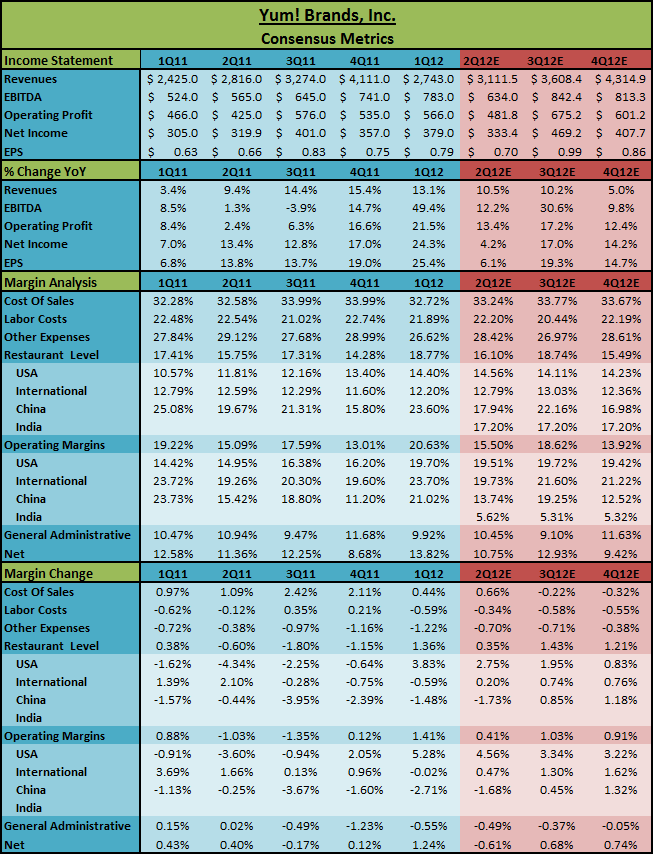

In preparation for YUM’s 2Q12E earnings release on 7/18, we’ve put together the recent pertinent forward looking company commentary from 1Q12 including Hedgeye commentary and important consensus metrics for the upcoming 2Q12 earnings release.

Summary Thoughts

- YUM is comparing against a more difficult 2Q11 results. It’s unlikely they raise full-year EPS forecast above the current 12% pace.

- Short interest is very low at 1.82%, but has risen sharply in the last month.

- Sentiment has turned down over the past eight weeks but remains one of four names in the restaurant space with a Hedgeye sentiment ranking of 90 or better.

- The sentiment surrounding YUM China drives this stock. Given the news flow from China, it will take nothing short of a spectacular quarter for the street to be comfortable with how 2H12 is shaping up.

CHINA

“KFC now has 3,819 restaurants with average unit volumes of $1.7 million; in 800 cities throughout the country and continues to expand into new cities as well as increase its penetration levels in existing markets. KFC is deeply rooted in China with its localized menu and broad appeal. Virtually all KFCs in China serve breakfast, which accounts for about 6% of sales. Nearly half our KFC restaurants offer delivery service and over half have 24-hour operations. These service and day part extensions are all in the early phases of development and provide tremendous growth potential for years to come as we further leverage our restaurant assets.”

“Next, I want to provide an update on our China margin expectations. Let me start by discussing our pricing strategy in China as our approach continues to evolve. Historically, our pricing actions have been implemented nationally and all at one time. Going forward, we will take pricing across our system at various levels and at different stages, depending on the trade zone. This will allow our team to more effectively monitor the consumer reaction to pricing."

“In 2011, we had a 3% price increase at the end of January. With the phase-in pricing approach, we have a relatively small impact from new pricing in the second quarter. As a result, we will likely see a decline in margins in the second quarter that is somewhat higher than what we saw in the first quarter. However, we are still roughly on track with what we outlined in our December meeting.”

“As you may recall, we estimated that first quarter margins would be about two points below last year. As the year progress, we expect the combination of our cumulative staged pricing and moderating inflation to result in year over year margin improvement of up to 2% in the second half of the year. I'm confident the team will continue to generate annual Restaurant margins of about 20%.”

“As we look into the balance of 2012, I believe that this will be another year of improvement to our competitive position and our business model. Our new unit development opportunities are as robust as they have ever been. Higher return new unit development continues to be the foundation of our growth in China. As I've said before, it's a pretty easy decision to improve capital investments when you have average cash paybacks of less than three years. It's even easier when you know how much discipline our China team incorporates into the development process."

"Now I want to provide a brief update on Little Sheep. As indicated on our fourth quarter call, with revenue of about $300 million, the Little Sheep business will add about 5% to our revenue base in China this year. In 2011, the Little Sheep business started strong but struggled in the second half of the year. Operating profit was about $20 million for the full year. We are still in the process of getting our arms around Little Sheep as we transition this business into Yum! China. We will begin reporting Little Sheep numbers in our second quarter results."

"I want to reiterate when you take into account transaction and transition costs, we expect only a modest profit benefit, if any, in 2012. However, we remain excited about having Little Sheep in our portfolio and we believe in the long-term potential of the brand and will invest behind its future success.”

CHINA’S MARGINS

“The biggest impact, we said we expect sales to moderate, but the impact is really inflation was very, very high in the third and fourth quarters last year. We got behind from a pricing standpoint. We think this staged pricing will start to have an impact in the second half of the year."

"Plus we expect inflation to moderate in the balance of the year. Again, to put things in perspective on the inflation side, on the commodity side in particular, we said going into the year, we expected 6%. We had 10% in the first quarter. If anything, we're gaining more confidence that 6% is the high end of what we expect from commodity inflation. So you have that benefit plus the cumulative pricing coming in that should help the margins in the second half.”

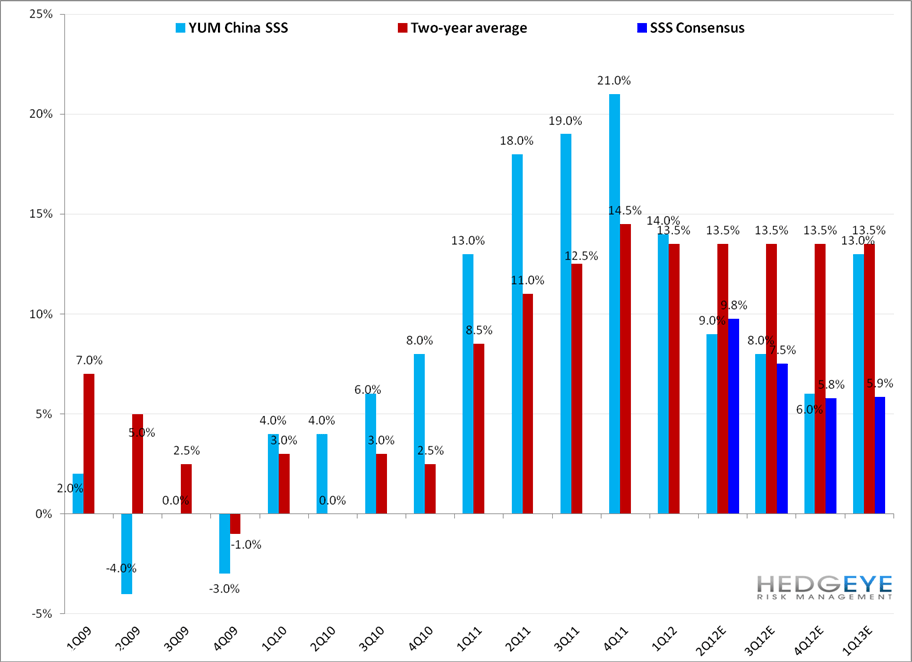

HEDGEYE – For YUM, the MACRO outlook on China is difficult to read. The Chinese government is trying to make the

economy more dependent on consumption and less on exports. To the degree that it is successful, YUM’s brands will benefit. Consumer confidence has been trending lower since 2007, but has improved in early 2012. Longer-term the potential for a housing bubble could hurt consumption. The biggest hurdle the company faces are difficult same-store comparisons from 2011.

SALES

“Our ongoing model does not meet the high level of same-store sales growth that we've recently experienced. We expect same-store sales to moderate at some point, although it's difficult to tell when that will occur. The important point is during 2012, we are again building up day parts and initiatives that can help drive sales well into the future.”

“I think it's really hard to forecast same-store sales in a year, in 2012 coming off a year like 2011, which was so strong from a same-store sales perspective. On the positive end you have momentum, on the negative side you know you're going to be lapping some big numbers, especially as we get into the second half of the year. We're not going to give a forecast for the second quarter. What I would say is traditionally we let people know if there's a significant bending in the trend. And we're not saying there's a huge change in the trend versus what we saw in the first quarter. So we're obviously off to a very good start.”

HEDGEYE – The comments are referring to the fact that SSS will slow in China sooner rather than later, but primarily as a result of difficult comparisons. News from other consumer product companies would suggest that YUM could see a significant slowdown this quarter.

“For Yum! Restaurants International, our sales results have been mixed in Western Europe and we expect this to continue, at least in the near term. Our focus in our strategic growth markets remains, driving profitable new growth development.”

HEDGEYE – Fortunately for YUM, Western Europe is a small part of the business and it’s primarily franchised. That being said, “Slowing growth” compresses equity multiples!

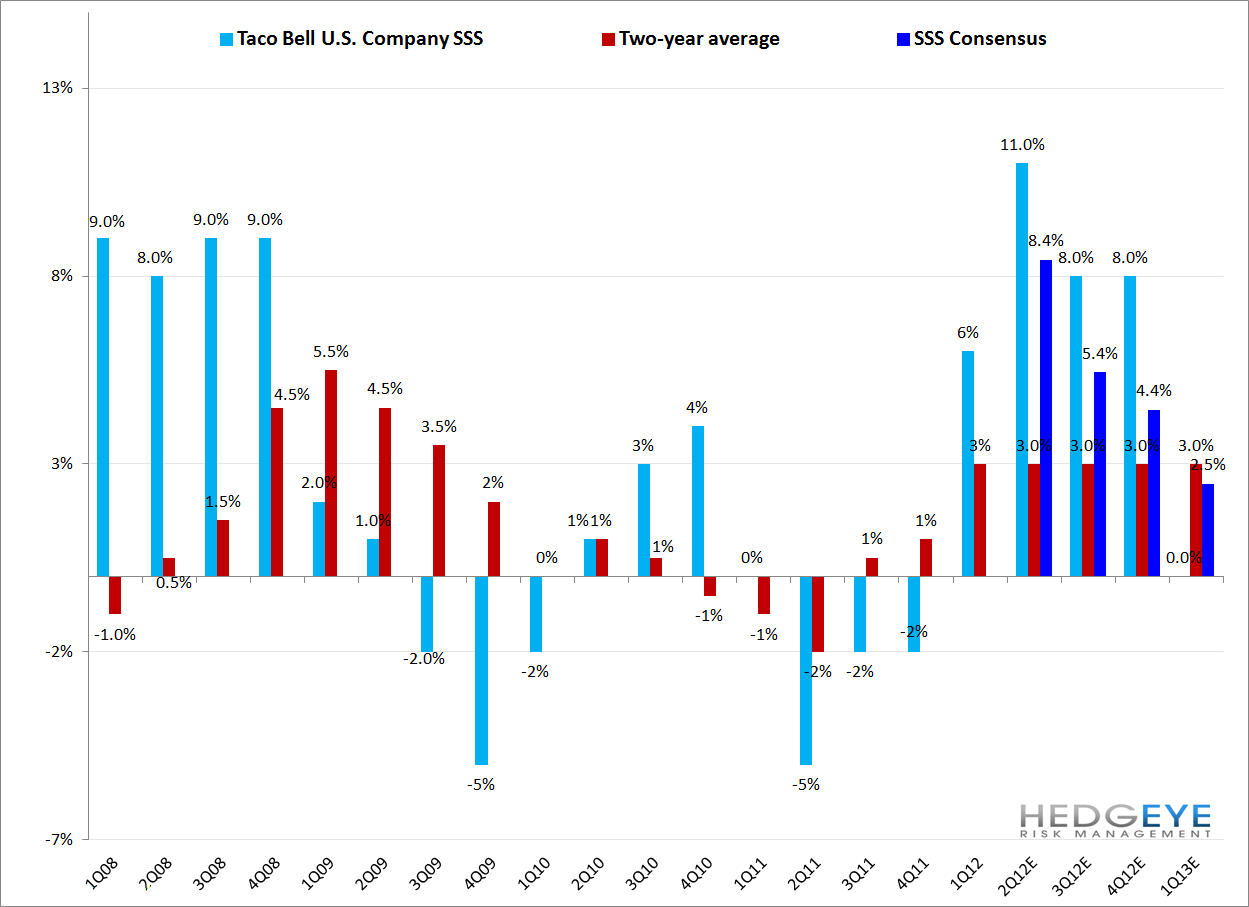

“In the United States, we expect strong second quarter sales at Taco Bell. The first quarter included only a few weeks of the Doritos Locos taco sales. This has been an enormously successful product introduction and thus far the second quarter sales at Taco Bell are running higher than they were in the first quarter. For the second quarter, we expect same-store sales at Taco Bell to be in the high single digits or low double digits.”

HEDGEYE – The Company reiterated the comment about Taco Bell’s performance on 5/8 but failed to mention it in two other conference appearances. How refreshing after a five year drought that we are seeing YUM’s business in the USA post strong numbers. Especially compared to what’s happening in a number of key regions around the world, the USA is looking stable, and Taco Bell has some momentum.

ANOTHER DIFFICULT COPARISON

“In our U.S. business, the 53rd week provided $18 million of operating profit benefit in the fourth quarter of 2011. This benefit was offset with higher spending throughout the year including franchise development incentives and higher than normal costs from restaurant closes. While the combined full-year impact is modest, the 53rd week will have a significant operating profit headwind for the U.S. in the fourth quarter of this year.”

"It will also negatively impact Yum! Restaurants International profits by about $8 million in the fourth quarter. International development continues to be quite strong. We opened 297 new units in the first quarter and our new unit pipeline is solid. We are expecting to open over 1,500 new international units in 2012, including 800 at Yum! Restaurants International, 100 units in India, and at least 600 in China. This is a key growth driver in 2012 and 2013 and I am encouraged by this pace of development."

TAX RATE

“Our expected full year tax rate is about 26% prior to special items. This is almost two points higher than our 2011 effective tax rate of 24.2%. A full year rate of 26% would result in a drag of about three points on full-year EPS growth. We expect the year over year impact on tax to be severe in the second quarter, due to the unusually low rate of 16.7% last year. This will materially impact our second quarter EPS growth.”

HEDGEYE – Both of these issues are cosmetic and can be fodder for the bear case. This is not a substantial concern and might be the least of the company’s concerns if the operating environment in China is as difficult as some believe.

Howard Penney

Managing Director

Rory Green

Analyst