Still treading water

M&A and Other Trends for Q2 2012

- Q2 2012 US hotel transaction volume was a meager $1.5 billion, up from Q1 2012's $1.0 billion, but down significantly from Q2 2011's $4.0 billion.

- The number of US hotel transactions in Q2 2012 almost double that in Q1 2012

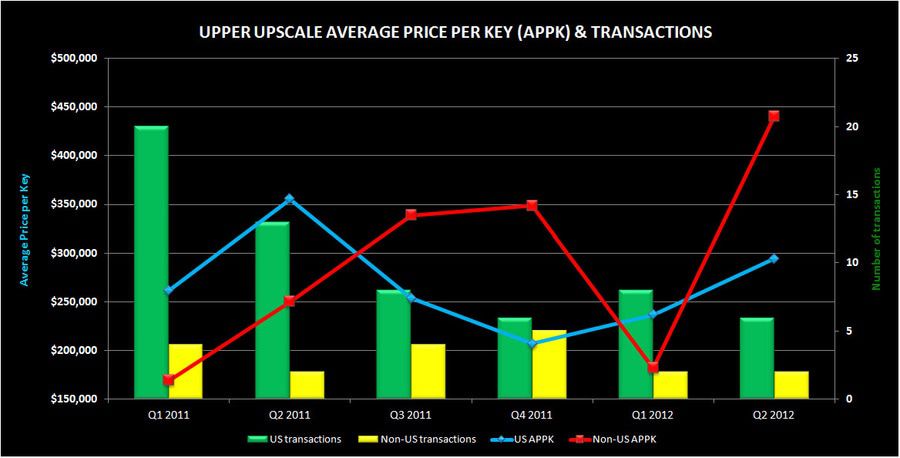

- US average price per key (APPK) in the Upper Upscale segment rose 24% QoQ

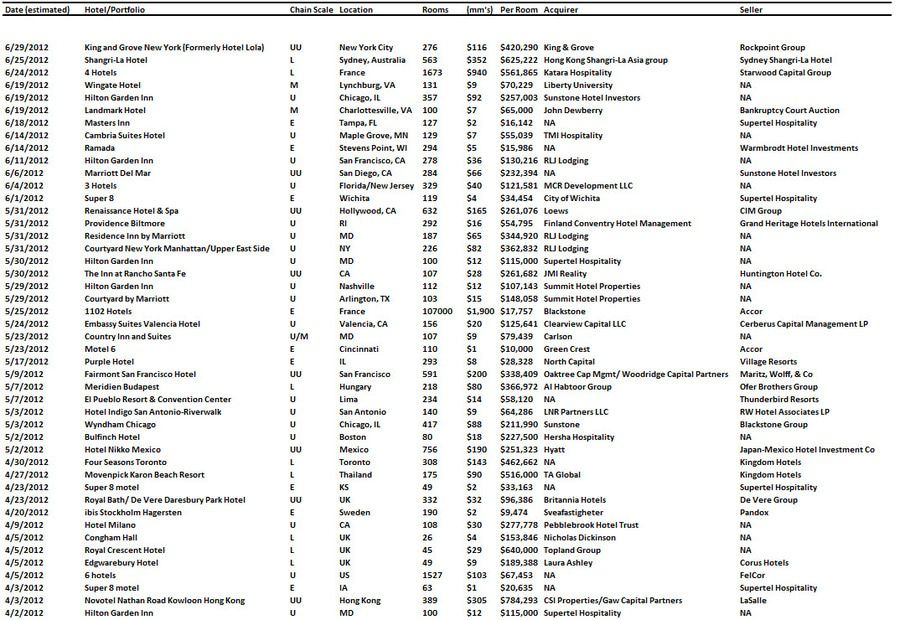

- Non-US APPK in the Upper Upscale segment jumped because of the sale of Novotel Nathan Road Kowloon Hong Kong, the largest single hotel transaction in Hong Kong recorded in the last 11 years

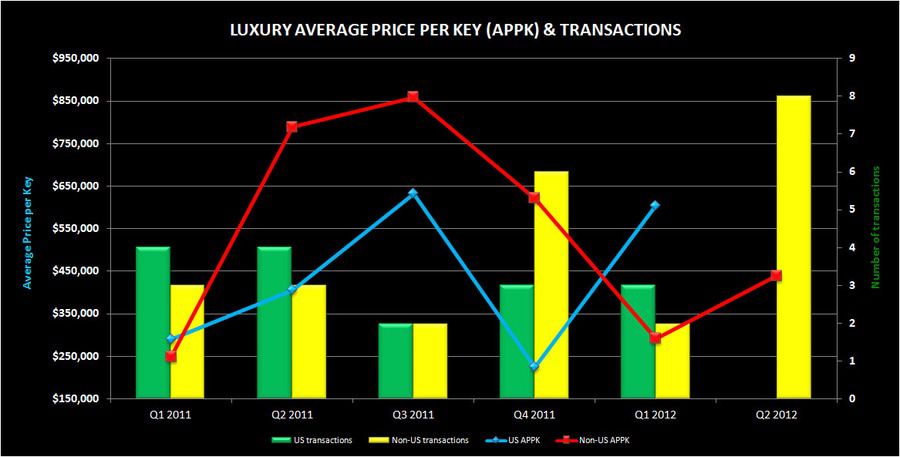

- All of the luxury transactions occurred outside of the US

- There were four portfolio deals including Blackstone's purchase of Accor's Motel 6 unit

- According to Fitch, May hotel delinquency rate was 11.15%, higher than April's 10.20%. The higher hotel delinquency rate was partly due to the inclusion of the Marriott Waikiki to the hotel index. The delinquency rate remains below the 14% seen in Q3 2011.