TODAY’S S&P 500 SET-UP – June 20, 2012

As we look at today’s set up for the S&P 500, the range is 33 points or -2.13% downside to 1329 and 0.30% upside to 1362.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/19 NYSE 2074

- Up from the prior day’s trading of 539

- VOLUME: on 6/19 NYSE 772.04

- Increase versus prior day’s trading of 9.16%

- VIX: as of 6/19 was at 18.38

- Increase versus most recent day’s trading of 0.33%

- Year-to-date decrease of -21.45%

- SPX PUT/CALL RATIO: as of 6/19 closed at 1.54

- Up from the day prior at 1.51

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – all the while, the bond market doesn’t care. Makes sense because the bond market has had what we have had right since March – more Qe slows growth. 10yr yield at 1.63%, up a whopping 5bps for the week and remains in a bearish formation with all 3 risk mgt durations of resistance overhead.

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.63

- Increase from prior day’s trading at 1.62

- YIELD CURVE: as of this morning 1.35

- Up from prior day’s trading at 1.33

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, June 15

- 10:30am: DoE Inventories

- 12:30pm: FOMC Rate Decision

- 2pm: FOMC Releases Projections of Economy and Fed Funds

- 2:15pm: Bernanke holds news conference on FOMC

GOVERNMENT:

- Federal Open Market Committee concludes 2-day meeting

- Interior Dept. auctions oil, natural gas leases in 39m acres in central Gulf of Mexico

- House, Senate in session

- Senate Banking subcommittee holds hearing on ordinary investors, IPO process

- Senate to vote on EPA air toxics rule

- House Education, Workforce panel holds hearing on multi- employer pension plans, with treasurer Kroger, CEO of Arkansas Best, 10am

- House Financial Services panel holds hearing on “Market Structure: Ensuring Orderly, Efficient, Innovative and Competitive Markets for Issuers and Investors”

WHAT TO WATCH:

- Fed seen extending Operation Twist, avoiding bond buying

- News Corp. makes A$2b bid to double stake in Australia pay- TV

- Procter & Gamble cuts quarterly forecasts

- Interior Dept. auctions oil, natural gas leases in 39m acres in central Gulf of Mexico

- Greek leaders poised to agree on three-way coalition

- King sought GBP50b QE extension in BOE vote defeat

- Quest Software accepts sweetened $25.75-shr bid from Insight

- Chevron among bidders seeking leases near BP spill site

- J.D. Power new-car survey to be released

- Senate to vote on air-toxics rule; BGOV Insight

- MSCI releases annual market-classification review

- MSCI seen passing over Taiwan, S. Korea for upgrades

EARNINGS:

- JinkoSolar Holding (JKS) 6:37am, CNY(5.16)

- Actuant (ATU) 7:30am, $0.59

- Micron Technology (MU) 4pm, $(0.21)

- Steelcase (SCS) 4:01pm, $0.13

- Clarcor (CLC) 4:02pm, $0.70

- Red Hat (RHT) 4:05pm, $0.27

- Bed Bath & Beyond (BBBY) 4:15pm, $0.84

- Apogee Enterprises (APOG) 6:30pm, $0.03

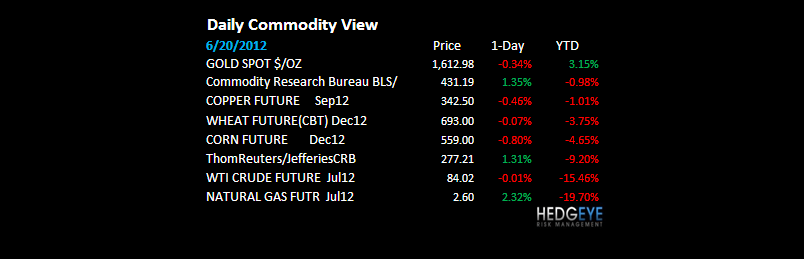

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG

COMMODITIES – nice big rip right back up to where Commodities can resume their bubble popping – if Bernanke doesn’t deliver the drugs today, that is. CRB Index has a stiff immediate-term TRADE line of resistance at 279. Oil, Gold, and Copper are red this morning. The bet was on what people would beg for, not that he’d actually deliver on the bet.

- IPad Boom Strains Lithium Supplies as Prices Triple: Commodities

- JPMorgan Poised to Make 157% Return on MF Global’s LME Shares

- Copper Declines as Fed May Opt Against Further Bond Purchases

- Oil Drops a Third Day in London on Supplies Before Fed Decision

- Cotton Futures Extend Gains After Surging 6% Yesterday on China

- Sugar Retreats After Reaching a Two-Month High; Cocoa Declines

- Oil in Production Conundrum on Saudi-Iran Split: Energy Markets

- Rio Tinto Commits $4.2 Billion to Expand Iron Ore Production

- Gold Seen Falling a Second Day in London Before Fed Decision

- Soybeans Climb as Dry Weather Persists, Threatening U.S. Supply

- Palm Oil Surges Most in 15 Months as Dry Weather Boosts Soybeans

- Japan Passes Sovereign Insurance Bill for Iran Crude Imports

- Hedge Funds Hurt in Third May Commodity Rout as Brevan Drops

- Copper Declines as LME Stockpiles Expand

- Indonesia Reducing Palm Oil Tax Seen Delaying Shipments to July

- Record Soybean Prices to Spur Indian Farmers to Boost Sowing

- Ivory Coast Cocoa Growers Returning to Farms After Attacks

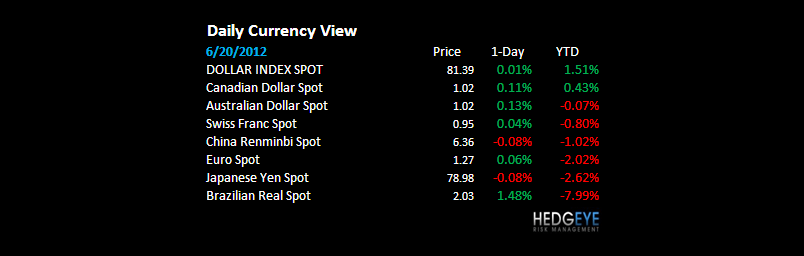

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – evidently every man, woman, and child in China doesn’t yet have a tv to watch the circus of people begging for more of what slows real-inflation adjusted growth (Qe); the Shanghai Comp didn’t cooperate with the “news” yesterday, closing down on the session (-0.3%) and remains broken across all 3 of our risk management durations #GrowthSlowing.

MIDDLE EAST

The Hedgeye Macro Team