RATIO: as of 07/17 closed at 1.04

- Down from the day prior at 1.47

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 36

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.49%

- Decrease from prior day’s trading at 1.51%

- YIELD CURVE: as of this morning 1.26

- Down from prior day’s trading at 1.27

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, July 13 (prior -2.1%)

- 8:30am: Housing Starts, June, est. 745k (prior 708k)

- 8:30am: Housing Starts M/m, June, est. 5.2% (prior -4.8%)

- 8:30am: Building Permits, June, 765k (prior 784k)

- 10am: Bernanke delivers monetary policy report to House

- 10.30am: DOE Inventories

- 11am: Fed to purchase $4.5b to $5.5b notes maturing Aug. 15, 2020-May 15, 2022

- 2pm: Fed releases Beige Book

GOVERNMENT:

- House, Senate in session

- House Armed Services holds hearing on budget sequestration effects, 10am

- Defense Secretary Leon Panetta, U.K. Secretary of State for Defense Philip Hammond hold joint press conference, 9:30am

- Equal Employment Opportunity Commission holds public meeting on Strategic Enforcement Plan, 9:30am

- Office of Personnel Management holds meeting of National Council on Federal Labor-Management Relations to make recommendations on improving services, cutting costs, 10am

- World Bank President Jim Yong Kim discusses global development at Brookings Institution, 1:30pm

WHAT TO WATCH:

- FDA approves Vivus’s weight-management drug Qsymia

- Housing starts may have climbed 5.2% in June

- Bernanke resumes semi-annual testimony at House today

- Facebook down 8.6% this week amid slowing-growth concerns

- DirecTV says it’s closer to deal with Viacom on channels

- Samsonite to buy High Sierra Sport for $110m NSN

- BOE Voted 7-2 as MPC Signals Rate-Cut Case May Be Reviewed

EARNINGS:

- Knight Capital Group (KCG) 6am, $0.10

- PNC Financial Services (PNC) 6:15am, $1.22

- BlackRock (BLK) 6:30am, $3.01

- Bank of New York Mellon (BK) 6:30am, $0.51

- US Bancorp (USB) 6:45am, $0.70

- Dover (DOV) 7am, $1.13

- Stanley Black & Decker (SWK) 7am, $1.52

- AO Smith (AOS) 7am, $0.67

- Bank of America (BAC) 7am, $0.15

- Northern Trust (NTRS) 7:14am, $0.75

- Honeywell International (HON) 7:30am, $1.11

- St Jude Medical (STJ) 7:30am, $0.87; Preview

- Abbott Laboratories (ABT) 7:36am, $1.22; Preview

- WW Grainger (GWW) 8am, $2.62

- Amphenol (APH) 8am, $0.84

- First Republic Bank/CA (FRC) 8am, $0.64

- SEI Investments (SEIC) 8:30am, $0.30

- Qualcomm (QCOM) 4pm, $0.86

- Stryker (SYK) 4pm, $0.99

- CYS Investments (CYS) 4pm, $0.48

- Greenhill & Co (GHL) 4pm, $0.25

- Platinum Underwriters Holdings (PTP) 4pm, $1.19

- RLI Corp (RLI) 4pm, $1.13

- Select Comfort (SCSS) 4:01pm, $0.27

- Covanta Holding (CVA) 4:01pm, $0.12

- International Business Machines (IBM) 4:03pm, $3.43

- Wintrust Financial (WTFC) 4:03pm, $0.47

- Yum! Brands (YUM) 4:05pm, $0.70

- Kinder Morgan Energy Partners (KMP) 4:05pm, $0.47

- Kinder Morgan (KMI) Aft-mkt, $0.26

- F5 Networks (FFIV) 4:05pm, $1.14

- LaSalle Hotel Properties (LHO) 4:05pm, $0.75

- Umpqua Holdings (UMPQ) 4:05pm, $0.21

- American Express (AXP) 4:06pm, $1.10

- EBay (EBAY) 4:15pm, $0.55

- Xilinx (XLNX) 4:20pm, $0.45

- SLM Corp (SLM) 4:30pm, $0.54

- Skyworks Solutions (SWKS) 4:30pm, $0.44

- Cohen & Steers (CNS) 4:30pm, $0.41

- East West Bancorp (EWBC) 4:45pm, $0.46

- NI (HNI) 5pm, $0.17

- Noble (NE) 5pm, $0.57

- Crown Holdings (CCK) 5:03pm, $0.84

- CVB Financial (CVBF) Late, $0.21

- El Paso Pipeline Partners (EPB) Aft-mkt, $0.50

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – its telling you all you need to know about no iQe4 upgrade drugs from Bernanke. With tensions in the Middle East rising, we like the long USD, short Gold (and Gold Miners) position more than long USD vs short Oil. Next support for Gold = $1559, but it’s loose.

- Shell-Led Arctic Push Finds U.S. Shy in Icebreakers: Energy

- Looming Copper Surplus Contracting as Mining Fails: Commodities

- Gold Set to Drop as Fed Refrains From Specific Easing Measures

- Corn Seen Rallying to Record $8.50 as Drought Kills Crops

- India to Curb Hoarding as Food Prices Rally on Weak Monsoon

- Japan Commission to Review Easing of U.S. Beef Import Curbs

- Corn Drops for Second Day on Concern Rally Is Curbing Demand

- Copper Rises on Speculation About Additional U.S. Policy Easing

- Oil Declines From Seven-Week High on Outlook for China, Europe

- BHP Sees Escondida’s Copper Output Rising by Nearly Half in FY15

- Cocoa Falls on Demand Speculation Before Processing Figures

- Silver Seen Declining to Lowest Since 2010: Technical Analysis

- China Money-Supply Pickup Signals GDP Recovery: Chart of the Day

- BHP Iron Ore Output Rises 15% to Beat Analyst Estimate

- U.S. Feedlots Buy Fewer Cattle as Feed Costs Rise, Survey Says

- Cocoa Arrivals From Brazil’s Bahia Advance 24%, Hartmann Reports

CURRENCIES

EUROPEAN MARKETS

ITALY – back into crash mode the MIB Index goes (-21% from YTD top) as the Italians really have nothing but hope and prayers left until the Germans ratify whatever Italian banks will need on September 12th; without German Parliament signing off on it, Spain can try to jockey the headlines, but Italy is on a political island that the Germans own.

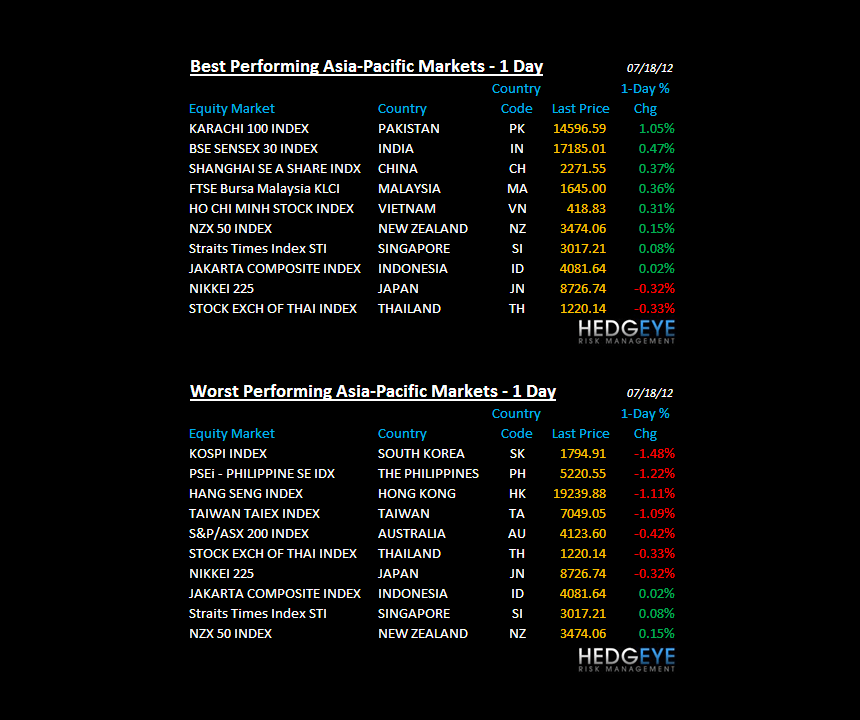

ASIAN MARKETS

KOSPI – in one of the nastier reversals from US green close to Asian red close last night, the KOSPI got pounded -1.5% to re-test its YTD lows; #GrowthSlowing is accelerating on the downside, globally, where it matters (Tech and Industrials demand); many ignored that in mid-April too. We didn’t, and won’t.

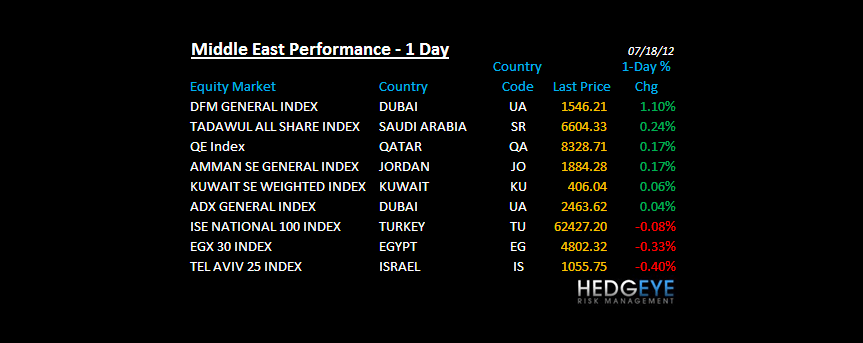

MIDDLE EAST

The Hedgeye Macro Team