TODAY’S S&P 500 SET-UP – June 18, 2012

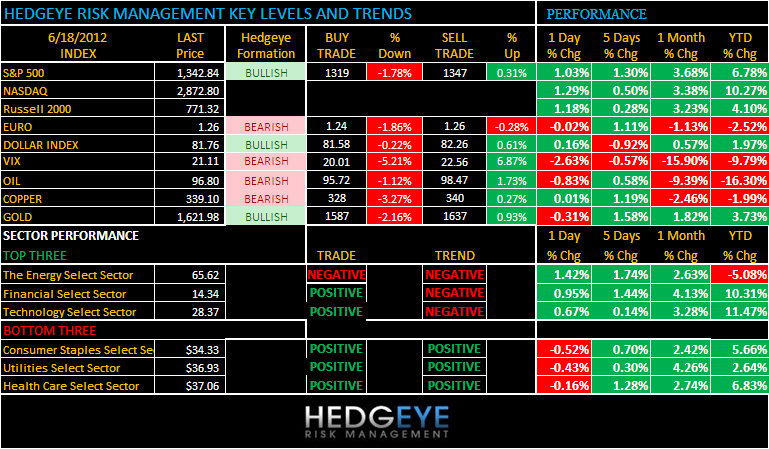

As we look at today’s set up for the S&P 500, the range is 28 points or -1.78% downside to 1319 and 0.31% upside to 1347.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/15 NYSE 1149

- Down from the prior day’s trading of 1229

- VOLUME: on 6/15 NYSE 1513.30

- Increase versus prior day’s trading of 94.17%

- VIX: as of 6/15 was at 21.11

- Decrease versus most recent day’s trading of -2.63%

- Year-to-date decrease of -9.79%

- SPX PUT/CALL RATIO: as of 6/15 closed at 1.72

- Up from the day prior at 1.23

CREDIT/ECONOMIC MARKET LOOK:

BONDS – US and European bond markets continue to front-run manic equity traders; both didn’t change TREND last wk, and this morning you are seeing Spanish 10s shoot back above 7% as UST 10yr remains in Growth Slowing formation at 1.59% (Yield Spread in the US (10s -2s) was down 6bps last wk, despite the no volume rally in stocks.

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.56

- Decrease from prior day’s trading at 1.58

- YIELD CURVE: as of this morning 1.28

- Down from prior day’s trading at 1.72

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: NAHB Housing Market Index, June, est. 28 (prior 29)

- 11am: Fed to purchase $1.5b-$2.25b notes in 2/15/2018-5/15/2042 range

- 11:30am: U.S. to sell $30b 3-mo., $27b 6-mo. bills

- 2pm: Fed to sell $8b-$8.75b notes in 5/15/2013-11/30/2013 range

GOVERNMENT:

- President Obama attends G-20 Summit in Mexico

- House, Senate in session

- AFSCME union holds convention, elects successor to President Gerald McEntee (through Thurs.)

WHAT TO WATCH:

- Samaras begins bid to form Greek coalition to stop crisis

- Euro leaders signal softening on Greek austerity

- Spain 10-yr yield surges past 7% to new record

- Hollande’s Socialist party wins control of French parliament

- Melrose in talks over $2.3b offer for CVC’s Elster

- China May home prices fall in record number of cities on curbs

- FDA staff reports due for 6/20 advisory committee meeting on Sanofi’s semuloparin for prevention of blood clots in chemotherapy patients, ONXX/LGND’s carfilzomib for 3rd-line multiple myeloma

- Orbis will back Vodafone’s bid for Cable & Wireless

- Microsoft, B&N may unveil e-reader/tablet: TechCrunch

- Fairfax Media to cut 1,900 workers as readers migrate to web

- G-20 said to be discussing mix of global stimulus if needed

- Weekly agendas for finance, energy, health, real estate, transports, industrials, technology, consumer, media/entertainment, Canada mining, Canada oil & gas

- Greek Election, G-20 Summit, Fed Meeting: Week Ahead

EARNINGS:

- IHS (IHS) After-mkt, $0.94

- Platinum Underwriters (PTP) After-mkt, $1.16

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

GOLD – no bailout or Monday morning money printing (yet) is pressuring Gold – will be interesting to watch it as a leading indicator into the FOMC meeting on Wednesday and whatever Geithner begs for at the G20 all the while (he wants the US (IMF) to bailout Spanish banks). Sold our long Gold position; shorted the Euro and bought cattle on Friday.

- Hedge Funds Boost Bullish Bets on Stimulus Outlook: Commodities

- Oil Little Changed as European Debt Woes Outweigh Greek Optimism

- HKEx Shares Tumble as ‘Expensive’ LME Bid Seen Passing Regulator

- Wall Street Gas Bears Squeezed by Utility Buyers: Energy Markets

- European Union Says Iran Oil Embargo on July 1 Will Go Forward

- Copper Seen Advancing as Greek Vote Eases Debt-Crisis Concern

- Gold Set for First Decline in Seven Days After Greek Elections

- Cotton Area in India to Drop 10% This Year as Prices Slump

- Gazprom May Offer China Lower Gas Price With Advance Payments

- German Clean-Dark Spread Declines as 2013 Power Contract Drops

- Solar Boom Heads to Japan Creating $9.6 Billion Market: Energy

- U.K. Natural Gas Advances as Norwegian, Dutch Flows Decline

- Noda Ends Japan Nuclear Freeze, Risking Backlash at Polls

- Funds Add Bullish Bets on Stimulus Outlook

- Iran Nuclear Offer Fails to Stall EU Oil Embargo at Moscow Talks

- Corn Climbs After Greek Election Eases Concern Over Euro Crisis

- Angola to Boost August Daily Crude Exports to Six-Month High

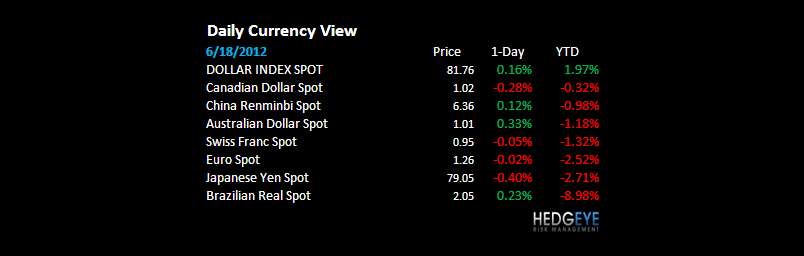

CURRENCIES

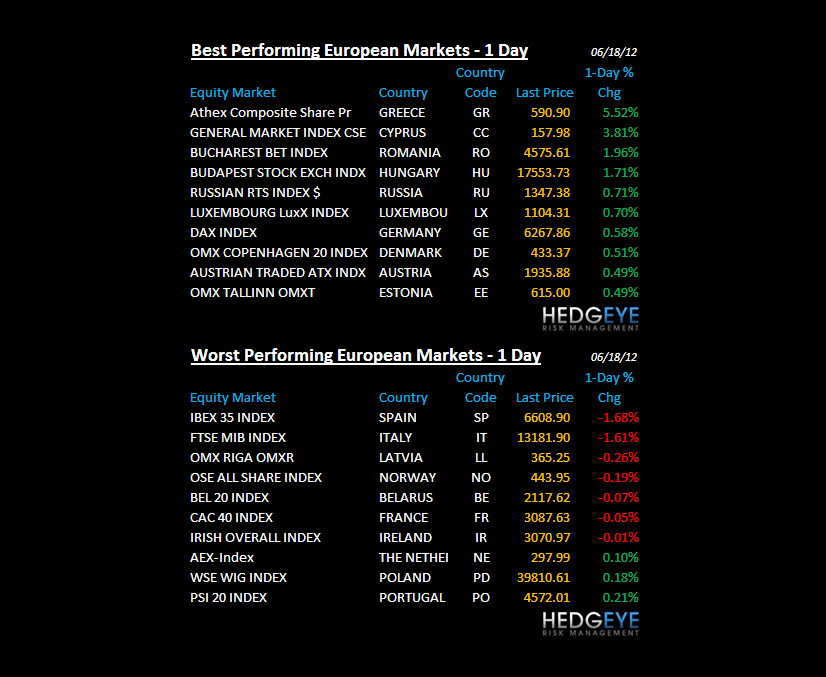

EUROPEAN MARKETS

SPAIN – Greece is the tree, Spain/Italy/Japan is the forest; markets get that – they also get that “coordinated action” means they can’t be fully invested (hedged), which is just sad to watch; Spain’s IBEX and Italy’s MIB down -1.8% and -1.5% this morn in un-coordinate reaction to whatever remains (both continue to crash, down -26% and -23% from YTD tops).

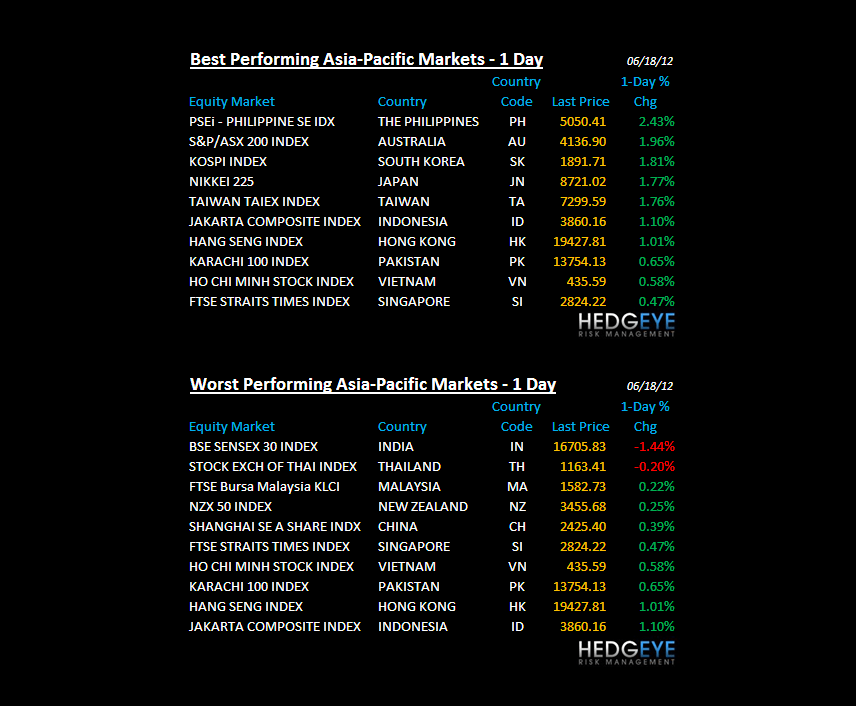

ASIAN MARKETS

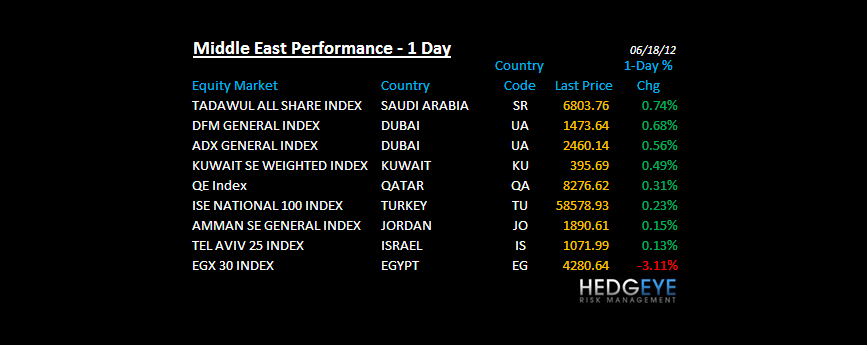

MIDDLE EAST

The Hedgeye Macro Team