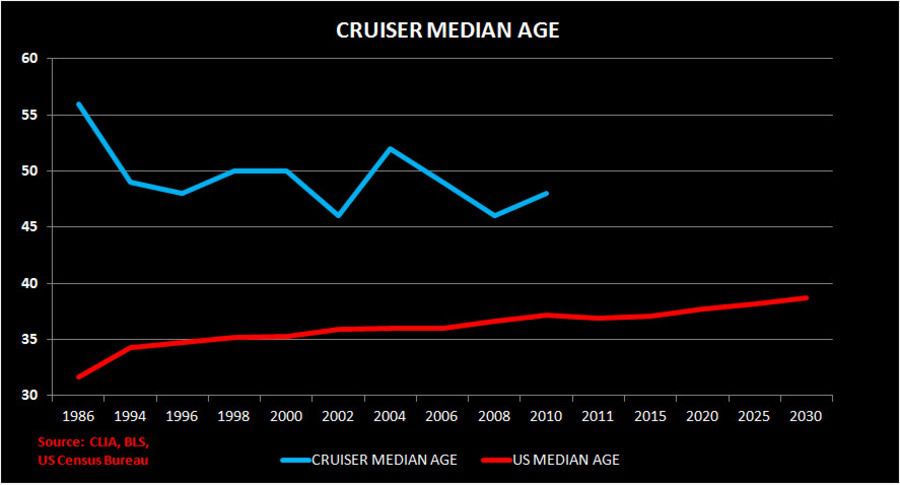

Hedgeye Gaming, Lodging and Leisure Sector Head Todd Jordan’s chart on cruisers, those who travel on cruise ships, shows some surprising trends.

The median age of the cruiser has fallen significantly since 1986 as you can see below. It’s since hovered between 46 and 52 for the last few years. Younger people are digging cruises. The 60-year-old plus crowd is of course the largest customer base but cruises could be coming back in a very cool, hip way. Using our TRADE/TREND/TAIL model, Jordan has a sunny outlook for cruise companies, specifically RCL and CCL.

TRADE: Long RCL /Short CCL – valuation disparity and better pricing outlook for RCL.

TREND: Long RCL and CCL – strong dollar, lower fuel costs, cheap stocks.

TAIL: Long cruisers/short domestic casinos – demographics, basically sub-baby boomer generations are cruising but not gambling.