TODAY’S S&P 500 SET-UP – June 26, 2012

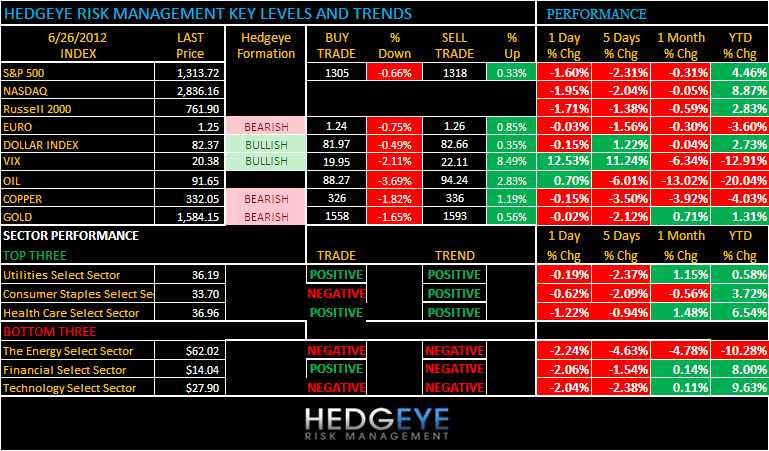

As we look at today’s set up for the S&P 500, the range is 13 points or -0.66% downside to 1305 and 0.33% upside to 1318.

SECTOR AND GLOBAL PERFORMANCE

SECTORS – most important risk management point in our S&P Sector Studies last night was mean reversion – leaders (Tech and Consumer) are now flagging the same risk signals as the losers (Energy and Industrials). It’s just one of the many signals that tell me earnings season will be as bad as the companies are already whispering (73 SP500 companies already guide down).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/25 NYSE -1657

- Down from the prior day’s trading of 1140

- VOLUME: on 6/25 NYSE 753.75

- Decrease versus prior day’s trading of -52.22%

- VIX: as of 6/25 was at 20.38

- Increase versus most recent day’s trading of 12.53%

- Year-to-date decrease of -12.91%

- SPX PUT/CALL RATIO: as of 6/25 closed at 1.86

- Up from the day prior at 1.65

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 37

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.63

- Increase from prior day’s trading at 1.60

- YIELD CURVE: as of this morning 1.34

- Up from prior day’s trading at 1.31

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook retail sales

- 9am: S&P/CS 20 City M/m, April, est. 0.3% (prior 0.1%)

- 9am: S&P/CaseShiller Home Price Index, April, est. 134.85 (prior 134.1)

- 10am: Consumer Confidence, June, est. 63 (prior 64.9)

- 10am: Richmond Fed Manufacturing Index, June, est. 3 (prior 4)

- 11am: Fed to purchase $4.5-$5.5b notes in 8/15/2020-5/15/2022 range

- 11:30 am: Treasury to sell $25b 52-wk bills, 4-wk TBA

- 1pm: Treasury to sell $35b 2-yr notes

- 4:30pm: API inventories

GOVERNMENT:

- House, Senate in session

- OECD releases survey of U.S. economy, 10am

- Senate Banking Cmte hearing on how to empower and protect military servicemembers in the consumer finl mktplace, 10am

- National Research Council holds conference on NASA’s strategic direction, with space agency officials, 8am

WHAT TO WATCH:

- Rupert Murdoch is said to consider splitting News Corp. into two, one focusing on publishing, the other entertainment

- Moody’s downgrades 28 Spanish banks on debt risk

- Apple’s bid to limit Google’s use of certain patents as a tool to block imports of the iPhone and iPad may be getting traction at a U.S. trade agency

- EU President Van Rompuy’s report on the future of the euro includes the option of a “phased” introduction of common debt

- Facebook appointed COO Sheryl Sandberg to board, naming 1st female dir.

- U.S. Congress said to consider delaying automatic federal spending cuts until March 2013

- Russell announces final 2012 membership lists for indexes

- Encana is investigating a news report of e-mails between it and Chesapeake Energy regarding land-lease bidding in Michigan

- Vivendi to appeal $956m verdict in a lawsuit over its 2001 purchase from Liberty Media of its stake in USA Networks

- Spain sells EU3.08b of bills vs maximum target EU3b; sells 6-month bills at 3.237% vs 1.737% in May

- Italy sells zero 2014 bonds at 4.712% vs 4.037% on May 28

- Europe’s financial crisis isn’t affecting the ability of speculative grade U.S. companies to meet debt obligations, keeping the default rate below the historical average: Moody’s

- BP sold stakes in 2 North Sea fields to Mitsui for $280m in cash

- Corn climbs to 7-mo. high

- KKR raises $4b for investments in infrastructure, energy

- Madoff customer pool is poised to swell to $7.3b by July

- U.K. posts larger budget deficit than economists forecast in May

- HSBC lowered its projection for China’s economic expansion this year to 8.4% from 8.6%

EARNINGS:

- Robbins & Myers (RBN) 8:30am, $0.90

- H&R Block (HRB) 4pm, $2.07

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor has been signaling #GrowthSlowing since Feb/Mar; that has not changed here in June as Copper has tried to rally several times and failed each time at lower-highs, down another -0.4% this morning to 3.31; question is when does it have a $2 handle? Strong Dollar will deflate the commodity inflation.

- Cattle-Hide Economy Slumping as Goldman Sees Rally: Commodities

- Oil Trades Little Changed as Storm Threat to U.S. Supply Fades

- Corn Climbs to Seven-Month High as Dry Weather Parches U.S. Crop

- Cocoa Rises on Speculation Ivory Coast Rains Will Cause Disease

- Russia Increases Gold Reserves as Ukraine, Kazakhstan Add Metal

- Gold Set to Decline on Concern Europe’s Crisis Will Boost Dollar

- Copper Seen Rising for Second Day as China Demand May Strengthen

- KKR Raises $4 Billion for Investments in Infrastructure, Energy

- Gasoline Supplies Gain for Second Week in Survey: Energy Markets

- Rice Crop in India at Record to Spur Exports for Second Year

- ETFs Passive No More in Challenge to $7.8 Trillion Active Funds

- Paris Rapeseed Set to Gain on Moving Average: Technical Analysis

- Tropical Storm Debby Edges Eastward Toward Florida’s Gulf Coast

- Mitsubishi’s $5.4 Billion Copper Bet Sparks Codelco Fight

- Iron Ore Set for Monthly Advance as China Stimulus Boosts Demand

- China’s First Wind-Farm Lull Limits Outlook for Sinovel: Energy

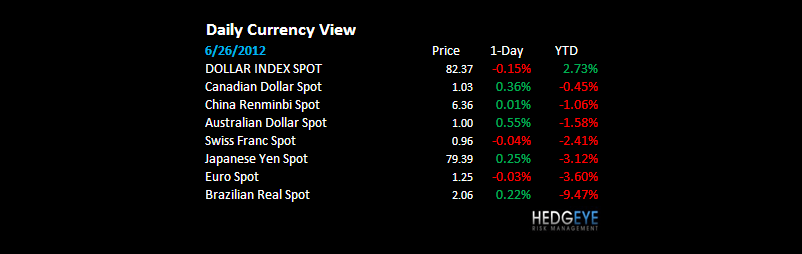

CURRENCIES

EUROPEAN MARKETS

ITALY – one of the foundations of Keynesian central planning is the belief that governments can “smooth the business cycle”; how’s that working out? Italian Retail Sales plummeting (-6.8% y/y) and Italy’s CDS rising back up to 590 this morning as Italian Bank funding issues come back to the table (Monti Pasche, 3rd largest Italian bank); MIB remains broken/crashing.

ASIAN MARKETS

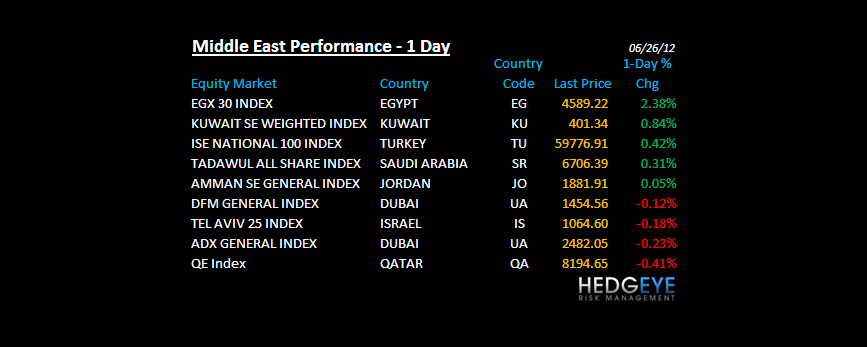

MIDDLE EAST

The Hedgeye Macro Team