Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

Key Takeaways:

* One week ago we published our risk monitor with the title "Risk Cooling Off, For Now". While that didn't seem to be the case on Monday of last week, it certainly played out over the remainder of the week. This morning, we're struck most by the divergence between sovereign and bank default swaps in Spain and Italy. The strength in the sovereign swaps is reflecting the perceived progress made at the EU summit to directly recapitalize the banks. However, you'd expect to see that reflected in reduced default expectations at the banks themselves. This wasn't the case, however, as Spanish and Italian bank CDS was broadly wider last week.

-------

If you’d like to discuss recent developments in Europe, from the political to financial to social, please let me know and we can set up a call.

Matthew Hedrick

Senior Analyst

(o)

-------------

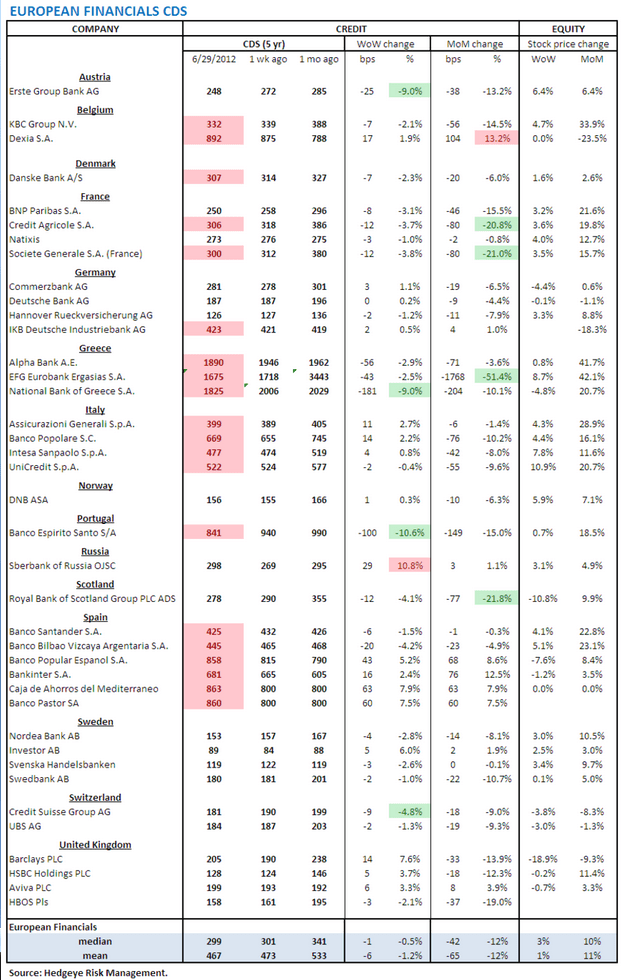

European Financials CDS Monitor – The most interesting takeaway in this week's risk monitor is that the Spanish and Italian banks swaps were broadly worse week over week, while the sovereign default swaps were much tighter. Considering that the strength in the sovereign swaps was reflecting the plan to directly recap the banks through the ESM, we find it surprising that the individual company default probabilities seem not to have noticed. Overall, 22 of the 39 European financial reference entities we track saw spreads tighten last week. The median tightening was 0.5% and the mean tightening was 1.2%.

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. Last week, the Euribor-OIS spread tightened by 1 bp to 42 bps.

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis. As the chart shows, European bank reliance on the ECB remains exceptionally high.

Security Market Program – For the sixteenth straight week the ECB's secondary sovereign bond purchasing program, the Securities Market Program (SMP), purchased no sovereign paper for the latest week ended 6/29, to take the total program to €210.5 Billion. Could this position of hold change? We think the ECB has to take a larger role to buy Europe’s sovereign peripheral paper. We’ll be looking to this Thursday’s ECB meeting for any information on a change of positioning.