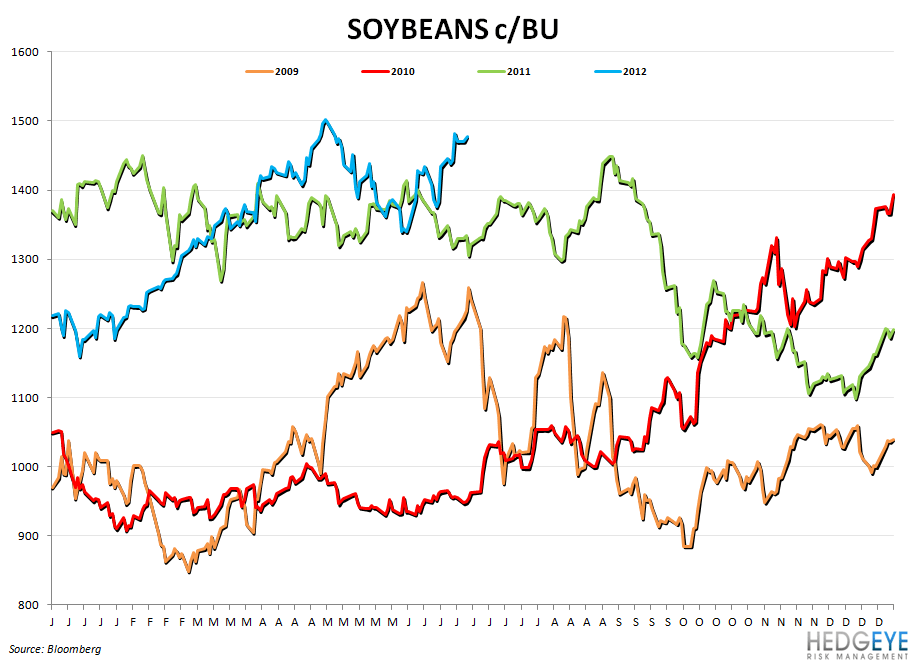

Corn and wheat prices increased sharply week-over-week as hot and dry conditions persist across the corn belt fueled speculation that crop yield estimates for the United States would be revised lower when the next USDA WASDE report is released on July 11th.

General Overview

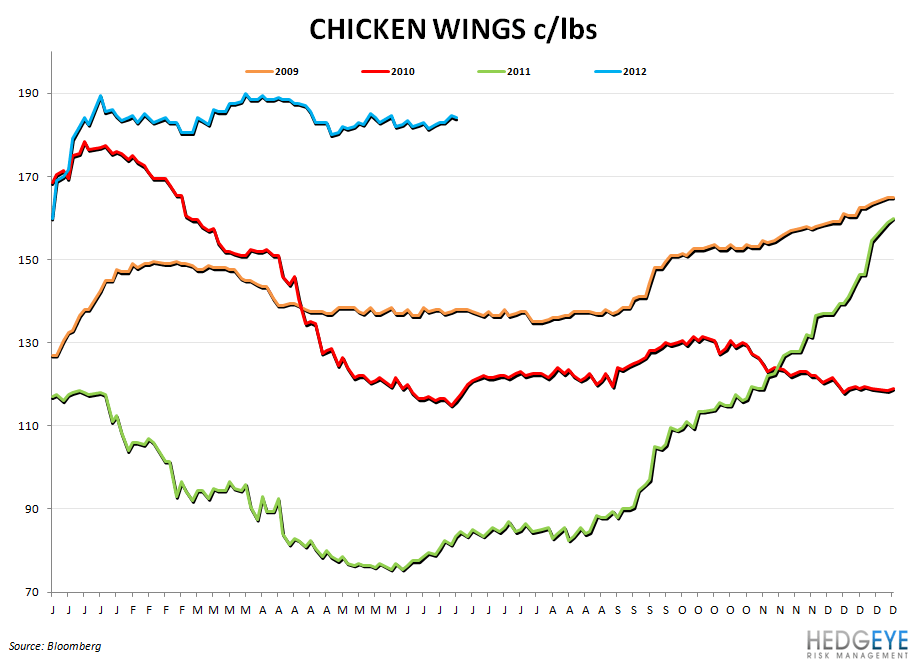

A government meteorologist was quoted in the press today as having said that this year’s weather pattern, which settled into the Great Plains and the Southwest last year and has spread into the Corn Belt, resembles those of 1988. With corn stockpiles already low, grain prices could have room to run. Overall over the past week, despite the dollar gaining slightly versus a week ago, commodity prices we follow that pertain to the restaurant space moved higher. The standouts on a year-over-year basis are chicken wings and wheat on the upside and coffee and dairy, on the downside.

Commodity News

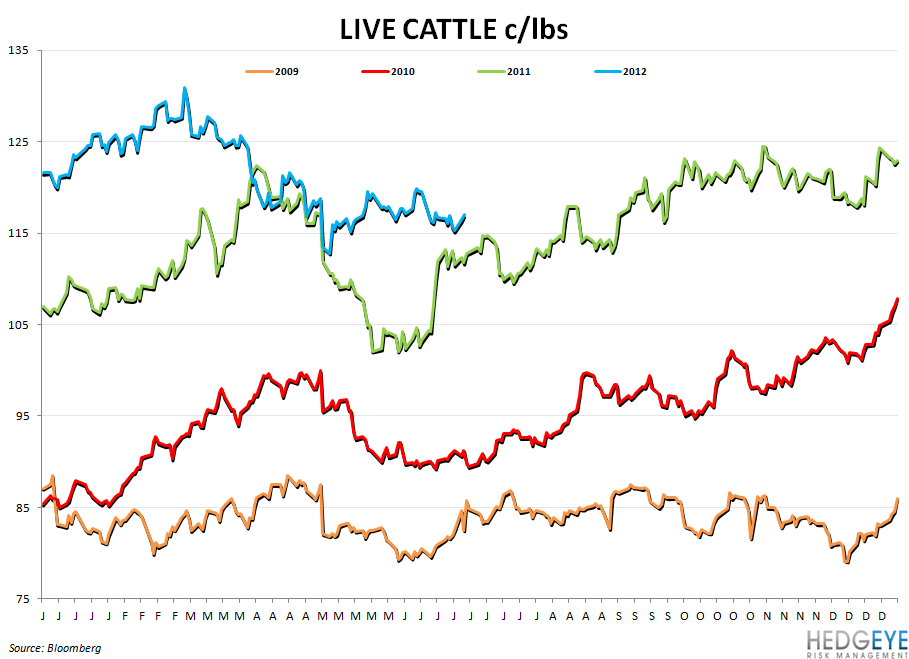

Beef prices are likely to find support this summer from the dry and hot conditions and the derivative impact on feed costs and herd sizes. Consumer prices for beef at retail continue to move higher than overall food costs.

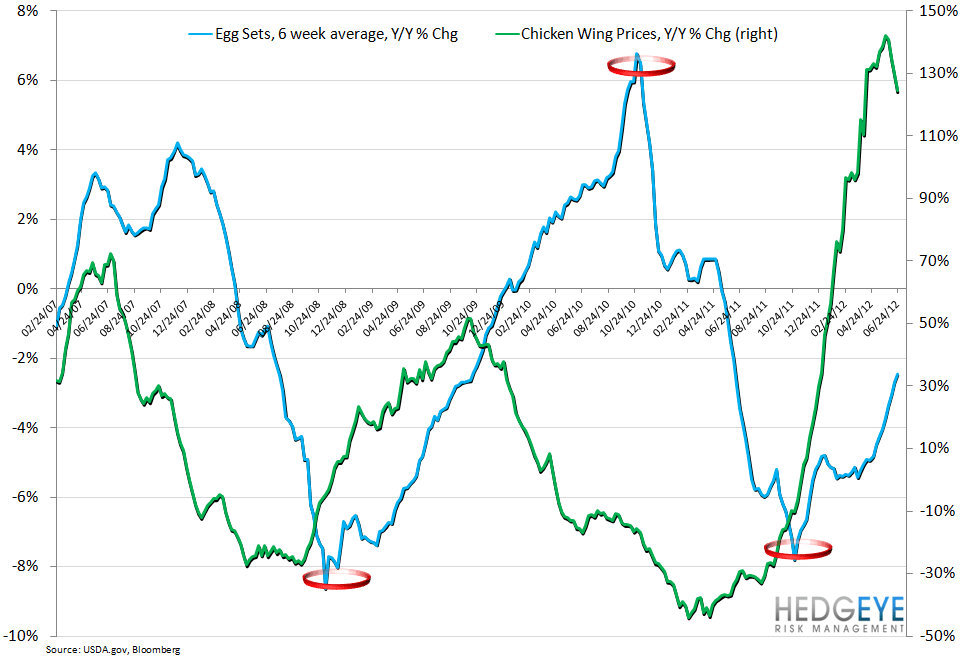

Chicken supplies remain tight but, on a year-over-year basis, USDA data released today shows that the supply of egg sets is declining by 2% compared to 6% declines seen as recently as April.

Correlation Table

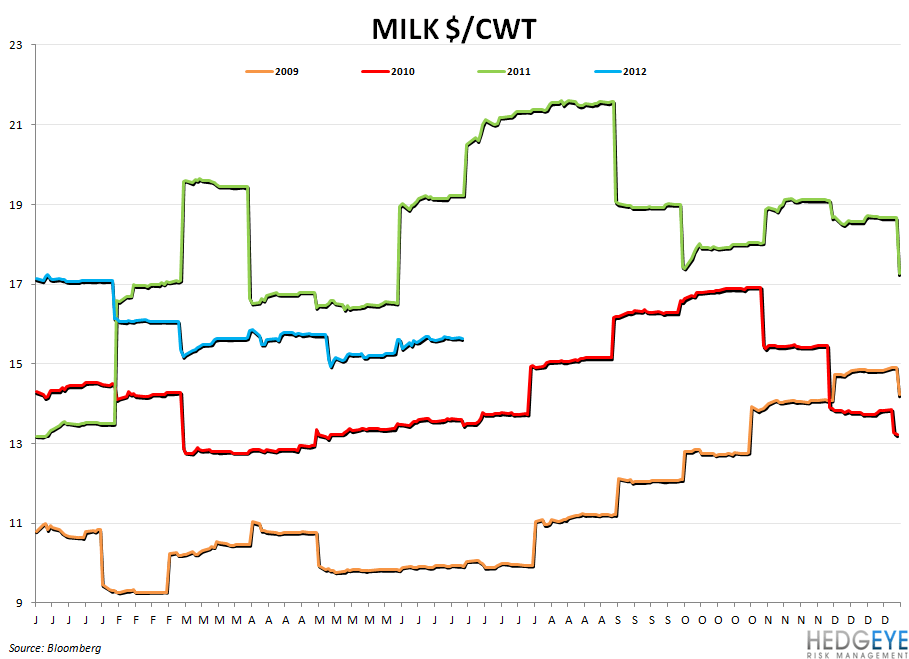

Charts

Howard Penney

Managing Director

Rory Green

Analyst